This post will start a series of my job as an Independent Financial Adviser(IFA) and the planning process for my client.

Let me first clarify that regardless one is a tied or independent agent, I believe everyone will plan for the benefit for the client. In no way is my post suggesting that an IFA is better than a tied agent or vice versa. I have been reading some post that as an IFA which we represent multiple companies is not an advantage to the client because we will just sell the plan with the highest comission or premium and I see the need to dispute such comment.

Before I continue, I need to emphasis that when it comes to insurance planning, premium should never be the only factor to consider. The benefits and features are also important for comparison. However, I will use premium as a basis of comparison for this post. We will keep the comparison of benefits and features for future post.

Prior to an recommendation is made, all Financial Adviser Representatives(FAR) need to conduct a need-based analysis to ascertain the amount of coverage gap for the client. For illustration purpose, I am assuming this particular client needs a Whole life with critical illness of Early, Intermediate and Advanced stage. I am not sure how other FAR works but below is a comparison I will show to every client before narrowing to a few options. As mentioned, we will use premium as a base comparison in this post. Do note the figures below is for a particular age only. The “best” company for this age could be the “worse” for another age group.

The variables have to be the as similar as possible to have a close comparison.

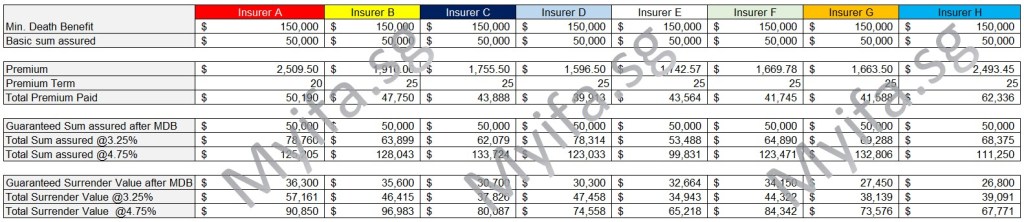

| Basic Sum Assured | $50,0000 |

| Multiplier | 3x |

| Minimum Death Benefit | $150,000 |

| Premium Term | 25 years (except Insurer A) |

Different clients have different priorities of concern. Quite clearly, if one is concern with premium, Insurer D offer the lowest premium at $1596.50 annually.

Another client may be concern with the coverage after the minimum death benefit drops. If we look at the total sum assured illustrated at 3.25%, we can see Insurer A($78,760) and Insurer D($78,314) are having a close fight. We may have to look at the premium again and decide which is the better choice. The illustration at 4.75% will show different insurers with Insurer C($133,724) and Insurer G($132,806). A common question by the client is should we look at 3.25% or be more optimistic to look at 4.75%. Here’s a little tips to that question.

Now, although Insurer A has one of the highest annual premium, we need to be clear that it has only a 20 years premium term and Insurer A did not have the highest total premium paid. Insurer H have the highest total premium paid that can also be translated to be the most expensive policy but there are reasons to it and we will discuss this in future when we go more into the benefits and features. For another person who wants the option to terminate this policy in future when the dependents are financially free may want to look at the surrender value and similarly, we look at the 3.25% and 4.75% projection. This time you realised Insurer B can be a strong contender.

So… back to the comment that an IFA will sell the policy with the highest comission or premium. Can we do that with this comparison table? You decide.