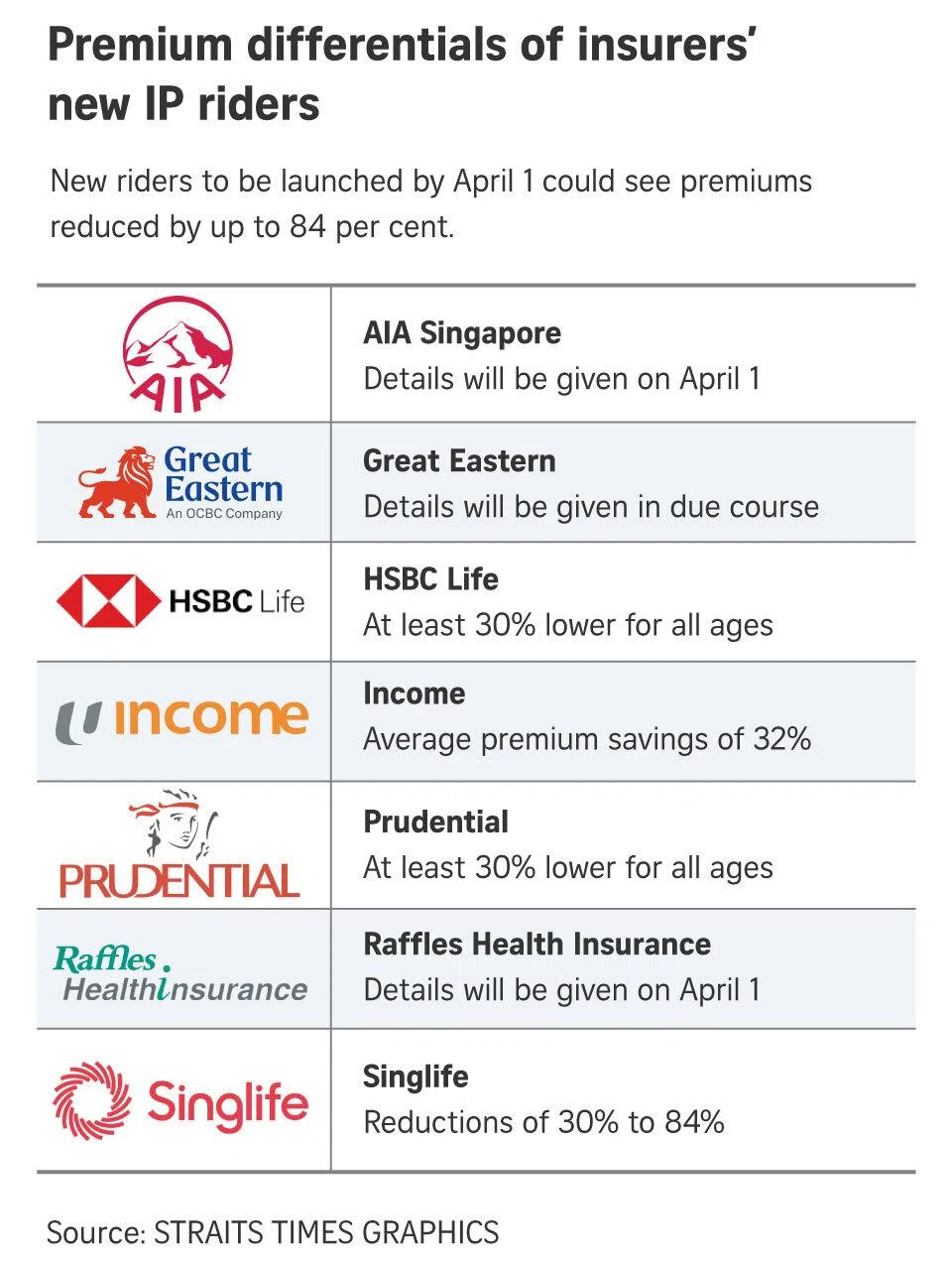

Over the past few weeks, the table as shown above comparing premium changes across insurers has been widely shared on WhatsApp and social media. I have received more queries about this than almost anything else in recent memory and rightly so. If you are one of the approximately 71% of Singaporeans who holds an Integrated Shield Plan, and especially if you have a rider attached to it, the changes coming on 1 April 2026 will affect how much you pay out of pocket the next time you are hospitalised.

Some policyholders have expressed frustration that the timeline feels rushed. That concern is understandable, but it is worth noting that the Ministry of Health (MOH) announced these changes in November 2025 giving policyholders several months to review their options. The purpose of this article is to make sure you use the remaining time wisely.

The image showing the premium change across insurers has been circulating around for the past few weeks and I had received quite a number of queries asking what should we do as an Integrated Shield Plan(ISP) policy holder. That don’t come as a surprise because about 71% of the population in Singapore has an ISP and and 67% of these IP policyholders have riders. This near-zero out-of-pocket model, while comfortable, has been quietly inflating premiums for everyone. the upcoming changes will affect them.

A Quick History: How Did We Get Here?

Integrated Shield Plans were originally designed to cover hospitalisation costs on an “as-charged” basis — meaning 100% of claimable bills were reimbursed by the insurer, provided the policyholder had purchased a rider to cover the deductible and co-insurance. This near-zero cash-outlay model was comfortable for policyholders, but it created an environment where over-consumption of medical services became normalised and, in some cases, treatment costs were inflated.

The first significant correction came in 2018, when MOH introduced a mandatory 5% co-payment. Insurers typically capped this at S$3,000 per year if treatment was received from their panel of specialists or if pre-authorisation was obtained prior to admission. That change helped, but premiums continued to climb at an average of 17% per year over the past three years, becoming especially burdensome for policyholders aged 60 and above.

The 1 April 2026 reforms are the next and more decisive step in that correction.

What Changes on 1 April 2026?

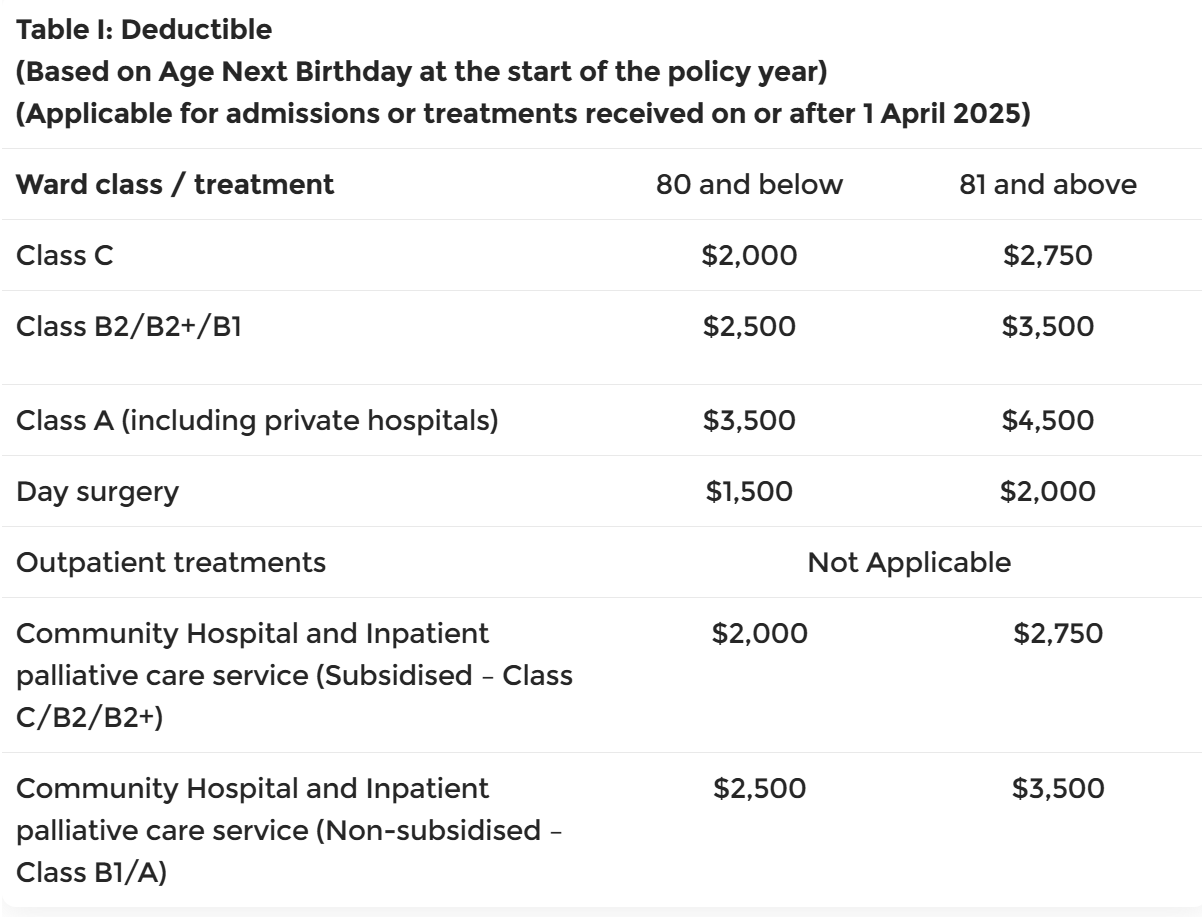

From 1 April 2026, new IP riders sold will no longer be permitted to cover the minimum IP deductibles set by MOH. The co-payment cap at , which was set at a minimum of S$3,000 per year in 2018, will also be raised to a minimum of S$6,000 per year.

In plain terms, two things shift:

1. You must now pay your deductible yourself.

Currently, your rider absorbs the deductible which is the first portion of the bill that must be paid before insurance kicks in. From 1 April 2026, new riders are prohibited from covering this amount. Depending on your ward class, the deductible ranges from S$1,500 to S$3,500. You will now be required to pay this yourself, either in cash or via CPF Medisave.

(Source: CPF Board)

2. The annual co-payment cap doubles.

The minimum cap on annual co-payments (your share of the 5% co-insurance) rises from S$3,000 to S$6,000. Importantly, this cap applies to co-insurance only and excludes the deductible, which means the two amounts now stack independently.

The 5% co-insurance rate itself remains unchanged.

The good news is the new riders are expected to cost approximately 30% less than current full-coverage riders. For private hospital policyholders, this translates to annual premium savings of around S$600 to S$1,600, with larger savings for older policyholders. However, the question is whether those savings outweigh the higher potential out-of-pocket exposure at claim time..

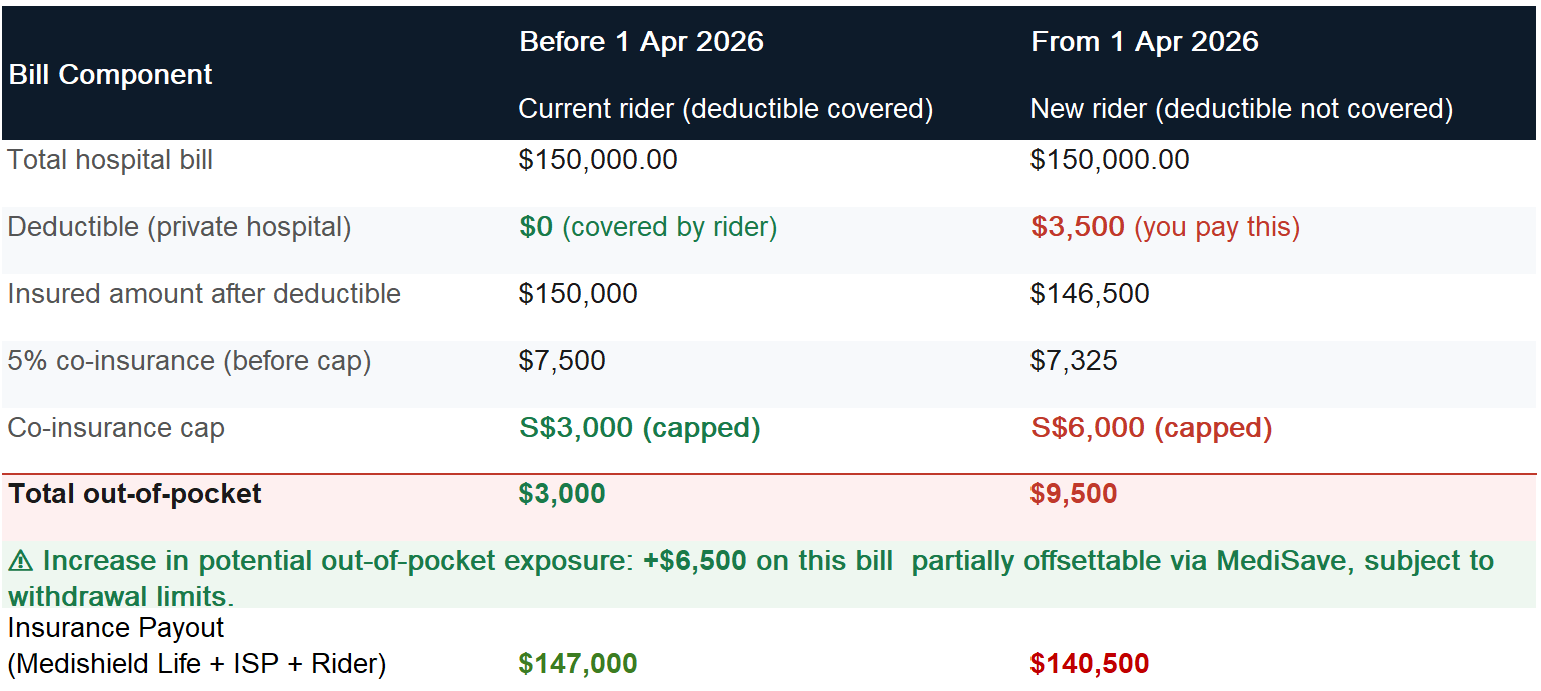

An example assuming a total hospital bill of $150,000 at a private hospital.of the impact of cash outlay is shown below

Base on current riders, the policy holder may have to pay $3,000 out of pocket and with the new riders, $9,500 after 1st April 2026.

Which Group Do You Fall Into?

There are 2 groups of ISP policy holders at this moment.

The first group are those who had applied their ISP on or after or incepted their ISP before 27th Nov 2025. Your rider will be automatically switch over to the new riders when the ISP is renew from 1st April 2028.

The second group are those whose ISP were applied or incepted before 27th Nov 2025 and they will be proetected under the Grandfather Clause which means the current change will not affect them. However, should they wish to downgrade their plans, they need to do it before 1 April 2026 in order to remain covered under current existing clauses and will not be affected by the changes for now.

Here are the key decisions to consider:

Option 1: Downgrade from Private Hospital to Government Restructured Hospital Plan

If you are currently on a private hospital IP and find the new premium and out-of-pocket structure unsustainable, downgrading to a Class A or B1 ward plan at a restructured hospital is a meaningful option. This means:

- Your deductible drops from S$3,500 to S$2,500 (Class A/B1)

- Your premiums fall considerably both for the base plan and the rider

- You still have access to specialists at restructured hospitals like SGH, NUH, CGH, NTFH and TTSH

- You retain the right to choose your specialist and ward within that tier

Note: We are neither recommending ISP from Income nor giving financial advice. Please speak to a financial adviser representative to understand the solution that most suit you.

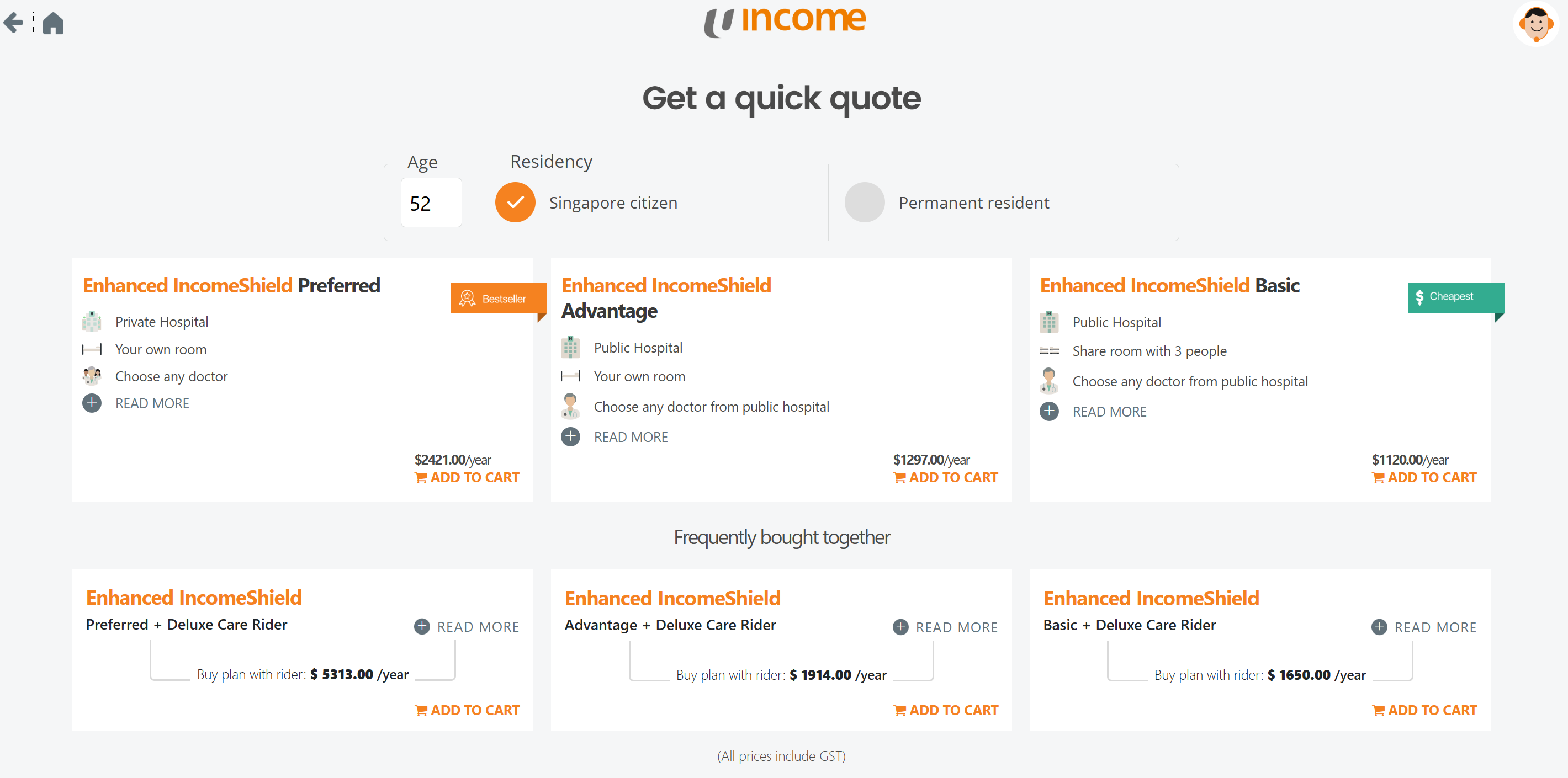

Using ISP from Income, the premium for the different plans based on a 52 year old Singaporean are shown above. There is no premium difference between genders or smoker status.

Preferred plan allows treatment at Private hospital and the main plan cost $2,421/yr. On top of that, if we get the Deluxe rider so that we only need to pay 5% co-payment upon hospitalisation, the total premium comes up to $5313/yr. Out of this amount, $600 can be paid using our CPF Medisave for the Preferred plan and the remaining $4,713/yr has to be paid by Cash.

We can choose to downgrade to the Advantage plan that allows up to Government Restructured “A”-Ward (Single Bedded Ward) or downgrade further to the Basic Plan that allows up to Government Restructured “B1”-Ward (4 to 5 Bedded Ward). By doing so, we will reduced our premium for $5,313 to below $2,000.

While we saved a lot in premiums, do note we are likely to seek treatments at Government Restructured Hospital. If we decide to have treatment in a private hospital. There will be pro-ration factor that range from 50-70% depending on insurers. This means if our policy has a pro-ration of 70%, we can only claim 70% of our medical bills.

Option 2: Downgrade Your Rider — Remove Full Deductible Coverage

If you wish to stay on a private hospital plan but want to reduce your premiums now, you can remove or downgrade your rider before 1 April 2026. This means:

- You voluntarily accept paying the deductible yourself going forward

- Your rider premium reduces significantly

- You can use MediSave to offset deductibles and co-payments, subject to withdrawal limits

By removing the deductible coverage means any bill below the deductible is not claimable. In the case of of a private treatment, the deductible is $3,500. If the bill is only $3,000 then the insurer will not pay anything. However, this amount will be accumulated and the insurer pays once the accumulated bill exceeds $3,500. If the bill is only $5,000 then the insurer will pay the amount above $3,500. By removing the deductible, we can see premium savings as much as 40% (depending on insurer & plan). Using the Enhanced IncomeShield Preferred as an example, we can do so by downgrade the Deluxe to Classic Rider. This will reduced the total premium from $5,313 to $3,885/yr.

While we save on the premium, the cash outlay is higher at point of claims.

The Deadline Is Real

If you are considering any changes to downgrade your hospital tier or adjusting your rider, you need to do by 31st March 2026. Any changes made after this date means your new or amended rider will fall under the new MOH framework with the higher deductible exposure and co-payment cap of $6,000.

This change is not the end of good health insurance in Singapore. The riders will still provide meaningful protection against large, unexpected bills and lower premiums may make coverage accessible to those who previously could not afford it. But the equation has shifted. The right plan for you now depends on more variables: your age, your health history, your Medisave balance, and your household’s ability to absorb a deductible at short notice. There may also be solutions available if we are looking to mitigate the cash outlay.

Every client is encouraged to review their IP and rider before the end of March 2026. If you are unsure what action is right for your situation, reach out and we can walk through your specific plan, your health profile, and your financial priorities together.

Disclaimer: This article is for general information purposes only and does not constitute financial advice. Please consult a licensed financial adviser to review your individual circumstances before making changes to your insurance coverage.