I had completed my WSQ Diploma in Service Leadership with Service Quality Center recently. It was a great pleasure to be in a class with cabin crews who had years of experience serving one of the best airlines in the world – SIA. From their sharing, I am happy to know how the Airline tries to help the staff who are grounded during this pandemic and I’m confident that SIA will be back soaring high in the skies once again when the pandemic is gone.

A common question from the cabin crews and trainers was the reason to self-sponsored for this program especially I had zero skillfuture credit left and have to pay by cash. My answer to them is while banks, insurance companies etc had spent a huge sum of money to provide top notch services in the financial service industry, the service provide by individual financial adviser representative is still very lacking. It may sound very idealistic but I hope there will be a framework or at least a CRM system where it is more service than sales-oriented in future. And I hope this course will give me more insights to service excellence.

I am glad that I managed to pick a few good processes and ideas that can be modified to suit an (almost) One Man Operation model for an financial adviser representative. One of the take away during this course was being introduced to Customer Satisfaction Index of Singapore (CSISG). The CSISG is a measure of customer satisfaction cutting across a variety of key sectors and sub-sectors in the services industry of Singapore. The study is conducted by SMU and produce on a quarterly basis. However, it is updated annually. In the CSISG model, each company’s satisfaction score is an accumulation of their customer’s expectations and opinions. Different sectors will have different touchpoint allowing us to perform comparisons between companies. Today, I shall share the finding of the financial service industry in specific for the insurance sector.

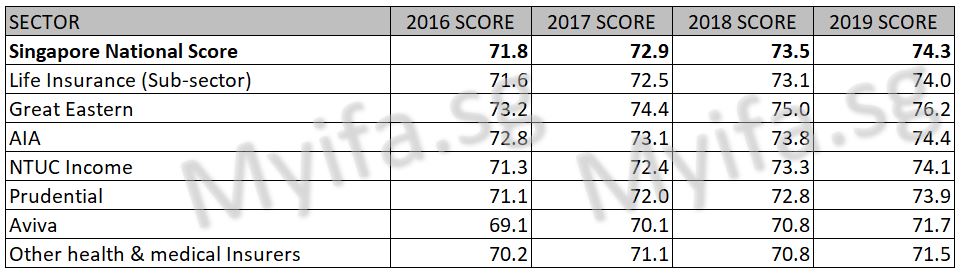

The Singapore National Score serves as an benchmark for services across different industries and the following table shows the average score a particular industry performs i.e the Health and Medical Insurance. For example, in 2019, the industry average was below National Score. Prudential was the only insurance that not only did better than the industry average, its service score was better than National Score.

The Life insurance industry excluding health and medical insurance paints a different picture as below.

First, I am glad to say the scores for the insurance industry been improving year to year from 2015 to 2019. This article is not to show which company is better than another but it serves as a good guide that every company has lots of room for improvement in terms of service standard. One of the worries faced many financial adviser representatives is the competition when it comes to different channels of distribution as well as contact points with the clients. I believe most will not be surprise to know majority of the touch points with clients are from Financial adviser representatives.

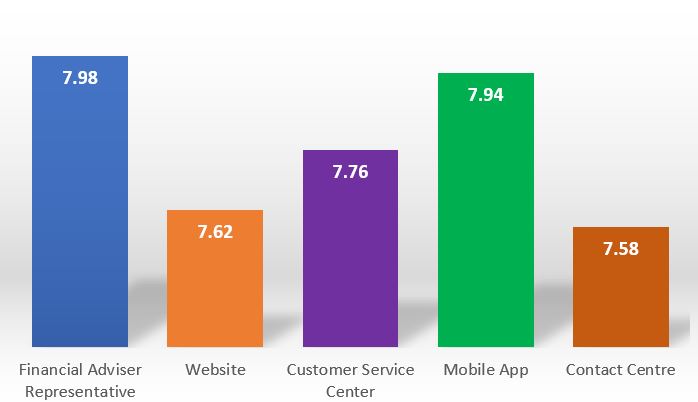

Next, we look at the satisfaction level when clients contact the various channels. The lowest scale of satisfaction is 5 and a score of 9 being the highest.

In my humble opinion, these result shows that despite huge amount of funds are invested into technology, a interaction with a human sitting face to face in front of the client to handle queries is the method preferred by clients. While customer service center and contact center also offers that option, the fact that the staff may not understand the client’s situation as well as the financial adviser representative may had resulted in a much lower rating.

We shall look into the sales process in future.