” Don’t worry, this insurance company will not go bust. They are rank number xxx in the Fortune 500 list of companies”

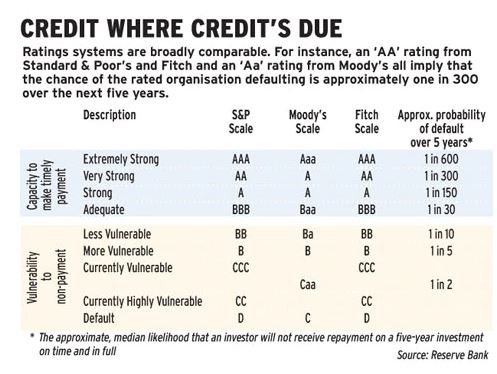

“This insurance company has a credit rating of AA- by Standard & Poor. You can trust this company will not go bankrupt”

How often do we hear Financial Adviser Representative(FAR) making those statement or something similar? What does these credit rating means to you as a policy holder?

As defined in Wikipedia -“A credit rating is an evaluation of the credit risk of a prospective debtor (an individual, a business, company or a government), predicting their ability to pay back the debt, and an implicit forecast of the likelihood of the debtor defaulting.”

Prudential Assurance currently has the credit rating of “AA” by S&P. The lowest credit ratings of insurance companies in Singapore is “A-” and both Aviva and Etiqa are given this rating. The rest are between “AA-” to “A+”. With these credit ratings, does it mean that it is safer to buy a policy from an AA insurance company over one with just “A” rating? Let’s read on to find out.

After the Global Financial Crisis, every insurance company is require to meet the Capital Adequacy Ratio(CAR) of at least 120%. The capital adequacy which falls within the Risk-Based Capital framework was first introduced in 2004 and the latest revision was in 2016. The CAR comprises of 3 components.

1. Component 1 -This component relates to insurance risks undertaken by an insurer. For general insurance business, the requirement is calculated by applying specific risk charges on an insurers premium and claims liabilities. The risk charges applicable to different business lines vary according to volatility of the underlying businesses. For life insurance business, the requirement is calculated by applying specific risk margins to key parameters affecting policy liabilities such as mortality, morbidity, expenses and policy termination rates.

2. Component 2 – This component relates to risks inherent in an insurer’s asset portfolio. It is calculated based on an insurer’s exposure to various markets including debt, equity, property, and foreign exchange. This requirement also reflects the extent of the mismatch between assets and liabilities.

3. Component 3 -This component relates to concentration risks in certain types of assets, counter-parties or groups of counter-parties. It is calculated based on an insurer’s exposure in excess of the prescribed concentration limits.

I will try to explain CAR as simply as I can and I hope I am not misrepresenting it in anyway. For those who wants to understand CAR in details can read up this article by Deloitte . In layman terms, the insurance companies is supposed to derive the amount of possible claims made, policy holders turning up to surrender or take a policy loan from them base on a formula . For example, if a particular insurance company has a potential payout of $10mil due to the situations mentioned above from all its policy holders, the insurer needs to set aside 120% of $10mil as CAR. When an insurer’s CAR falls below 120%, it will result as a “trigger point”. The insurer must notify the Authority and submit a plan on how it intends to bring the CAR back up above the 120% level.

In my humble opinion, a good credit rating of a company is always good but this rating is important if we are considering which company to invest. As a policy holder, the CAR is more important than the credit rating of the insurance company. It is a better indication of how likely you get your money back may it be a claim or upon early termination of your policy if the insurance company is in red. Moreover, should an insurer goes bust, our policies will be covered under the Policy Owners’ Protection Scheme .

Do note that a high CAR may not necessarily means an insurer is more financially secure than the others. Typically, if an insurance main core business is term insurance or policy without any cash value, it tends to have a higher CAR.

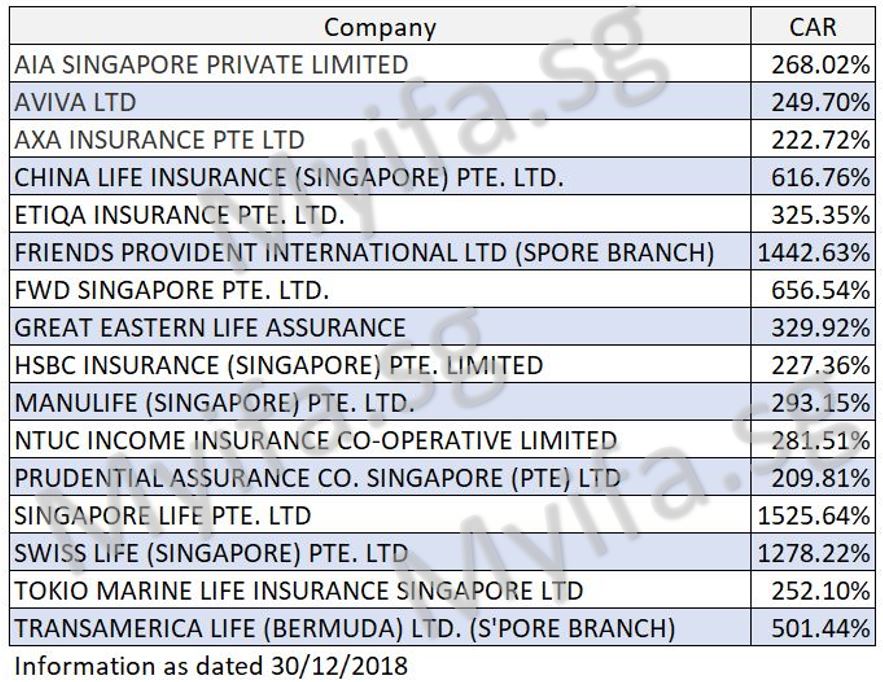

Having said these, let us see how each insurer fare in terms of the CAR which is a minimum of 120%. These comprises of only the life business of the insurance companies as general insurance have their separate CAR.

2 Comments