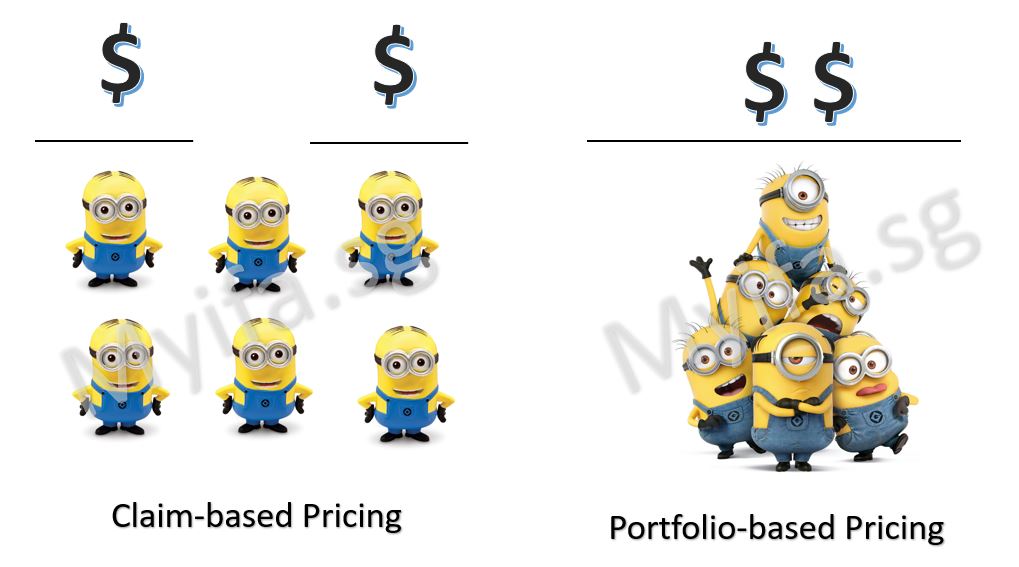

There are generally two methods when it comes to premium pricing for insurance and they are either Portfolio-based or Claim-based. In a portfolio-based premium pricing method, the premium will be reviewed based on the entire portfolio’s total premium and total claims. If there are losses to the portfolio, the insurer can revise the premium upwards. Likewise, if there is a gain, the insurer can revise the premium downwards or refund the extra premiums to the policy holders. In short, any change in premium rates will apply to all policyholders of the same plan. To cite some examples, SAF Term plans and Dependent Protection Scheme are insurance plans that are priced based on portfolio underwriting. For claim-based pricing, the premium will be determined based on the individual’s claims experience. The more you claim, the higher the premium. And of course, the premium will be lower for policy holders who had smaller claims and there might be premium discount for those who did not make any claim. One example is our motor insurance that comes with No-claim discount.

A simple illustration of claim-based and portfolio-based pricing is shown below.

The way the premium is priced between a claim-based and portfolio pricing method is similar except in a claim-based pricing model, the policy holders will have to pay an additional premium depending on their claim experience. The advantage is the policy holders may pay a discounted premium if there was no claims made. There are policy holders who prefer this method of pricing as they think it is a fairer pricing approach. On the other hand, there are policy holders who prefer portfolio-based pricing model because insurance is pooling of risk and the risk should be shared by all equally. We shall discuss about claim-based pricing since majority of the policy holders are less familiar with it and we shall focus on integrated shield plans.

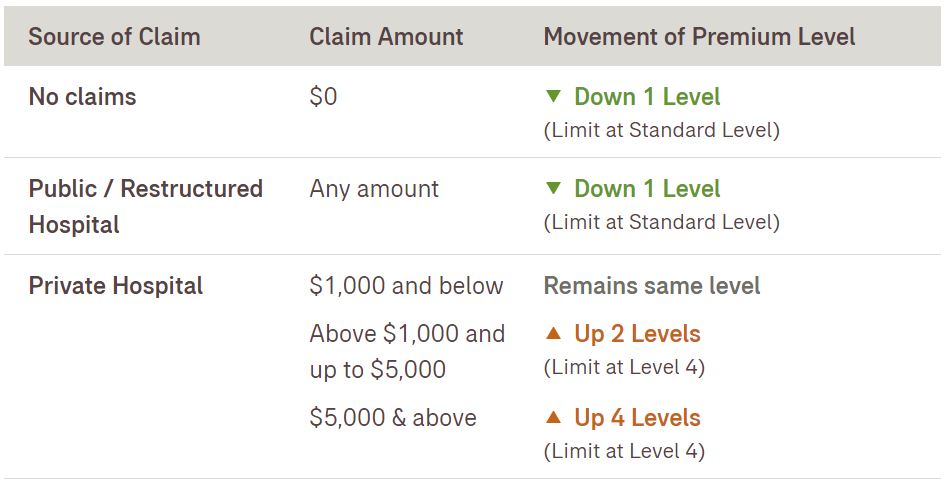

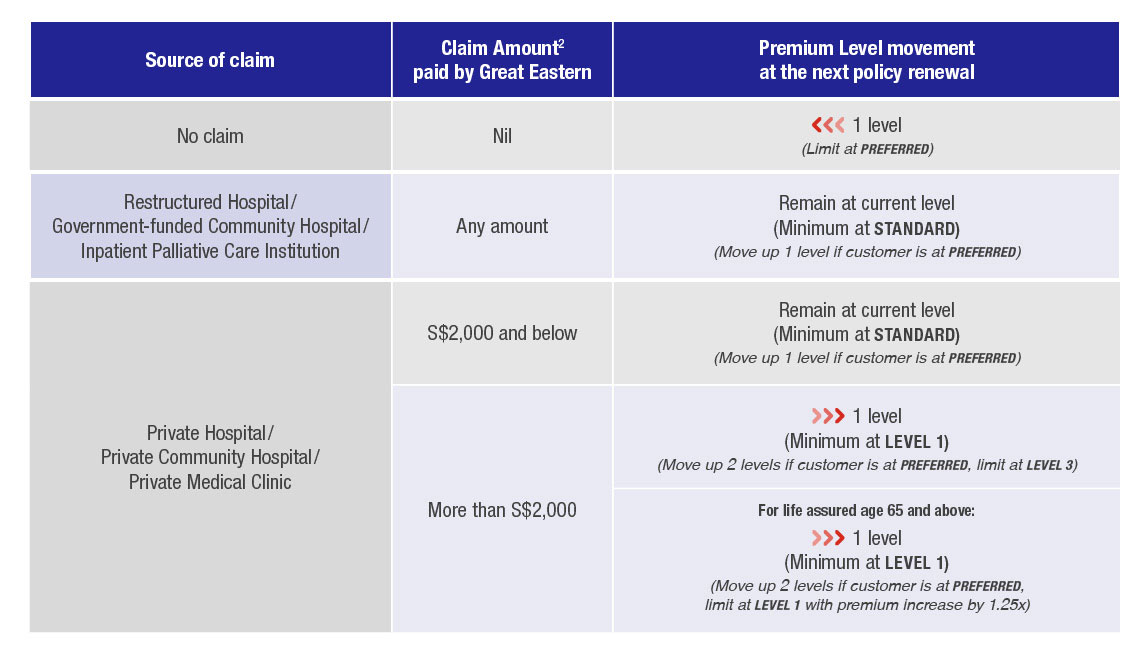

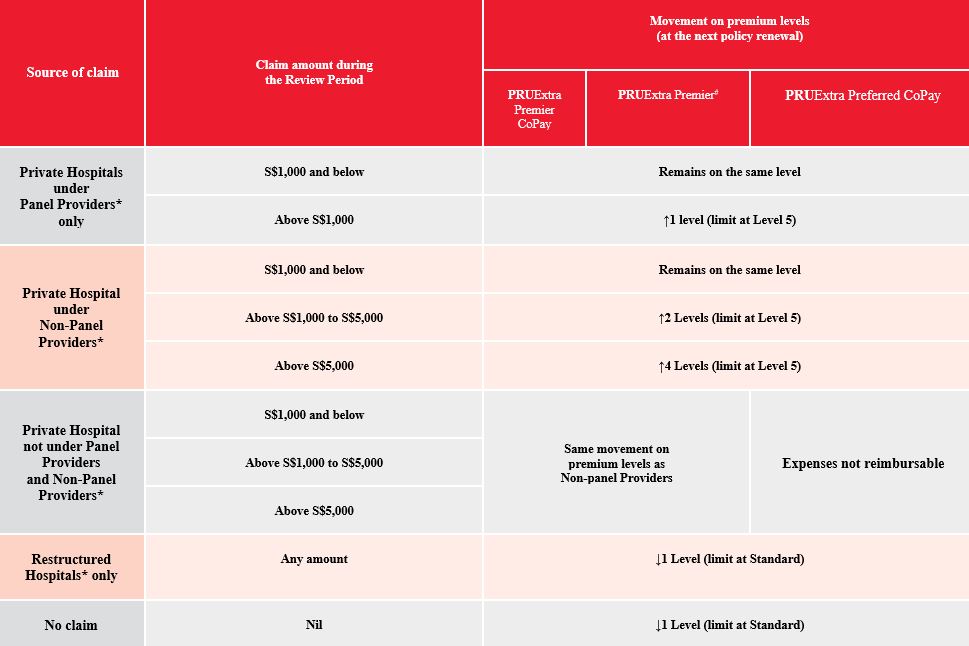

In a claim-based pricing model, the factors that determines how much additional premium the policy holders depends primarily on

- The source of claim

- The amount of claims made

- The premium level movement

There are three companies that had implemented claim-based pricing but it is not subjected to all the plans. Those affected are

- AIA VitalCare

- PRUExtra Premier CoPay, PRUExtra Preferred CoPay, PRUExtra Premier, and PRUExtra Plus

- GREAT TotalCare (Elite-P) and GREAT TotalCare (Classic-P)

Each of them has their way of assessing the premium level movement which are shown below.

Let us do a quick exercise. Choose any of the insurers above and look at its chart for 5 minutes.

There are different ward types such as Government or Private Hospital – Panel or Non-Panel Specialist and the amount claimed will determines the movement level your premiums. The premium movement level, of course, indicates if your renewal premium is at discounted rate or a multiplier of 1 to 3 times depending on the insurer.

Now, assuming you seek treatment with a Non-panel Specialist in a Private Hospital and without referring to the insurer’s chart that you had seen 5 minutes ago, can you tell me what is your increased premium if you were at Standard Level and claim $2,500 and $3,000 respectively? You can check the table to see if your answer is right or wrong. A claim-based pricing model can be complicated to the consumer as we can see from the above charts and table. From a representative point of view, the difficult part of our business is not at the point of sales but at the point of claim. The exercise you just did had illustrated it is not easy to remember the premium movement as well as criteria after a short 5 minutes. How much the client is likely to remember the benefits or policy terms especially after months or years of inception?

In my humble opinion, the pricing of insurance lies in the responsibility of the actuarial. If the over-price a product, the insurer will lose the market share. If they underprice it, the company loses money. Logically speaking, if an ISP does claim-based pricing, the premium should be much lower than a portfolio-based priced ISP since the actuarial had indirectly transfer part of the risk to the individual. One of the major increased in premium is when a policy holder turns 40 to 41 and I shall use this age band for discussion. I would first highlight that I am not comparing which is the better ISP. The premiums should be be the only consideration for getting a ISP and we should look at the benefits too. The following is to look at the two models of pricing from a consumer point-of-view. I am using a random two plans from each of the pricing model for discussion purpose.

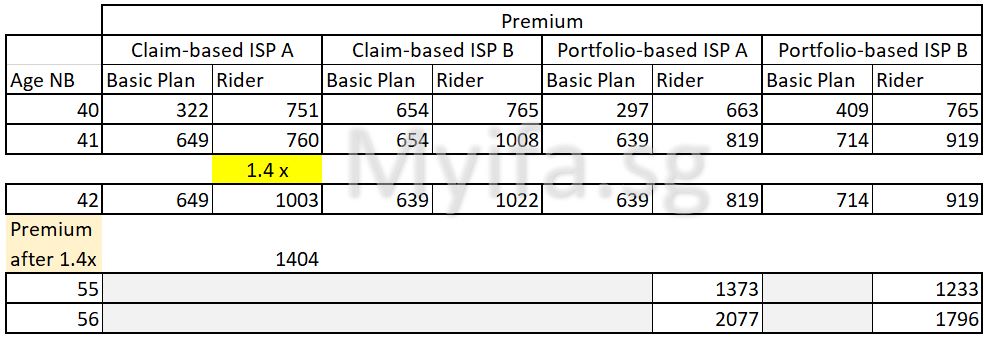

I spoke with some people who claimed claim-based model will result in lower premium because the risk is spread to the claimant. We will look at the rider’s premium since only this portion will be affected by the level movement when a claim is made. The question is by how much lower are the premium, if any?

Next, I am using the Claim-based ISP A for illustrated as it is lower priced than Claim-based ISP B. The movement across the different ISP varies and I am using 1 Level at 1.4x for ease of illustration. Assuming I am currently aged 41, my renewal premium at age 42 is $1,003 if I did not make any claims throughout the year. However, if I had made a claim of $2,000, that resulted in my premium moving up from standard to Level 1 i.e. 1.4x, my renewal premium at age 42 will be $1,404 (1.4 x $1003). The premium, based on the higher of the 2 Portfolio-based ISP, will still be lower than $1,404 regardless a claim is made or not. If I am on a Portfolio-based ISP, it will take me more than a decade when I reach 55 to 56 for my premium to reach $1,404. That is, of course, on the assumption premiums are not revised.

I have no statistic of the policy holders each insurers have in their ISP who will turn 41 to 42 but I think to assume 50 is a very safe number. If 10% of these policy holders were to claim an average of $3,000 for the medical bills, that’s a total of $15,000 paid out by the insurer. The insurer can spread out this $15,000 over 50 policy holders and the premium at age 42 will increase from $1003 to $1303 instead of $1,404 by an individual. To be fair, the calculation is not as simple as this because there are many other factors. However, this is what insurance is about – Risk pooling!

One of the most logical thing I would do as a policy holder is I will not claim a bill that is below $2,000. We may have to re-think again… what is the real advantage of Claim-based model? Is it to to reduce premium or to reduce claims. While the objective may be similar which is claim control, one model is pro-company while another is pro-consumer.

To conclude, I am not against claim-based model. It is a better approach in an employee benefit policies where a particular company made significantly higher claims than others. I prefer this model under such situation where the loading is on the company than shared by all companies in the portfolio especially those which had made no claims. However, we need to understand that when this risk is transfer to a company, that is a population of staff and still not on individuals.

Hi, maybe there’s some error for prudential. It’s 20% discount before standard level. Not 10%

LikeLike

Thanks for highlighting. Amended to 20%.

LikeLike