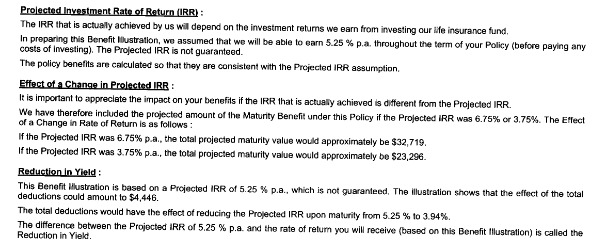

In the process of recommending a financial plan, the more informed clients will asked about the participation funds of the insurer. They want to know the performance of the par funds and in some instances, they want to know the size of the par fund. How important are these questions to a policy holder?

Let me bring up a recent bonus cut by an insurer which surprised many financial adviser representatives(FAR). Why are there still surprises from FAR if they had expected bonus to be cut across insurers because of COVID-19? The reason is because this particular insurer had never cut bonus throughout the major financial crisis in the past years. From the 1997 Asian Financial Crisis to the 2000 Dot Com Bubble and even the 2008 Global Financial Crisis, this particular insurer is the only company that did not cut any bonus for its policies for the past 38 years. You might know which insurer am I talking about by now and most probably you are right. It is Tokio Marine Life Insurance(TMLS) or formerly known as Asia Life Insurance.

With such impressive record, it is no surprise that many financial practitioners are taken aback when TMLS recently issued a bonus statement that it will revise downward the bonus rates for two products. This will affect about 2,0000 policies. Let us first look at the performance of the participating fund of TMLS with other insurer which had announced their par fund performance as to-date.

| Net Investment Return | ||||

| Insurer | 2017 | 2018 | 2019 | Average last 3 years |

| TMLS | 10.55% | -2.51% | 13.05% | 7.03% |

| NTUC Income | 9.04% | 0.82% | 9.59% | 6.48% |

| Prudential | 10.63% | -2.12% | 12.26% | 6.92% |

| Great Eastern | 10.14% | -3.02% | 12.66% | 6.59% |

TMLS had one of the better returns for 2019 and for the the average 3 years, so why did TMLS revised down the bonus? Do note this article is not to justify the revision was correct but before comments such as insurance companies are out to cheat or other conspiracy theories start to flood the market, let me share my view. The two affected policies were removed from the shelf more than a decade ago. Today’s illustrated investment returns of 3.25% to 4.75% is a far cry from what was projected in those days. I am indeed surprise with the action taken by TMLS, not because of the bonus cuts but because they started the cut only now when other insurers have been reducing their bonuses in the past 10 years or more. The point here is TMLS is not short changing its policy holders but other insurers had done the cuts long ago.

Next question – Why are there only 2 policies affected if a revision of rates is needed? Shouldn’t it affect all the participating plans if the par funds are not performing to expectation? Although the performance of the par funds is shown in the benefit illustration, it shows the whole portfolio of the par fund. However, the expected returns and time horizon of products varies from one to another. For e.g. an endowment plan with maturity in 20 years will be very different from a 20 years limited pay whole life. The insurer needs the maturity to be paid for the endowment plan in 20 years but not the whole life. Even if a death claim were to be made for the whole life plan, the money paid will not be from the investment returns thus the premium collected from these 2 plan can be invested differently.

IMHO, one of the better disclosure from participating fund performance report is from AIA. It clearly states which plan is under which product group and the returns for each group. Using 2017 as illustrated below from a AIA par fund report, we can see the returns for the respective group . The reports from other insurers reflect only the net returns of 10.5%. If the policy is under Group 5 that has an returns of 7.7%, do you think the returns of 10.5% matters to him? And those groups that hit 11% or more, should they expect more?

Compared the report below with AIA’s and you can understand why I think AIA has the best explained participating fund performance report. The rest of the companies will reflect similar to the table below which in Singapore context, it is ” Got say like no say”.

The next information made known to the policy holder will be which product belonging to which group.

What is your thoughts on these reports?

Will it be a deciding factor when you want to buy an insurance plan?

Regardless which insurer you had purchased your insurance from, one thing is for sure. The insurance company will not keep the gains from these par funds, give it to the shareholders and declare there are not enough money to pay for the bonuses. MAS is very strict with the distribution of the returns on par fund. It is mandatory to return a minimum of 90% of the investment returns to the policy holder and the shareholders is limited to a maximum of 10%. Having said that, it is always good to do a review of your policies every 2-3 years to ensure your maturity amount is up to your expectation and cover any gaps if required.