In my near 20 years in the financial advisory business, one of the most common complains by policy holders is that they were cheated by the insurance companies. It could be in the chance when a claim was submitted and being rejected or the insurance company did not pay the maturity amount as promised. In this post, we shall just focus on the latter. Are insurance companies really cheating the policy holder’s money? Let’s find out!

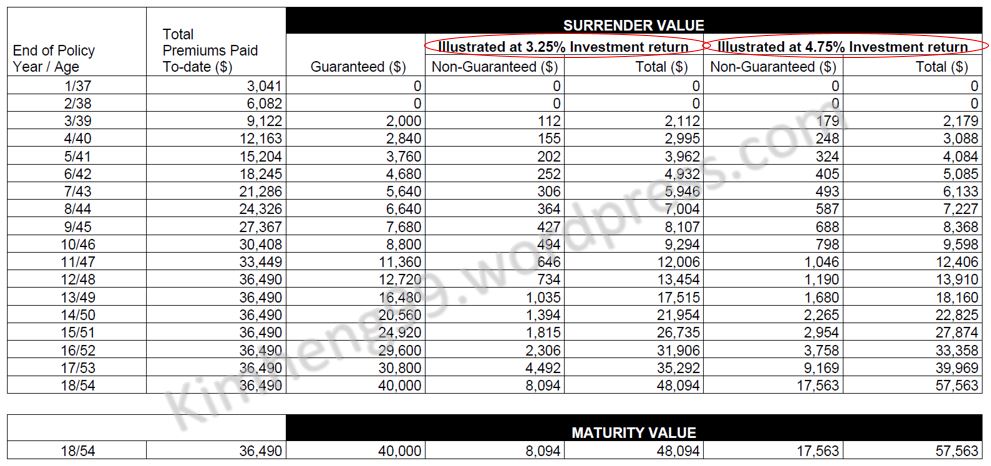

When a Financial Adviser Representative(FAR) proposed a plan to the client, he needs to show the benefit illustration(BI). One section of the benefit illustration shows the value of the policy at the specific period of the policy term if he decides to terminate the policy or hold till maturity. This section is the “Surrender Value” as shown below.

Monetary Authority of Singapore(MAS) requires all insurance company to illustrate the surrender values base on two investment returns i.e. 3.25% and 4.75%. This illustration often lead to many misunderstanding because the investment returns refers to the returns on the participating fund of the insurance company but many policy holders (and sometimes Financial Advisers) misunderstood it as the return on the policy they had purchased. In another words, many clients expect 3.25% or 4.75% to be the returns for the policy they had purchased although they know the returns consist of the guaranteed and non-guaranteed portion. So, if these two figures are not referring to the returns of the policy purchased, where can we find those figures?

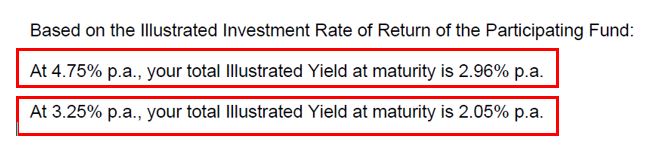

The following statement will be shown in the BI as well.

This statement will give you the indication the return on your policy. In layman terms, it means if the participating fund of the insurance company gets an investment return of 4.75% p.a. , the yield of this policy will be 2.96% p.a. If the participating fund is not doing as well and has an investment returns of 3.25% p.a., the yield of this policy will only be 2.05% p.a. However, do remember that these are MAS mandated illustration and does not reflect the actual returns of investment for the insurers. This means the actual returns of investment might be higher than 4.75% p.a. or lower than 3.25% p.a. and the yield of this policy can be higher than 2.96% p.a or lower than 2.05% p.a.

If there are so many “if”, what then will be more guaranteed? Does it means that whatever is illustrated is useless? The simple answer is no. These figures serves as a guide and we all know the market moves up and down over time and the sames goes for the participating fund for the insurer. If we look at the statement above again, the yield of 2.96% and 2.05% is approximately 60% of the investment rate of return of the participating fund of 4.75% and 3.25% respectively. Does that mean our yield will be 6% if the investment return of the participating fund is 10% in a bullish year? Again, the answer is no. Insurance companies know the investment returns fluctuate over the years. Not only they cannot be consistently hit a 10% return, there will be years when the market is bad and they get negative returns instead. Thus, any excess returns may be held back as bonuses for bad times rather than to pay it out to policy holders. This practice is known as “Smoothing of Bonuses“.

While there is no assurance that bonuses declared will be anywhere near the illustration in the BI, there are legislation in place to safeguard the interest of policy holders. MAS mandates a minimum of 90% of the investment returns must be distributed to policy holder and the shareholders is limited to a maximum of 10%. This prevents excessive distribution of profits to shareholders. Now that the policy holders are protected by legislation, next is to know how policy holders can protect themselves. Do note that each policy have its own pool of participating fund so there is no exact method or way to know how much is the returns of the participating fund but you can have an estimation to know if an insurer can fulfill their promises using a few of the following methods.

The methods are:

- Look at the historical returns of the participating fund.

We all know historical return does not guarantee future performance but this is the best guide to ‘predict’ the expectation for a layman.

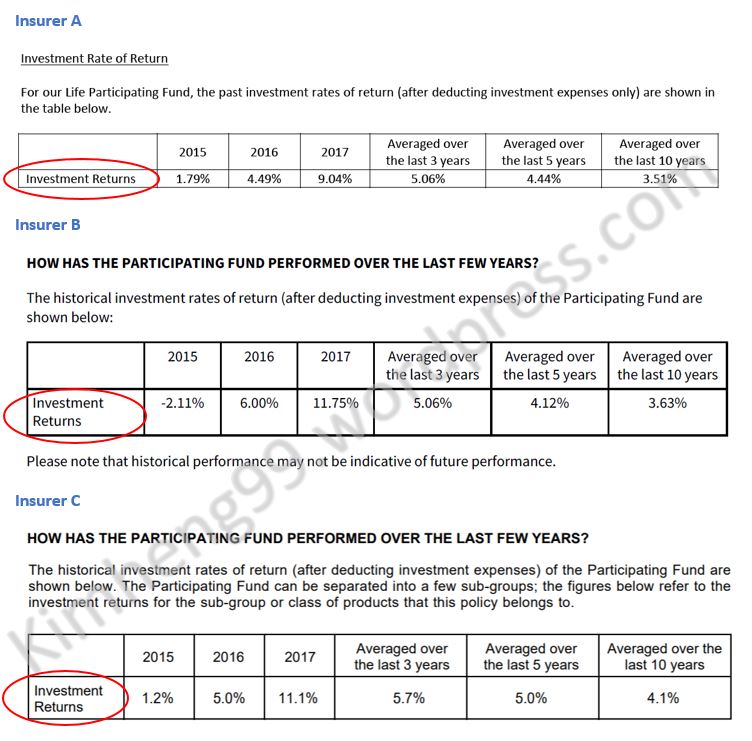

The investment rate of returns of the participating fund are stated in the product summary of the policy. Below is a sample of how it looks from three insurers.

As an informed consumer, we can use these information to consider if we should look at the values at 3.25% p.a or 4.75% p.a illustration. Although none of the above companies achieved an return of 4.75% in the average of 10 years, we can be confident that the illustrated values at 3.25% p.a is very realistic and some of these insurers may pay more than what was illustrated. There are times that an insurer did not achieve even an average return of 3.5% in the long term. In such cases, it might be a bit too optimistic even to look at the illustrated values at 3.25% p.a.

Some of my clients even use this information to decide which insurer they should purchase the policy.

2. Look at the anniversary statement from the insurers.

Insurers are require to sent an anniversary statement to policy holders. This statement will show the bonuses declared on the current year and past years. It will also show the current surrender value as well as the maturity value. You can use these values and compare against the benefit illustration which you had signed when you purchased and see if there are any difference in figures.

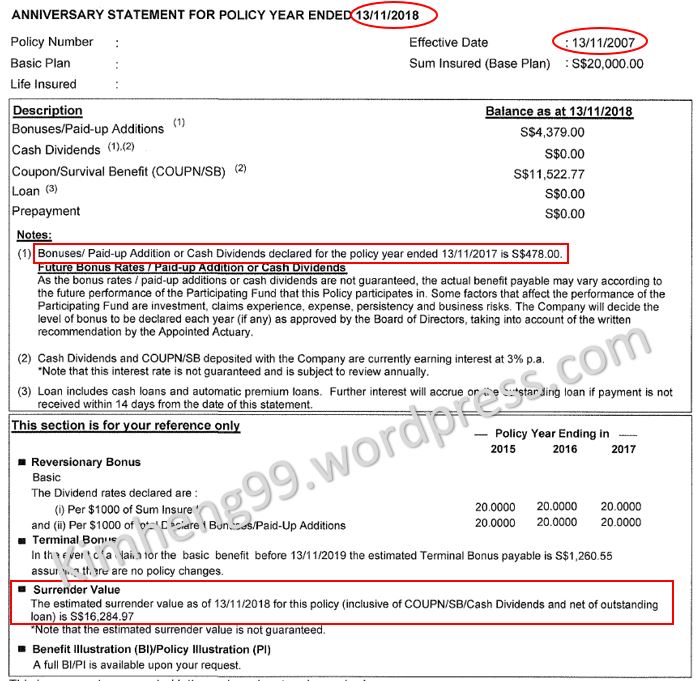

An example of an anniversary statement is shown below. There are many information in this statement and we shall focus on those that are useful for assessing the performance for the participating funds of our policy.

From the effective date, we know the policy was bought in 2007 and this policy statement was in 2018. We can look at the surrender value for the corresponding year in the benefit illustration and check if the value is same, more or less than what is shown in the estimated surrender value in the anniversary statement. Next is to look if the value is closer to the 3.25% p.a. or 4.75% p.a. illustration and you can have a better gauge to your maturity amount. It should be the ideally the same but if the values in the benefit illustration is higher than the anniversary statement, that means bonuses have been reduced.

3. Ask for Post-sales Benefit Illustration

One of the things I will do when I meet my clients for the very first time is to get the post-sales benefit illustration. This document will illustrate the maturity value base on the current projection. What this means is they will take into consideration of any changes in bonuses declared over the years and how the future values will be affected.

It is advisable to ask for a post-sales benefit illustration every 5 years or when you are reviewing your insurance portfolio. You might see a 20% decrease from the original maturity value and in older policies that were purchased before 2000s, a 30% difference is possible.

If that happens, speak to your financial adviser and see how he/she can mitigate the situation. That will be more useful than to have a rude shock and complain that insurance companies cheat people.

“If that happens, speak to your financial adviser and see how he/she can mitigate the situation.”

I wonder how wld the FA mitigate the situation ?

There is nothing that anyone could have done to prevent the decrease or know that a decrease in projected surrender value would happen.

LikeLike

You are right that as an individual, we are in no position to prevent the decrease. There are a few ways an adviser can mitigate the damage in such situation. One way is to find out if there is any negative impact due to the reduction. If there is, is it significant to perform a damage control and what are the options.

LikeLike

This was a good read. I’m just curious about one thing:

“MAS mandates a minimum of 90% of the investment returns must be distributed to policy holder and the shareholders is limited to a maximum of 10%.”

Can I check where is this from? Like MAS website or is it a specific document in my policy documents

LikeLike

Hi CS,

Glad you enjoy the read and it’s good that your ask this lesser known rule. This mandatory requirement is not stated in the policy contracts and yes, you can find the information in various websites such as MAS or the Singapore Statues. It is commonly known as the 90/10 Rule and the principle applies to REITS as well.

For your convince, the following is from an MAS consultation paper “Transfer of profits to shareholders from the Par Fund is restricted to a maximum of 1/9th of the amount of bonus allocated to Par policy owners. This aligns shareholders’ profit objective with Par policy owners’ interests, and takes reference from Section 17(6)(c)(iv) of the Insurance Act (Cap. 142).”

You can check out the Statue for more details. Hope this help.

LikeLike