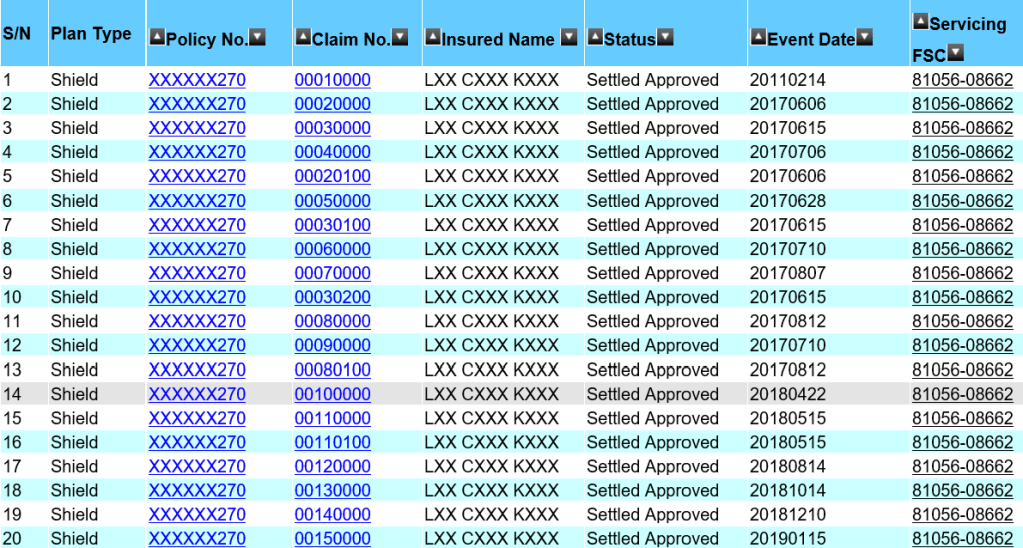

The list above shows an actual claim from one of my client, aged 45, for his hospitalisation bills. The treatment started in 2017 and is currently on going. I am thankful that we have an efficient healthcare system in Singapore that made these claims a seamless process. However, there are also bills such as Pre- and Post-hospitalisation bills that may need the financial adviser representative (Rep.) to make numerous trips to the client’s residence to collect the bills. The Rep. will assist with the submission especially if the client had just discharged from the hospital and not in the condition to submit the claims on their own. In some cases, the Rep may have to advice the policy holder how to claim or help to appeal on rejected claims. Before I continue, let me clarify that I am not writing to show you that I am a good Rep. with fantastic client service. What I had mentioned are activities that majority of my fellow financial practitioners will do for their client as well and we do not expect anything except maybe a thank you. Thus, I saw the need to speak up on an article that suggested the premiums for integrated shield plans were caused by the amount of money paid to Reps and management.

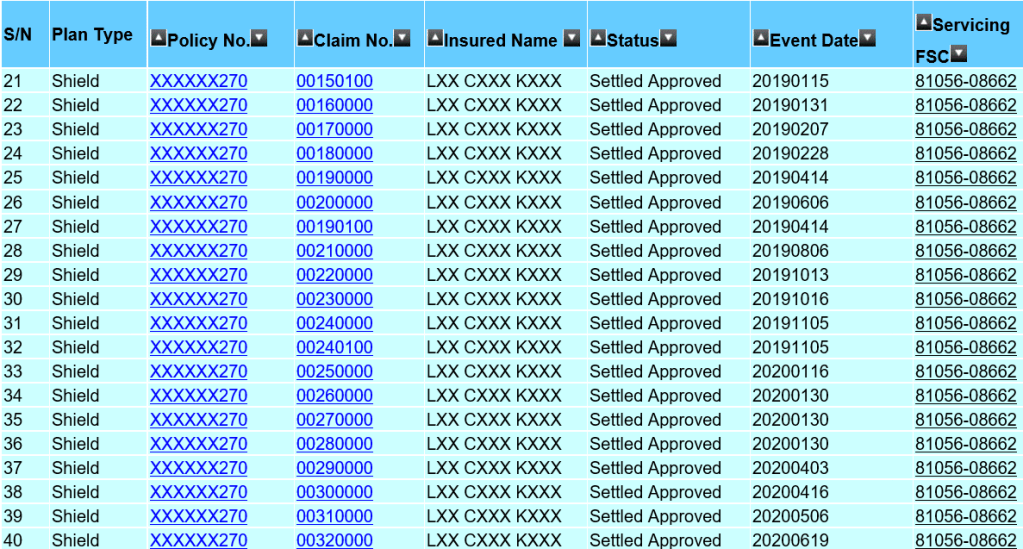

As mentioned, the first claim by this client dated in 2017 was about $50,000. Ignoring other claims, the insurer has to charge the client an average premium of $16,666 over 3 years till 2020 to cover that bill. The actual premium paid was about $2,500 annually during this period and that’s a total of $7,500. Again I mentioned, ignoring other claims, base on the $50,000 claims alone, the insurer had ‘lost’ $42,500 on this client. A more accurate claim amount made so far will be exceeding $120,000 with $60,000 made in 2020. You can estimate the loss made by the insurer.

When a claim is filed, the claim officers are required to process the claim as well as the finance department to make the payment to CPF and the medical institution even though the shield plans are integrated with Medishield Life now. Those are man-hour cost to an insurer and it is quite ridiculous to assume insurers should absorb this cost. It was mentioned about 13% goes to these management cost and the actual amount is $325 a year or less than $30 a month if you take reference to an annual premium of $2,500 . Do you think that is a fair amount to pay for the claim officers to process the claim? Of course, the argument is if the premium is higher for e.g. $10,000 then 13% is significant at $1,300. That is true and that will likely be the premium for someone age 80 and above. Logically speaking, the chance of hospitalisation is higher thus the premium is higher and that is also likely to be more claims to be processed(more work to be done). In today’s environment, we are fighting for minimum wages to be at $1,300 per month and here we are, suggesting $1,300 a year is too much for the claim officers’s man-hour rate.

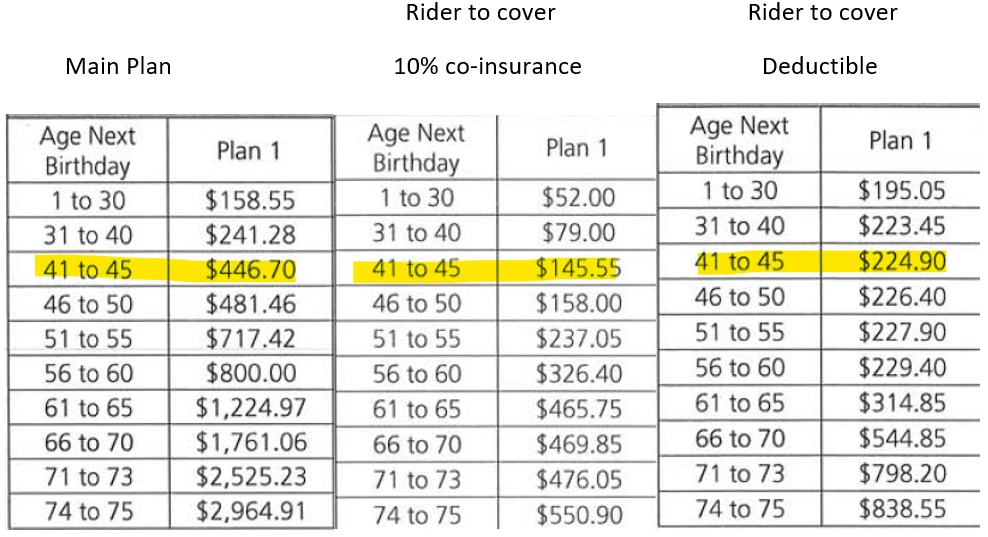

The beauty of insurance is risk pooling. That means we share the risk and in this case, the claim of $50,000 will be shared by the same age group of policy holders. And we need to collect from 20 policy holders of the same age to cover this $50,000 assuming the premium is $2,500. However, do note the more policy holders, the more claims will arise. Let us look at how the premium had escalated over the years. Below shows the premium for an integrate shield plan that covers private hospitalization in 2010 for an age 45 male.

The premiums for the main plan has increased from $446 in 2010 to $714 in 2020 and the total premiums for the riders had increase from $369 to $1282 for an 45 years old male. What was reported correctly was the premium for the riders had increased significantly but to have a rider is an option. It was suggested a reduced commission for Reps will reduce the premium. Before we go into that, let us look at the differences between Medishield Life and the Integrated shield plans mentioned above. In summary, Medishield Life covers B2/C ward in government restructured hospitals while the above integrated plan covers up to private hospital. Such comparison is similar to comparison a Japanese car to a Continental car and asked why the latter is so much more expensive. A fairer comparison is to look at a Japanese car compared to another Japanese car and in this case, an integrated plan that covers up to B2/C ward in a government hospital as well.

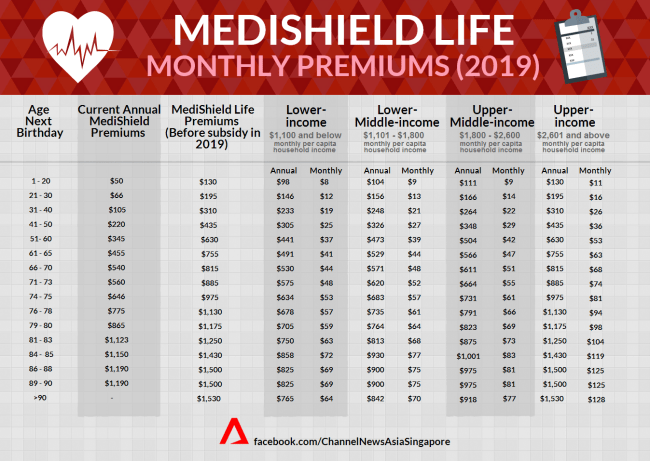

For a policy holder aged 45, the Basic and Rider premiums for an integrated plan that covers up to B2/C ward in a government hospital in 2010 was $314.05 and $267.50 respectively. Today, the premium will be $312 and $350. While the premium for the riders had increased, it will not significant and the Basic premium had in fact reduced. My point here is, insurance companies, are not charity organisation and they exist to make profit just like any establishment. The question is how much profiteering are the insurance companies making by increasing the premiums and why didn’t insurance companies increased the premium for B2/C ward government hospital plan as much as they did for the plan that covers Private hospital? How much does 13%, 20% or even a 30% of commission significantly increased the premium as compared to the bills incurred. Are we chopping the wrong tree to find the worm?

A reference we can use to determine what is an acceptable increase is looking at how much the national scheme had increased over the years and the proposed increase.

While having a portable health insurance is a good idea and I would like to see that happen, we need to be careful with a few issues such as churning from Reps or cherry-picking from consumers leading to adverse selection. To put things into context, how might the situation be if majority of the policy holders with medical conditions switch into your insurance company? If we look at Table 1, the premium for our national healthcare scheme almost doubled for an 45 years old Singaporean. The reason for this increased was there were better benefits and more importantly, Medishield Life provides cover for pre-existing conditions as well as congenital and neonatal conditions. This increased in premium means every Singaporean is co-sharing the risk by having the healthy ones pay more to compensate for the higher claim rates of the less healthy ones with pre-existing conditions. This system works because this is a national scheme and there is a large number of people to share this risk to make it affordable, thus, the Medishield Life was also made mandatory. However, in a private arrangement like an integrated shield plan, most(if not all) policy holders will not be willing to pay the extra premium for another person’s risk. Therefore, insurance company charge a loading or additional premium if a policy holder has a higher risk of claim and in a situation where insurers feel that a particular risk will affect the risk of the rest of the policy holders, they either exclude that risk or reject the application. This is to protect the interest of the company as well as other policy holders.

1 Comment