On the 2nd May 2021, a judgment was passed for an accident that happened in 2014. The payout amounting to $13.6mil is believed to be the highest for a bodily injury claim so far.

Questions started to flood my whatsapp. The two main questions were

1) Why is there such a huge amount of payout?

2) Who will pay that sum of money?

Let us look the the first question of how the court determines a payout amount in situations of death or bodily injuries. In a situation where the accident resulted in death, the basis of judgment is based on current age of the victims, the possible number of years he could had worked and his potential income loss based on promotion or pay increment etc. If it was bodily injuries, the payout is usually much higher. In addition to the considerations in a death payout, other cost of living for the victim such as medical cost, cost of employing a care giver and other reasonable cost will be added on.

Now, to the more crucial question. $13.6 million! How are we ever going to pay that sum of money and who will pay for it?

Most of us knew that it is mandatory to have a Motor Insurance in place before the vehicle can be on the road. There are three types of Motor Insurance and the coverages are as follow:

Third Party

- Death or injury to other parties

- Damage to other parties’ property

Third Party, Fire and Theft

- Death or injury to other parties

- Damage to other parties’ property

- Fire damage to, or theft of, your vehicle

Comprehensive

- Damage to other parties’ property

- Death or injury to other parties

- Fire damage to, or theft of, your vehicle

- Accidental damage to your vehicle

- Windscreen damage

- Damage arising from riot, strike and civil commotion

- Personal accident cover (private car only)

- Medical expenses (private car only)

The driver also has the option to add on other benefits offered by the insurance companies. By law, the mandatory requirement is a Third Party Motor Insurance. And if you are still paying an installment for the vehicle, the finance company will very likely asked for a comprehensive Motor Insurance.

By now, you will know the motor insurance will pay for the damages. However, you might be thinking if the insurer will pay in full or have a cap to the payout? What happens if it is not paid in full? We need to first understand which section of claim does this $13.6mil falls under. This is a Third party liability claim and in a motor insurance, a liability claim can be categories into either

- Damage to other parties’ property

- Death or injury to other parties

An example of damage to other parties’ property is the Tanjong Pagar car crash accident. Assuming this is an claimable event and the owner of the shophouse claim against the driver, the insurance company will pay base of the benefit under this section. Depending on insurance companies, the limit for damage to other parties’ property benefit is usually $5 million. In this accident, it was a bodily injury and there is no limit when it comes to third party liability for death or injury to other parties which means the insurance company will have to pay the $13.6mil in full assuming that is the final judgement by the Court unless there are reasons not to do that.

The fact is no amount of money will be a fair compensation to the victim’s family but regardless of amount, it will ease the financial burden for them. The insurance payout will not remove the emotional loss but it helps to mitigate the financial loss. Imagine there was no insurance in place, most likely the victim’s family will have to sue the driver for the damages which is likely to be futile and destroyed another family financially.

Thus, I am in to have bicycles or other types of portable mobility device like e-scooters to have mandatory insurance. There are many obstacles to get this implemented. For e.g. do we then need to license bike first? Can the riders pay the premiums? Does a child on a children 4-wheeler children bike also need purchase an insurance? These are the ‘How’ to get it going and before we go into this discussion, we should first look at the ‘Why’. Why do we need an insurance for bicycles and PMD or Why we can do without an insurance for these road users? Let us discuss that first and if we see the need to have it, then we can crack our brains how to implement it.

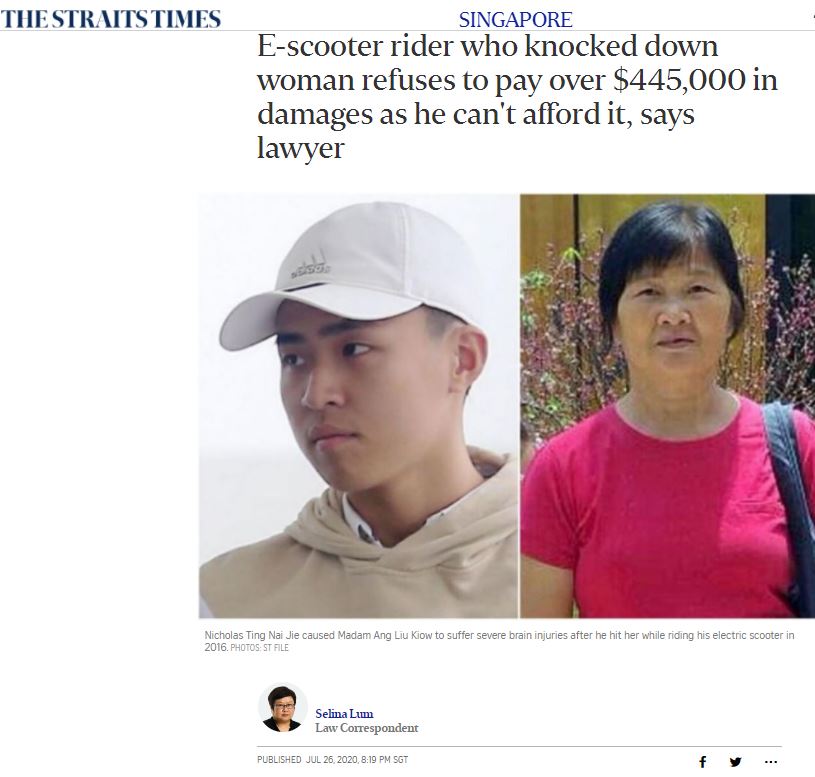

It is not because representative can make more money to sell these insurance but look at the accident of Mdm. Ang Liu Kiow who suffers from brain injury after she got hot by an e-scooter.

Despite being awarded $445,000 in damages by the Court, the rider says he cannot afford it. His lawyer said the rider cannot afford even if it was just half the amount and the victim cannot recover any money from him because he has no assets.

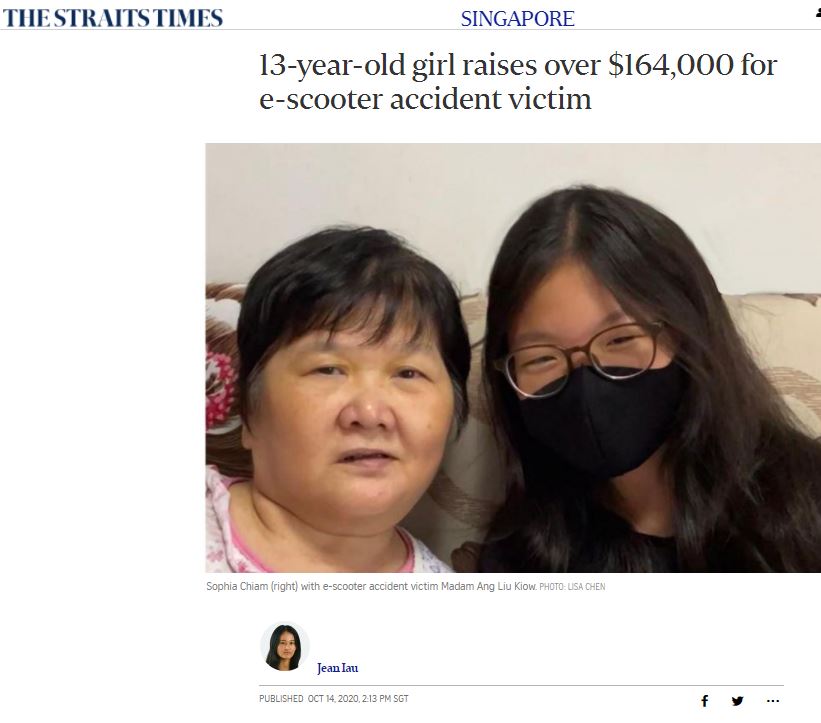

Thankfully, there was this kind 13-year old girl who did a crowdfunding for Mdm. Ang and raised over $164,000!

No victim should go thru these stress and, in my humble opinion, it is a joke to walk away with any attempt of trying to compensate the victim. There are also responsible riders or PMD users who read about my article and took their initiative to protect themselves against personal liabilities on these mobility devices.

To conclude, Be safe! Be responsible! Regardless you are a cyclist, driver or pedestrian.