You are likely to hear from your financial adviser representative the insurance company will underwrite your application if you had applied for any life insurance. Underwriting is the process an insurance company evaluates its risk. In this article, in specific to a person’s health or life. This process helps an insurance company to determine the amount of additional premium, known as loading, to be charged to the applicant for taking on additional risk if the person has certain pre-existing medical conditions prior to the insurance application. For instance, we know the chance of a person with obesity and suffering from hypertension will have a much higher chance of making an insurance claim compared to someone who has good BMI reading with no medical conditions. You might had to answer to a question similar to the one below when you were applying for your insurance.

“Have either of your natural parents or any siblings died or suffered from cancer, heart disease, stroke, high blood

pressure, cardiomyopathy, diabetes, kidney diseases, mental disorder, tuberculosis or any hereditary disease?

If yes, please provide details below.“

The above medical question is meant to find out an individual’s family history of medical condition. It raise a red flag to insurers when there are one or more parents or siblings suffering from the same medical condition especially if the condition was diagnosed before age 60. A common scenario is a female applicant being loaded with extra premium for her insurance application although she has no symptoms of breast cancer but because her mother has breast cancer or having the condition being excluded because her siblings also suffered from breast cancer. This method of underwriting has caused many unhappiness with clients and financial adviser representative often need to appeal on these unfavorable terms.

With effect of 27 October 2021, life insurers will implement the ‘Moratorium on Genetic Testing and Insurance’ developed by The Ministry of Health (MOH) and the Life Insurance Association (LIA). This moratorium is to support Precision Medicine (PM) in Singapore and aims to prevent individuals from being deterred to undergo clinical genetic tests for any

medical indications and/or participating in PM research due to concerns about insurability. Under this Moratorium, a distinction is drawn between diagnostic genetic tests and predictive genetic tests.

| Diagnostic genetic tests | Predictive genetic tests |

These tests confirm or rule out a diagnosis based on existing symptoms, signs or abnormal non-genetic test results which indicate that the condition in question may be present (i.e. testing in symptomatic individuals). | These tests predict a future risk of disease in individuals without symptoms or signs of a genetic disorder (i.e. testing in asymptomatic individuals) |

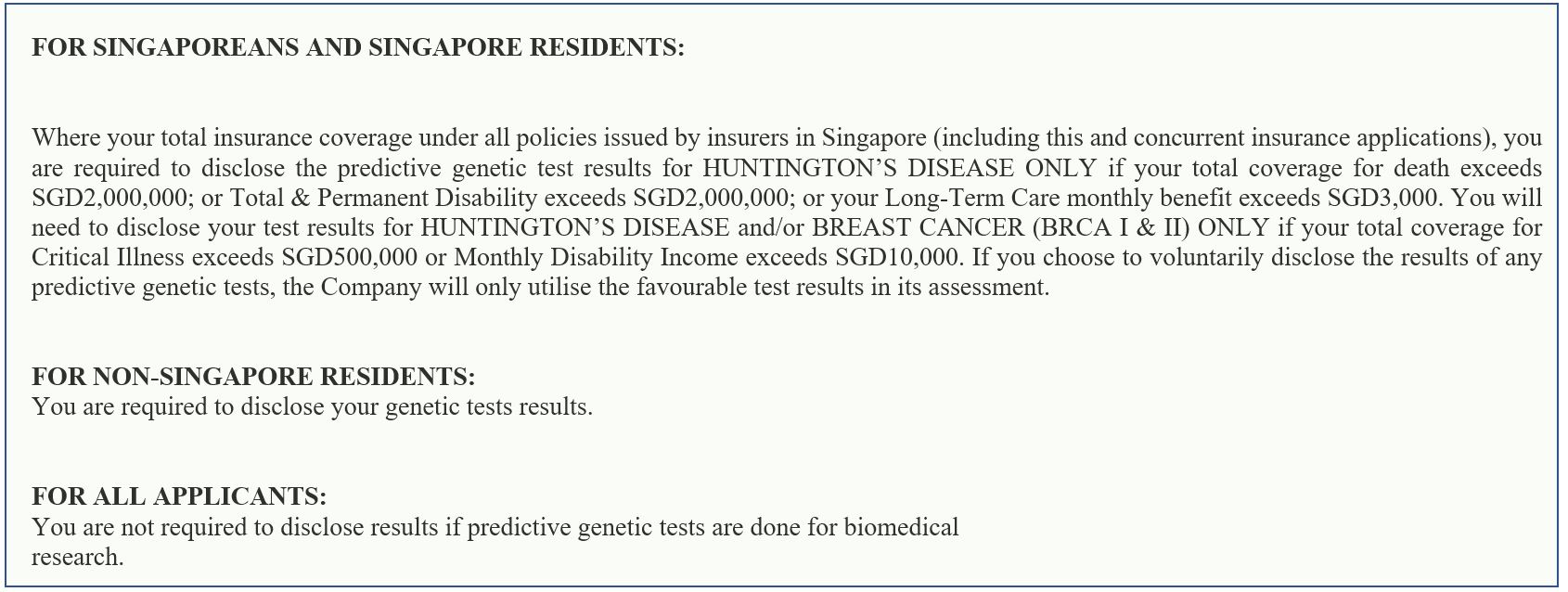

Life insurance companies in Singapore are not allowed to ask insurance applicants for their predictive genetic test result, if they had taken a test, and are not allowed to use the test result when assessing the applicant’s medical profile. The moratorium will effect on insurance that provides benefits on the following types of insurance.

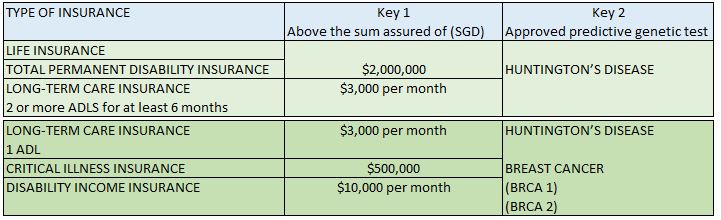

However, the insurer can ask the life insurance applicant who is a Singapore Resident to disclose, and use, the result of approved predictive genetic test(s) which you had taken in the past for assessing your insurance application, or which you may take in the future for re-assessing the terms of the policy after the policy has been issued to you if both “keys” are met under the double-key model.

If a life assured voluntarily declares a predictive genetic test result which is not in the scope of the moratorium and gets a favourable genetic test results, insurers may use such result for underwriting. However, if the genetic test results are unfavourable, insurers cannot use such result for underwriting. What these means to you is this change put the life assured in a better position when he/she is applying for an insurance application.

In conclusion, you will see the Preamble clause in the application forms after 27 October 2021 that states