You might had heard of insurance agents asking you to make your purchase of insurance policy with critical illness benefits as soon as possible. The reason is with effect from 26 Aug 2020, there will be a new definition for the critical illness benefits known as “LIA CRITICAL ILLNESS (CI) FRAMEWORK 2019“. Is there a need to rush into buying before the new definition kicks in? Let us look at what are the changes made and make an informed decision.

Who will be affected?

For Individual Policies

- New CI products introduced before 26 August 2020 may adopt either Version 2014 or Version 2019 definitions. If the insurer chooses Version 2014, the CI product must be withdrawn by 26 August 2020.

- The application of Version 2019 definitions will be based on the Proposal Signed Date.

- For proposals that are signed by 25 August 2020, insurers must ensure that the policies are issued no later than 25 February 2021*. This gives insurers a grace period of six months to issue all such policies under Version 2014 definitions.

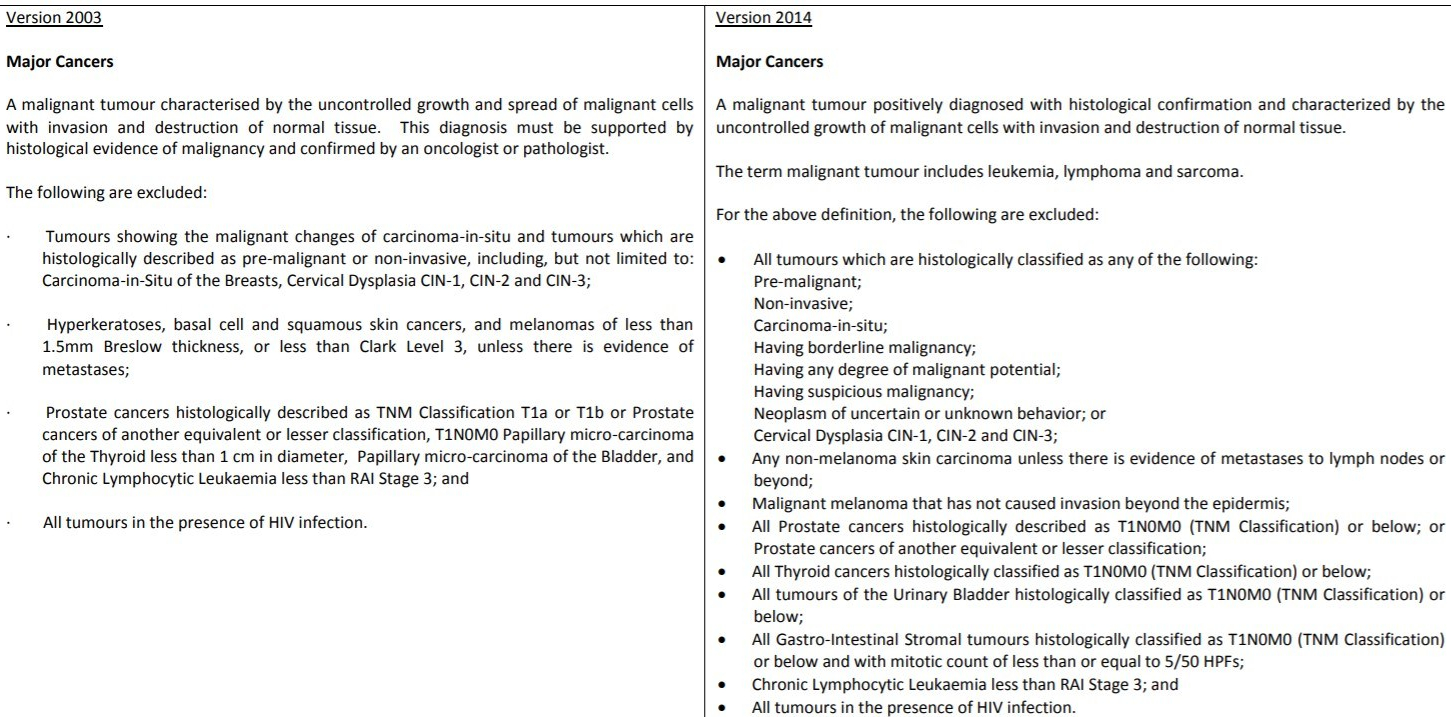

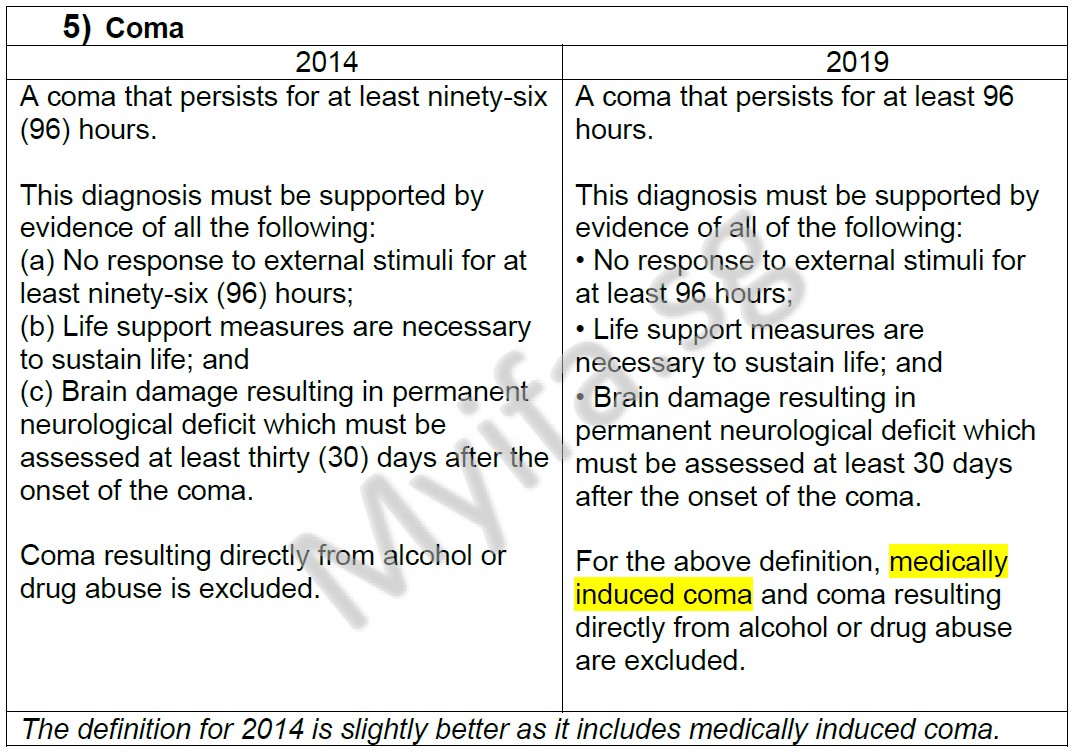

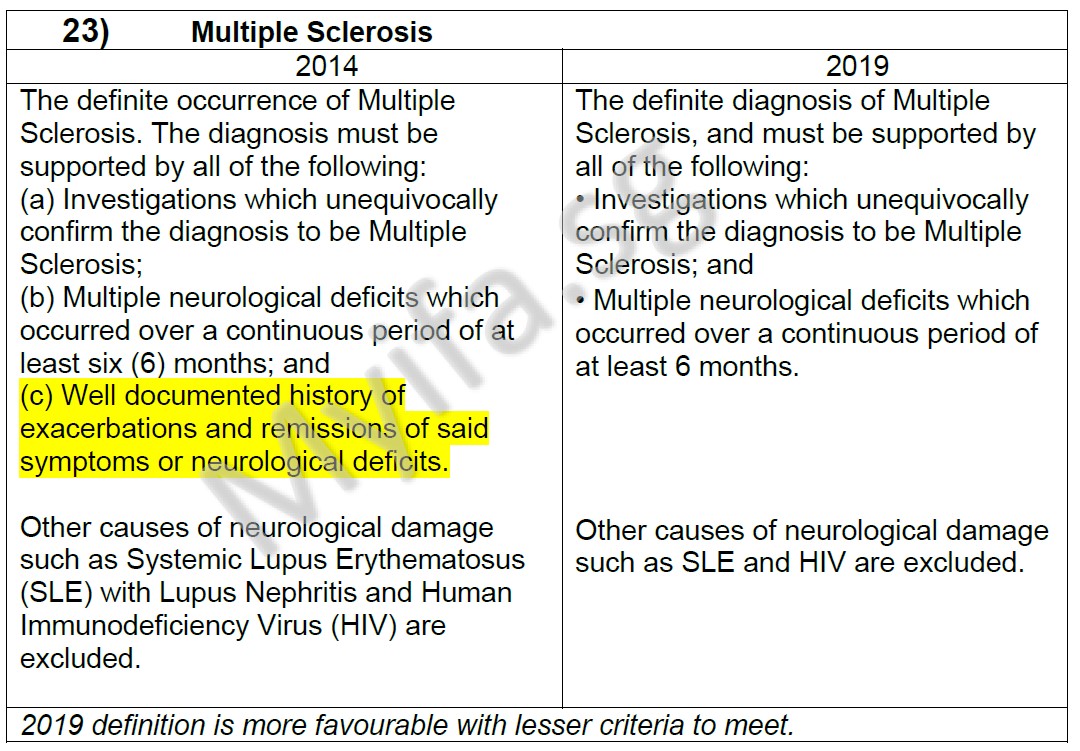

This is not the first time the change was made. The current critical illness definition was revised in 2014 from the 2003 definition. Below is an example of the change from 2003 to 2014 definition for Major Cancer.

These changes are necessary with new medical testing that is available now that may lead to ambiguities if a claim is made. Some changes may set more criteria to make a successful claim, to have more exclusion and some illness had extended the scope of coverage.

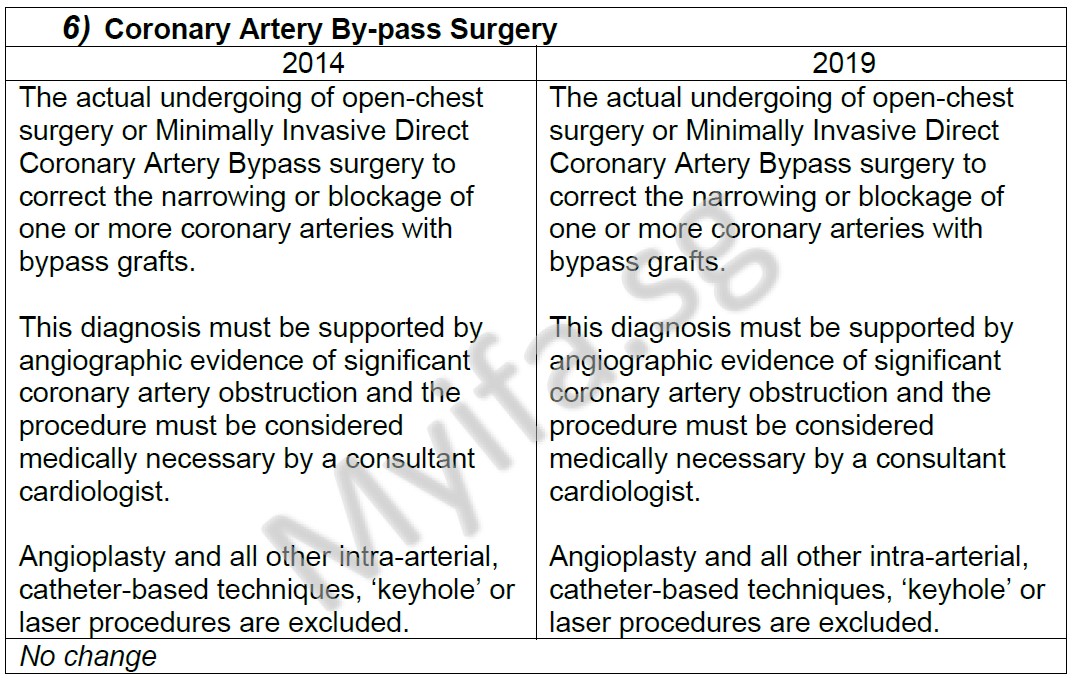

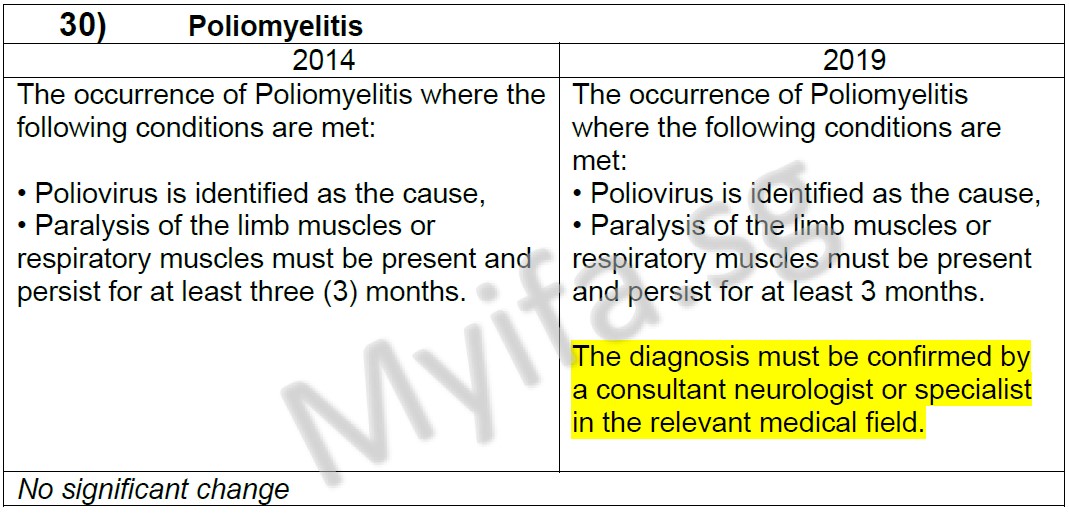

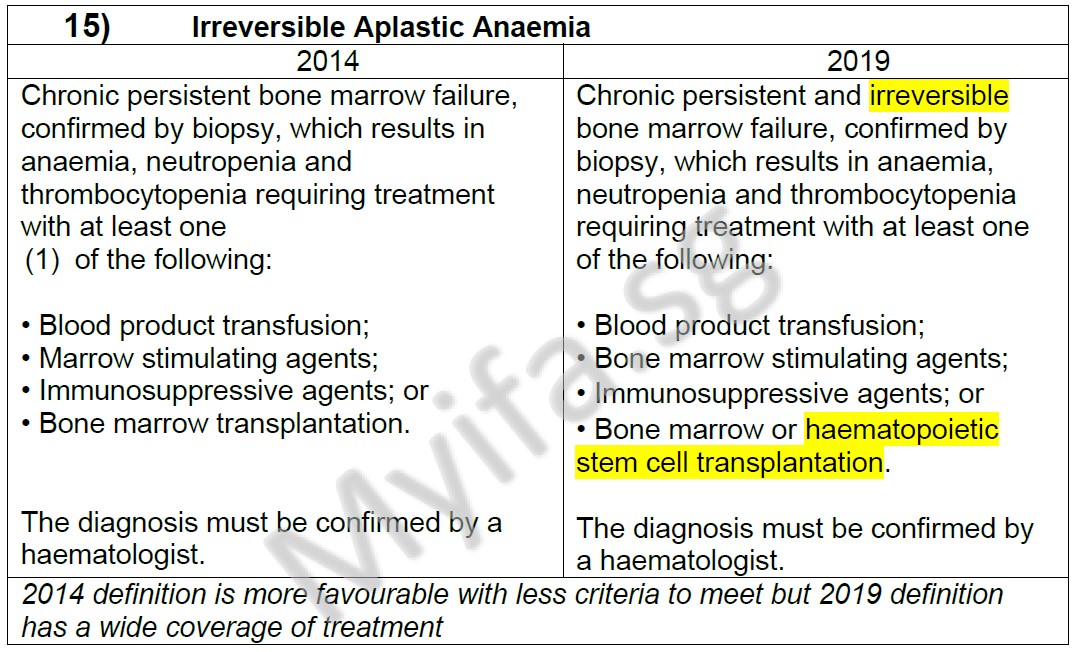

For the change from 2014 to 2019 definition, I had broadly classify into

- No change

- No significant change

- One more favorable than other

For e.g.

No change

No significant change

2014 is more favorable

2019 is more favorable

For the full 37 definitions, you can download CI List 2014 vs 2019 .

2 Comments