The Risk-Based Capital (RBC) framework was first introduced to insurance companies in Singapore back in 2004. RBC adopts a risk-focused approach to assessing capital adequacy (CAR). A more comprehensive and risk-sensitive framework known “Risk-Based Capital 2 (RBC 2) framework” was introduced in March 2020 to enhance policyholder protection and ensure insurers can perform its operation on a sustainable basis. One of the changes in RBC2 was to raising the CAR from 120% to 130%. This means that MAS would trigger a supervisory action if the insurer’s CAR falls below 120% but today, falling below 130% will trigger the supervisory action from MAS. What this means is the insurer needs to hold more cash to enhance policyholder protection through through the matching of cash inflows received through investments with the expected liabilities of the insurer. The liabilities could be in the form of claims, policy maturity, surrender values etc.

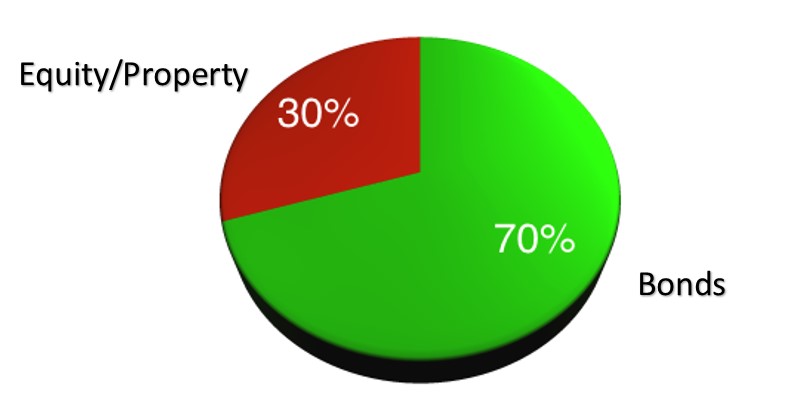

Our current participating funds(par fund)are under the RBC framework. To achieve an average 4.75% p.a. return on the par fund, the insurer typically invest the funds in the 70/30 allocation as seen below.

The bonds are a mixture of government bonds that gives around 2.5% p.a. and investment grade corporate at estimated 4% p.a. The equity/property investments are expected to give 8% p.a.

These are examples of some insurers and their allocation of investment mix. Do note that there is a targeted investment mix and an actual that will change over time according to the market. These information are available in the product summary.

Without going into the details which can be quite technical, the par funds are also hit by COVID-19. For example, the Singapore Saving Bond interest rates over the years even before COVID-19. These are likely to be one source of investments that pays the guarantee portion of the par fund. With the rate going down over the years, we do expect the guarantee portion of the par funds may be lowered as well. And knowing the fact the investment returns will be weak in the coming years, the equities that generate the non-guarantee portion of the policies will be reduced as well.

Think about it this way, you have $100,000 to invest in the past to generate a return of $4,750 but now, you only have $90,000 to generate the same $4,750. Even if the investment environment is as good as before, a lower capital will require a higher investment returns to generate the same amount of dollar. With a weaker market now, it makes the job even harder.

In my humble opinion, the possible changes in the insurance industry are

- Less capital will be invested because the insurers needs to hold more cash to satisfy the CAR requirement.

- Reduction on the non-guaranteed portion of bonuses for existing policies and those issued before RBC2 due to COVID-19 and the weak market. In fact, there are insurers which had already taken the approach to cut the reversionary bonuses and I think there will be more to come.

- The policy illustration on the benefit illustration was illustrating at a investment return of 3.75%-5.25%. It was reduced to illustrated returns of 3.25%-4.75% which is reflected in the current benefit illustrations. These figures are likely to be reduced further for participating policies in future with these changes in place.

If you are in a position or have plans to make any purchase of insurance may it for protection or saving purpose such as education or retirement planning, it might be better to do it now than the newer plans are launched under RBC 2.

This post was made for information purpose and may not be as detail as I hope as the technical details can be confusing for some. You can check the links if you want to know more about RBC and RBC 2. You can also speak to your financial adviser representative or drop me an email if you need any assistance.

2 Comments