A fellow financial practitioner recently asked me if I heard of HSBC Insurance will be taking over Aviva Ltd during a coffee session. My replied was that nothing is confirm at this stage. Furthermore, it seems that Allianz, Nippon Life and MS&AD are also interested in this deal. The questions in some consumer’s and practitioner’s mind are mainly who will be buying over Aviva Ltd and more importantly, what happen next? We are not going to discuss the issues relating to the buying of Aviva Ltd in this article. As a policy holder of Aviva Ltd, you can have multiple concerns. From bonus payout to getting policy information to customer service. Let us explore what happens when an insurer exits Singapore.

There are two ways an insurer will exit Singapore – One is by force i.e. either the authorities terminate their insurer license in Singapore or due to bankruptcy. We will discuss these scenario in another post. For now, we will discuss the other way of exit which is on a voluntary basis i.e. when the insurer decides to shut down their operations in Singapore or sell their business operation to a third party.

Is this a first in Singapore?

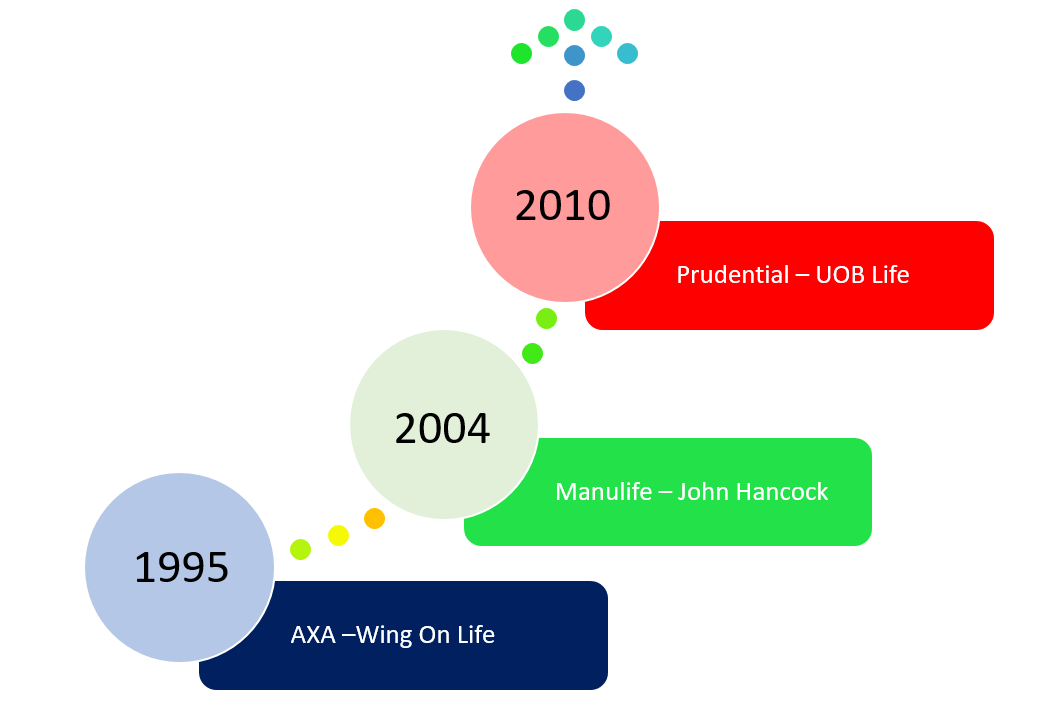

Are there any precedent case of an insurance company being acquired in Singapore? Base on my knowledge from the day I started my insurance business in 1998 with AXA Life, they acquired Wing On Life. I cannot remember the exact date but it was around 1995. That was the very first acquisition that I knew of for an insurance company. Almost a decade later, in 2004, the second acquisition took place between Manulife and John Hancock. Manulife bought John Hancock at an estimated US$11 billion and as this was a global deal, the office in Singapore were merged too. I was then carrying policies from both companies and this merger kind of made the life of an Independent Financial Adviser easier since we just have to market policies from Manulife instead of both companies. Six years later, UOB Life was sold to Prudential and re-named as PruLife in 2010. In all these situation, the new owners continue to honour their legal and contractual obligations to service their acquired clients in terms of returns and claims.

What if there is no ‘takers’?

Things can get more complicated when an insurer wants to cease their operation and exit Singapore but there is no buyer or they may not want to sell their portfolio to another party. In this case, the authorities(MAS) still require them to maintain an customer service office locally to handle claims and other queries. They are still contractually liable to their policy holders. One such exit was by Zurich Insurance in 2015. Mr Colin Morgan, (the then)chief executive officer of Zurich’s life business in Asia Pacific said, “We will be retaining a core number of people to oversee the transition, as well as an ongoing dedicated support team to service all existing customers, and wherever possible, Zurich will do what it can to redeploy affected employees within the organisation.” It was almost 3 years later that Zurich Insurance sold its portfolio to Singlife Insurance which got its insurer license in 2017. However, it is assuring to say that the policy holders of Zurich Insurance were still serviced well during these 3 years before Singlife Insurance appear.

Will the returns on my policy be affected?

When we pay our insurance premiums, the premiums are pool into a common fund known as the par fund(Participating fund). The par funds are invested into different assets such as stocks, property, bonds or other investments to generate the returns for our policies. MAS had mandated insurers company to give back 90% of the investment returns to the policy holders before distributing the maximum of 10% to the share holders. These par fund are separated from the share holders fund and what that means to you is regardless of how good or bad the performance of the insurance company, it will not affect your policy returns. In fact, any shortfall to meet the guaranteed benefits or solvency requirements of a par fund has to be funded by shareholders. However, if the par fund is not managed well or the market is not performing well, the returns on your par fund may be lower than projected.

The above is an example of how an insurance par fund is invested

In the event of an acquisition of another life insurance company, the team that managed your par fund usually remains the same. That means if you had trust this team to return the illustrated returns when you purchased your policy, you should trust that they are able to do it regardless of which insurer they work for. And if for some reason they are not doing their job and gave a lower than expected returns, the new owner may use their own team of fund managers who had performed better.

In conclusion, an merger & acquistion of an insurance company will not have significant impact on the interest of the policy holder. There are financial adviser representatives who advice against the exiting insurer and IMO, while that concern is appreciated, it is unwarrant to do so unless that insurance policy itself is a bad deal.