It is likely that you are reading this because you are concern or confused with the changes to the private integrated shield plans today(07/03/2018). In case you are here by accident and still unaware of the changes, you can read the following for more information.

Before discussing about the changes, let us first understand the need for it.

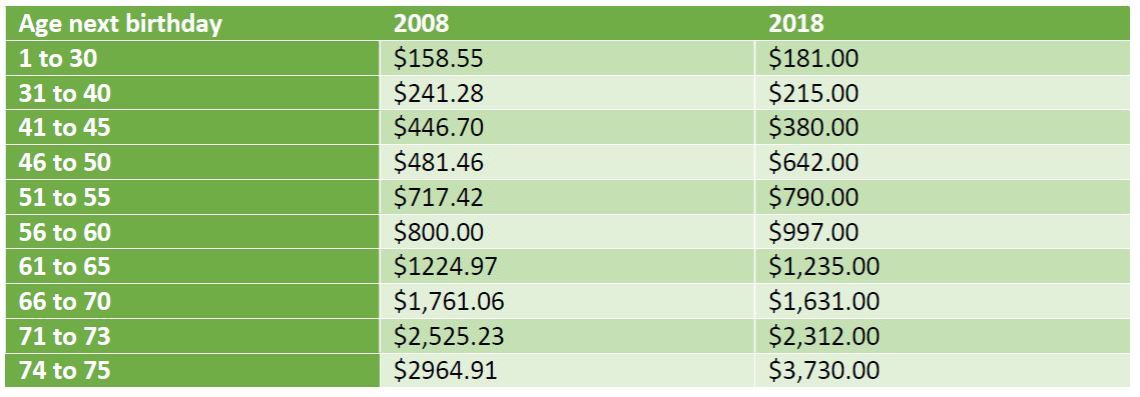

The following is a premium table for insured age 1 to 75 of an ISPs from one of the service providers in 2008 and in 2018. These premiums can be partially paid from the CPF Medisave Account up to the withdrawal limit base on the insured’s age.

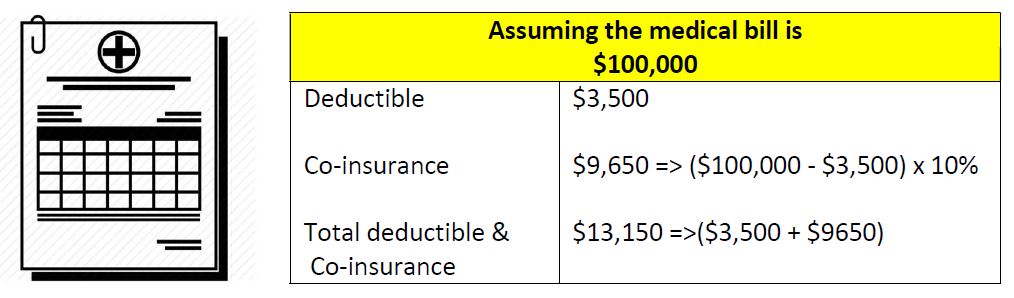

In order to cover both the deductible and co-insurance, the insured need to purchase the rider as below. It also shows the increase from 2008 to 2018.

The premiums for the main plan had increased 20 to 30% and the riders increased almost 200% to 300%. While different insurers may had adjusted their rates differently, the fact is all had sky rocketed over the last few years. Thus a change is needed and the question is “what” and “when” .

Before going to the details, let’s see if you are affected. The application date of your policy determines the impact of the new changes to your private integrated shield plans. The chart below shows the impact of the application dates on your ISPs.

Do note there is no changes to your policy if it was applied before 7th March 2018. However, we cannot rule out the possibility the insurers of making any changes to the plans.

What are the changes?

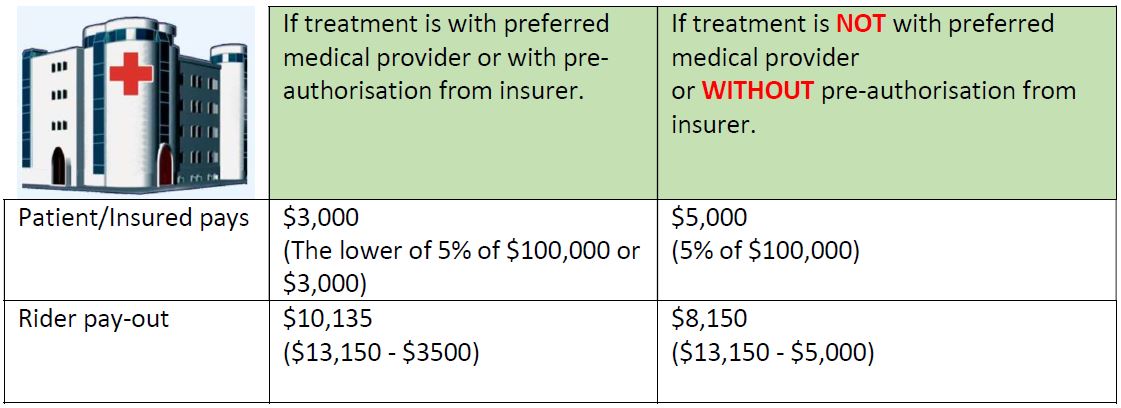

The patient must bear the lower of 5% or an annual cap of S$3,000 co-payment for new Integrated Shield Plan riders.

To manage cost, insurance companies will also also have their approved panel of doctors. The annual cap of S$3,000 applies if the insured is treated by the doctors in the approved panel or had received prior approval from the insurer on the treatment. This works similarly to some of your employee benefits where the insurer requires your medical consultation to be with a particular GP.

Example of the new IP Claim

Example 1

If there is no rider purchased, the patient/insured will have to bear the full amount of $13,150 assuming the balance is claimable by his IP.

Example 2

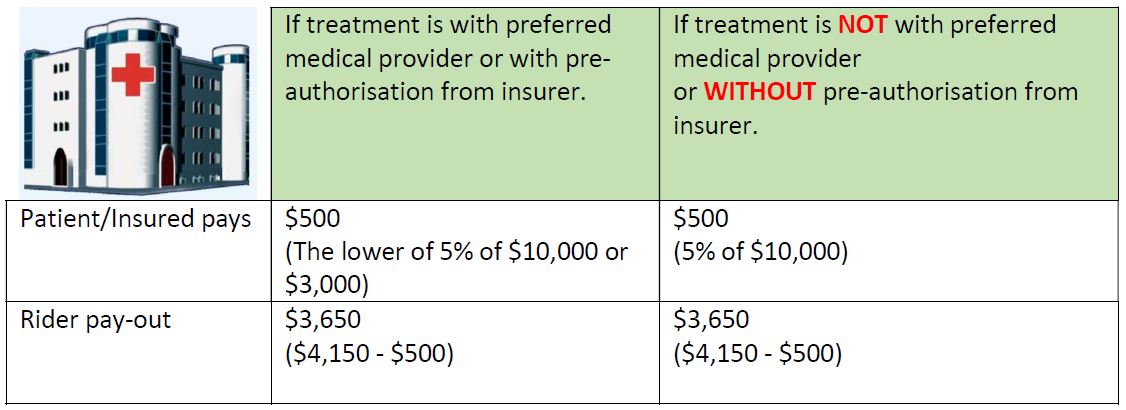

We can see from the two examples that the new IP has not much impact on small bills. The bill size needs to be at least $60,000 in order to have any difference between a preferred and non-preferred or pre-authorised and not pre-authorised treatment.

Conclusion

There are a few options that we can do to reduce or remove the 5% gap. There is no right or best way to do it and it depends on individual’s objective as well as budget. If you had purchased your IP before 7th March 2018, good for you. If you had not, please do so ASAP instead of KIV for any changes from insurer.

My colleagues and myself are conducting sessions for groups who need any clarification on the changes or to know how it affects you. All you need is to have a minimum group of 5 and we will arrange for a session for your group or staff.

I dugg some of you post as I cerebrated they were invaluable very beneficial

LikeLike