I received the above text via whatsapp recently. It is very common for Financial Adviser Representatives(FARs) to get queries on Supplementary Retirement Scheme(SRS) during the last quarter of the year. Before I share my answer to the above, let us first understand what is SRS and how it benefit us. In short, SRS is a tax-incentivised, voluntary form of savings strictly meant for retirement. For every dollar that you contribute to your SRS account will get you a dollar of tax relief.

While that sounds good, it may not be suitable for everyone. It makes obvious sense to contribute to SRS if you are paying taxes. However, SRS contribution will not be a effective tax reduction tool if you had reached the income tax relief ceiling of $80,000. Most tax payers I had advised and reached this limit are females who claimed “Working Mother’s Child Relief” which can be up to 25% of the mother’s earned income. Assuming both husband and wife earn $100,000 annually and ignoring other reliefs, the wife would have additional $25,000 of Working Mother’s Child Relief!

Does that mean we should not have an SRS account if we are not paying any tax? No necessarily so. There are still good reasons to have an SRS account despite not paying any tax in Singapore and we share look at the reason.

In an ageing country like Singapore, we know retirement is a serious social issue. SRS complements CPF to help us build our retirement fund. We also know the fact the retirement age will be increased over the years.

This is not just because we are an ageing country but most of our mortality rate is getting better over the years. If we are going to live longer, we cannot afford to spend a longer period in retirement unless our retirement funds are sufficient to last that extra few years. The retirement age in 1999 was 60 and life expectancy was 77. Without factoring inflation and assuming we need $10,000 a year in retirement, we need a total of $170,000 to see us through retirement from 60 to 70. The life expectancy in 2022 is about 83 years old. If we were to still retire at 60 and given the same assumption as above, we need to have a sum of $230,000 to see us through retirement from 60 to 83!

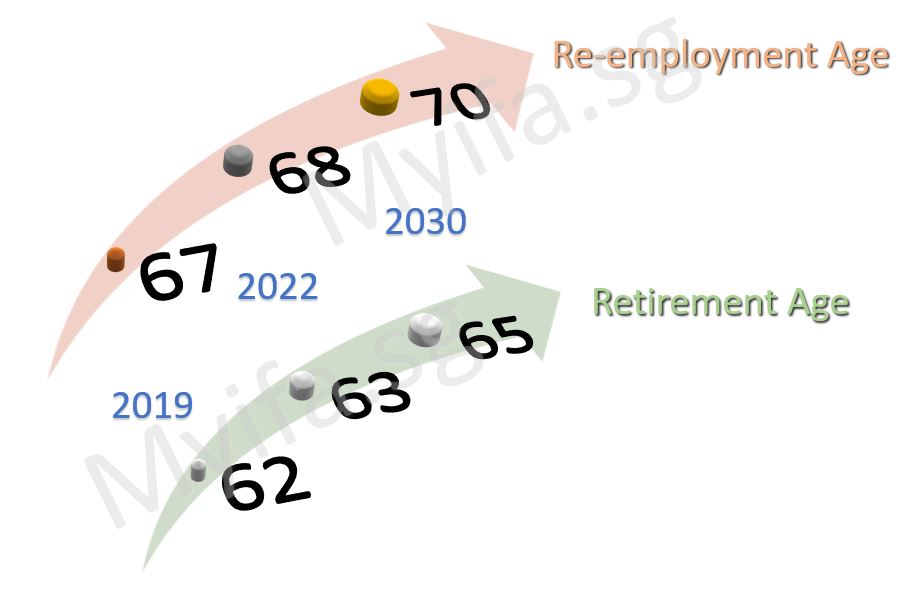

I have served many clients who are paying a 5 figures taxes annually and I remember the first income they received were not more than $3,000 a month. I would say some of their annual income when I met them a decade or more ago is as much as their taxes they are paying now. My point is, while we are not paying any tax now, it does not mean we will not pay taxes in future. All it takes is $1 to open an SRS Account today and you get to lock up your retirement age at 62 even though it will be pushed back to 63 in 1st July 2022. What this means is once you open an SRS Account now, it does not matter if the retirement age is pushed back to 63 or 65 because your SRS withdrawal age, which is based on the statutory retirement age, is based on the prevailing retirement age when you open your SRS Account. If you are not paying any tax, all you need is to open an SRS Account with a dollar and leave it alone till you start to pay income tax then assess the situation again. Most banks will charge a fall-below fee for the savings account but not your SRS Account. However, these are subjected to banks terms and conditions.

The banks that are SRS operators are DBS, OCBC, POSB, UOB. There is no preferred SRS operator and I will suggest to have your SRS Account with the bank that you normally use for transaction. It will be convenient for you. You can login to the via the bank’s mobile app or internet banking to have an SRS Account in less than 10 minutes. Once done, you can either perform a bank transfer, PayLah, PayNow and other options to transfer the money into your SRS Account. It is quite seamless!

WhatsApp us if you need any assistance or information for SRS.