I have been receiving many questions on Dependents’ Protection Scheme(DPS) over the past few weeks so I thought I will write something about it. The reason why there are so many people asking about DPS recently is because they had received letter notifying of the changes to DPS. We will explore these changes in the later part of this article. First, let us look at what is DPS.

The DPS as the name suggest is to protect your dependents financially in the event of an misfortune. DPS is term insurance that gives a payout benefit of $46,000 should the insured members suffer from the following before the age of 60.

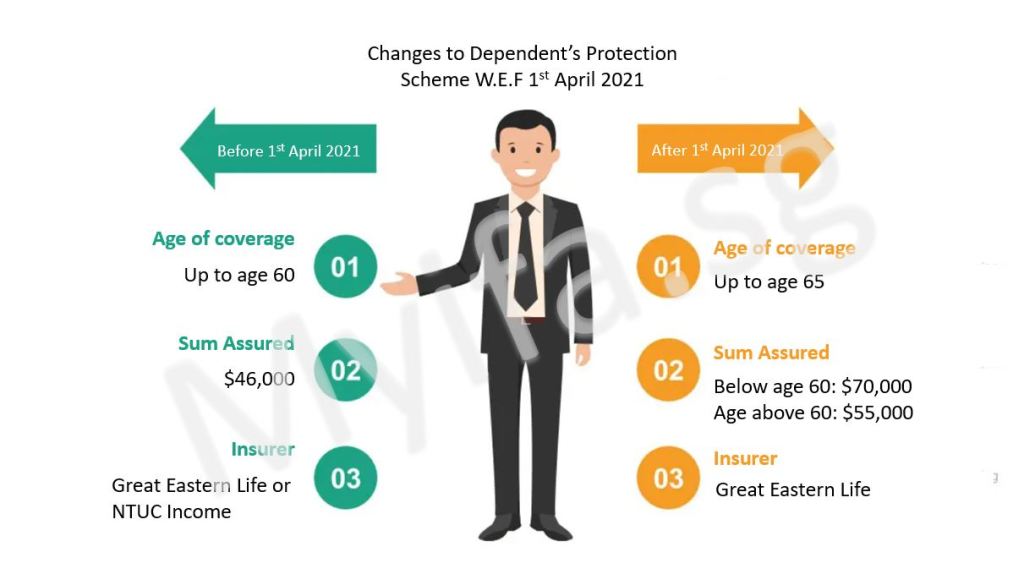

Most Singapore will have DPS coverage but many are unaware of it. This is partly because DPS is automatically extended to Singapore Citizens or Permanent Residents upon their first CPF working contribution between age 21 and 60 years old. Although you can choose to opt-out of this scheme, you are strongly encouraged to keep it. Since the inception of DPS in May 1989 by CPF board, the benefits has been revised upwards so that the payout benefit is more inline with the cost of living. The last revision was in 2005 when DPS was privatised and administered by Great Eastern Life and NTUC Income. Another revision will be made in 1st April 2021 and here are the changes in summary.

One of the common response that I got after my clients knew of the changes is ” Oh! the premium is going to increase again right???!” And you cannot blame them for having such thoughts because logically speaking, that should be the case since the sum assured had increased from $46,000 to $70,000. However, that is not the case. In fact, the premium came down across almost all ages and it is partly due to longevity i.e. Singaporeans are living longer and have better mortality rates now.

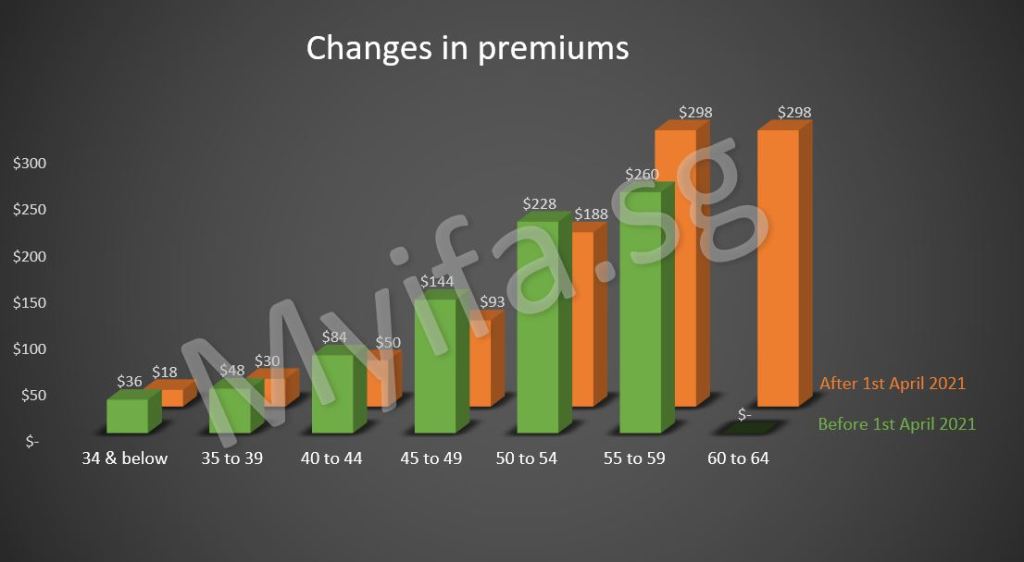

Let us look at how much the premium for DPS had decreased.

We shall use the DPS premiums for a insured age 45 as an example, it could cost $144 to cover a insured member for $46,000. The cost of insurance is about $3.13/thousand and for someone age 45 with the reduced premium, it will cost only $1.32/thousand which is about 2.3x cheaper! You can look at this decreased of premium in two ways.

- To get the same amount of $46,000 base on the revised premium, you need about $60 instead of $144

- With the same premium of $144, you can get about $190,000 of coverage instead of $46,000 based on the revised premium.

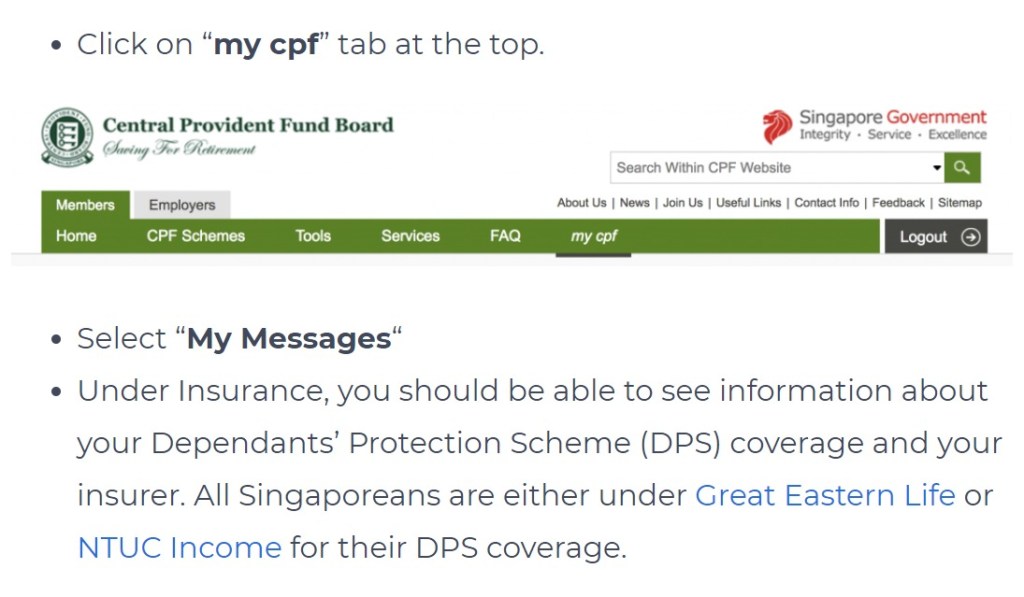

This trend of cheaper premiums for death coverage is commonly seen in term insurance as well. When we conduct a policy review with our clients, we saw term plans that were bought years ago could be more expensive as compared to one with the same amount of coverage now. One exercise I did with my clients while I was reviewing their coverage together with DPS is their DPS Nomination which is separated from your CPF Nomination. If your existing DPS is administered by NTUC Income, you will get a letter from Great Eastern Life informing that your nomination made will be void and you need to make a fresh nomination for your DPS with the attached nomination form. I had encountered a few clients who were under NTUC Income but (it could be due to administration oversight) they did not received the nomination letter. For those who are already with Great Eastern Life, there is no need for you to do anything. To check if you are currently under Great Eastern Life or NTUC Income, you can log in to your CPF using the steps below.

Step 1 : Log into CPF Website

Step 2 : Check the insurer.

If you need any help or have any questions on DPS, just whatsapp or drop me an email for assistance.

1 Comment