Peter is taking part in his first Marathon which has a distance of 42.195km. If he runs an average of 5km/hr, how long does he take to finish the Marathon?

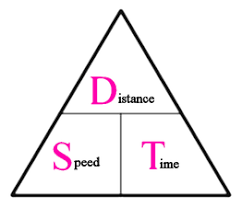

Don’t worry! We are not having a Maths class today. Most of us are familiar with the triangle below that shows the relationship between Distance, Speed and Time.

The answer to the question above will be

Time = Distance/Speed

= 42.195/5

=8.439 km/hr

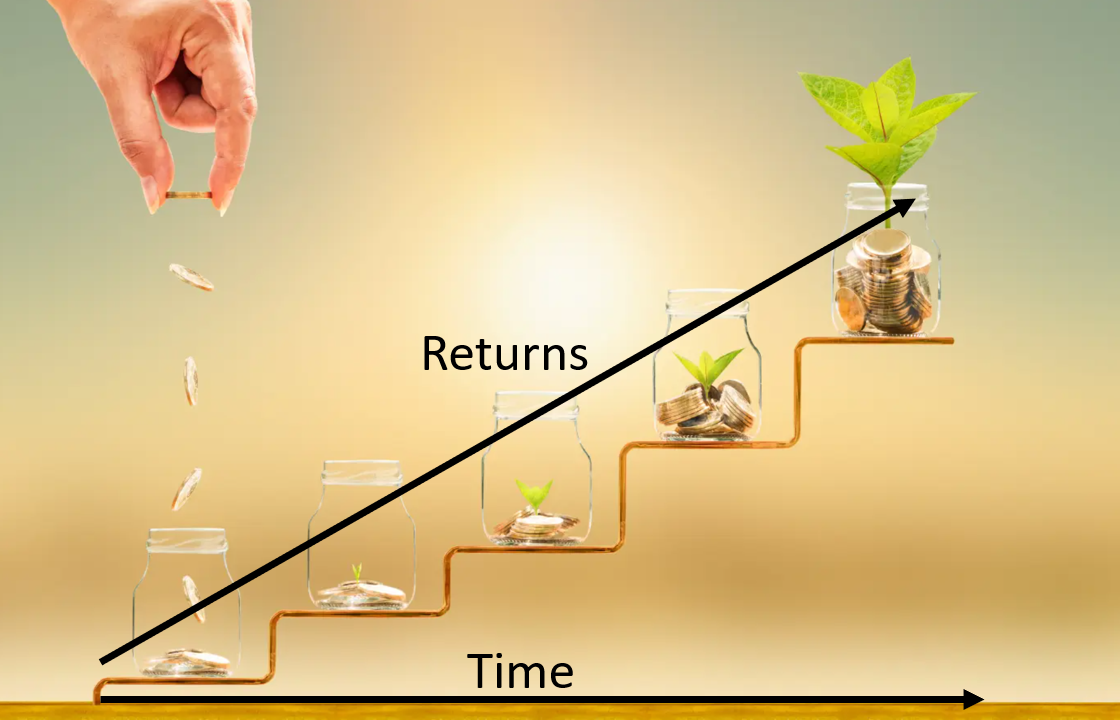

Now, assuming Peter needs to finish the Marathon in a shorter time, quite obviously he needs to run faster! What that means is he increases the probability of injuries such as falls and cramps if he increases his speed. The ability to run at the faster speed is also in question. So, how does what we had read is related to financial planning?

Think about it. Our financial goals are like the distance we need to clock. May it be accumulating a sum of money for our children education, retirement or a major purchase.

While we can usually change the variable of distance, speed and time, the reality in life is we have not much allowance to change. For example, if we need to plan for our child’s education fund in 18 years time and if we can move at our comfortable “speed”, we may be able to take 20 years to achieve it. However, we are very unlikely to delay this “time” to 20 years because that would mean our children are starting their university 2 years later than it should be. In order to achieve that “distance” in the given “time”, we will have to run at a faster “speed”. This means we may have to get a higher returns to get to our financial goals. Always remember that higher returns usually means higher risk as well. We are always prepared for a higher returns but are we prepared for a higher risk?

Let’s use the weekend to think of the “distance” we need to clock-

- What is my financial goal?

- How much is needed?

What is the “time” required –

- When do I need to achieve my financial goal?

- How much time do I have?

The “speed” that we can go.

- What is the minimum rate of returns I need to get?

- How much risk can I accept?

In most cases, we can adjust the financial goals and rate of returns but we cannot control the time. If we delayed a plan by 5 years, we are unable to cover this time loss but to increase to rate of return or reduce the financial goals. We have the experience, or heard of a colleague, of waking up late and have to rush to the office. We could had wake up early and take our own sweet time to make our way to office. Similarly, we can start to plan later and stress over achieving it especially when the market is bad or we can start to plan early, allowing ourselves to relax and cushion over the bad times. The choice is ours!