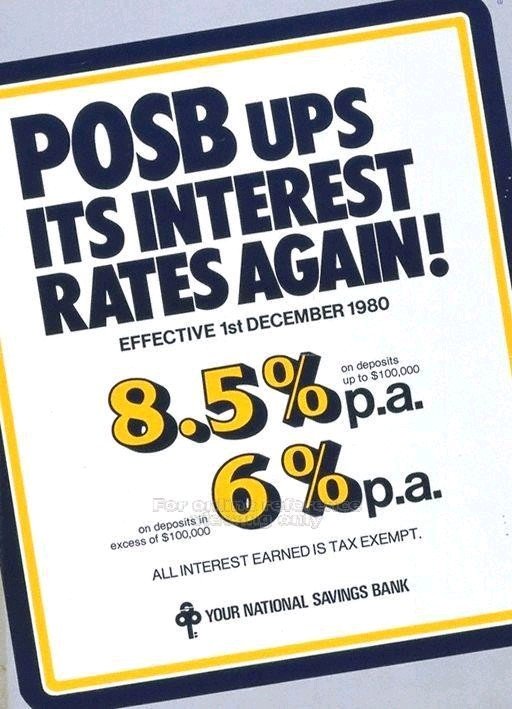

I have been seeing the photo below these few days. I guess it is no less than 10 times that it appeared on my Facebook and other social media notification.

The photo above shows the interest rates getting as high as 8.5% back in 1980. And looking at the current saving interest rate of less than 1%, many would had wished we grew up in that period. But is it really that wonderful?

I had used this photo to teach financial literacy to students on “saving rate vs inflation rate” about 5 years ago. And just to “add oil to fire”, while many are trying different CPF Hacks to get the maximum return on your CPF, the interest rate on your CPF Ordinary account back and Special account back then was 6.5%!

Now, let us go back to the saving interest rate. While the 8.5% p. a. on your saving account look fantastic in today’s low interest rate environment, we have to look at the inflation rate during that same period as shown below. As we can see, the inflation in Singapore during 1980 was 8.53%. So think again, is having that 8.5% high?

After so much of figures, you may be thinking…

The point I’m trying to put across is at any point of time, the saving rate will never be better than inflation. You can put your emergency money and some liquidity in a saving account or fixed deposit but you are not doing yourself any flavour if you keep your funds for long term plans such as retirement in the same instrument.

It is common to hear people not investing because they cannot take the risk. That is totally understandable as one can win or loss in investment and there is no sure win investment. However, by not investing, you subject yourself to inflation risk and that is a sure loss.

What is inflation risk? To put it simply, let us assume the inflation rate in Singapore is 3% and the bank saving rate is 1%. That means our net return is -2% and for every $100 that we keep in the bank will be worth $98 at the end of the year. You can imagine how much your $100 will be worth after 10 or 20 years. The depreciation to the spending power of your money due to inflation is inflation risk.

As an individual, you may have to decide if you want to face investment risk which is manageable through proper planning or live with inflation risk that is beyond our control.