Most Singaporeans/PRs will have a private medical integrated shield plan in additional to your employee benefit that is provided by your employer.

In the event of hospitalisation, which insurance plan should we claim from:

A) Your private medical integrated shield plan (PMIS)

B) Your employee benefit (EB)

C) Both

If you had answer to any of the options above, you are right. However, what are the pros and cons of each option? Let’s start with Option C. While there is nothing wrong to claim both your PMIS and EB at the same time, it is not the best option. Both these policies works are contracts of indemnity and works in the principle of contribution. What ‘contribution’ means is the total claims will be shared among the insurers when multiple insurance policies are covering the same loss. For e.g. if a bill of $100,000 is file to the insurer for your PMIS and EB, both will share this bill. It may not necessarily be a sharing of 50% each but they will not pay more than $100,000. Thus, you may be doing double work.

Most people will go with Option B i.e. to claim the EB. This is the proper answer to the question. However, it can be administratively hassle to apply for the Letter of guarantee(LOG) for your treatment as you may have to go through your HR Personnel and submit the LOG to your medical institution. You may also need to pay your bills upfront and submit your bills to the HR Personnel or EB Insurer after your discharge.

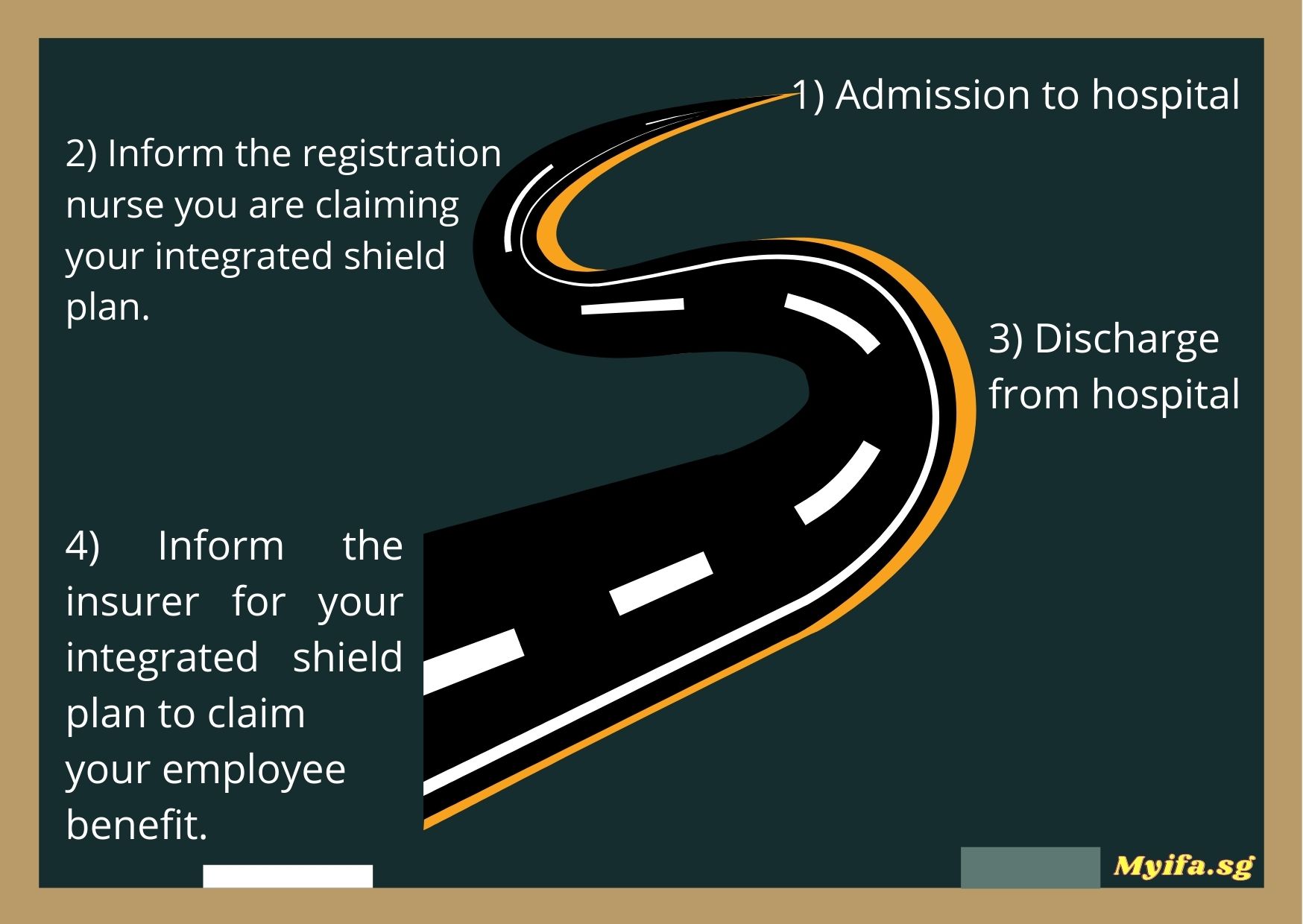

If you have a PMIS, my suggestion is to utilise it first. Two reasons for using your PMIS,

- PMIS is able to issue LOG during admission. The amount guaranteed by insurers range from $10,000 to $20,000. In the event if you are aware your bill cost more than the amount from the LOG, you can request your insurer to raise the LOG amount. Do note it is approval on a case-to-case basis.

- PMIS are integrated with CPF. This means you are able to discharge without paying a single cent in most medical institutions. The medical institution will settle your bills directly with your PMIS insurer.

However, don’t just stop there! Please inform your PMIS insurer to subrogate once you have finalised your claims your PMIS insurer. In more layman terms, it means getting the PMIS insurer to ‘counter-claim’ the EB insurer. Most of your PMIS insurers will send you a authorisation letter allowing them to subrogate from your EB insurer. All you need to do is sign and return to the PMIS insurer and they will do the rest. In case your PMIS insurer did not send the authorisation letter to you, all you need is to speak to your representative or the customer service officer to get one.

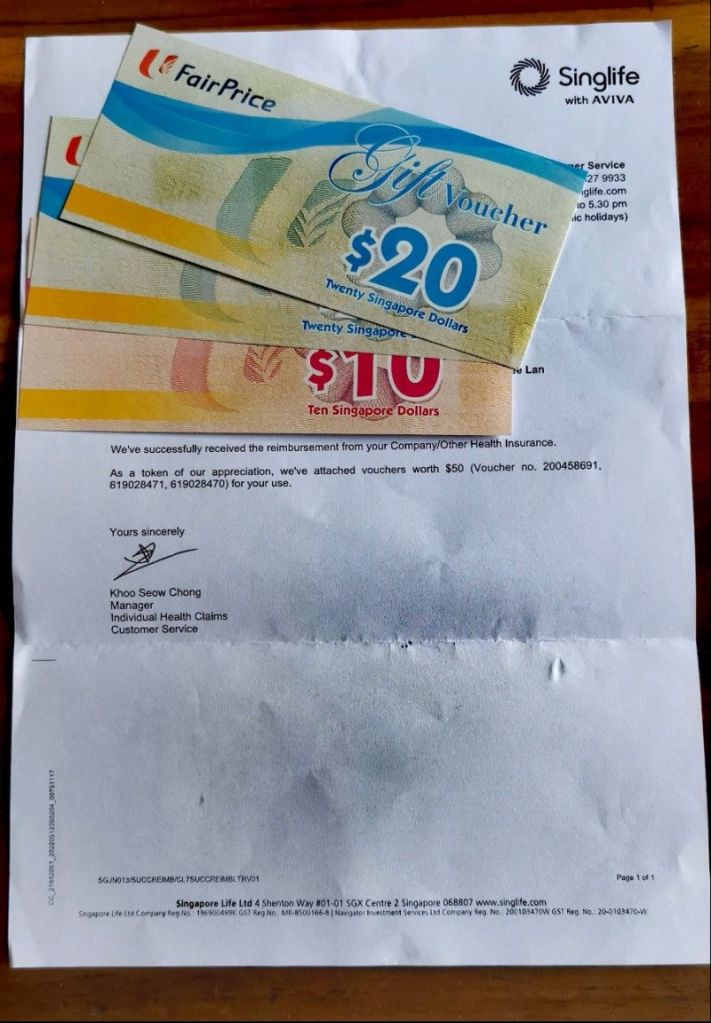

Most PMIS insurers also incentivise you when you subrogate your EB insurer.

This is an incentive for my wife. Singlife which is her PMIS insurer gave her $50 NTUC Voucher after they had successfully subrogated her EB.

If she had went direct to claim from her EB, she will not be entitled to these vouchers.

In summary, this is the process you may want to follow for future claims.