If you have been paying for your private medical insurance i. e. Shield plans, you might be receiving the renewal notice together with a rude shock. Depending on insurers and your age , the increased in premium can range from 20% to 35% on the main plan. The jump can be as high as 50% to 80% for the riders. An article on the increase in premium was shared much earlier here.

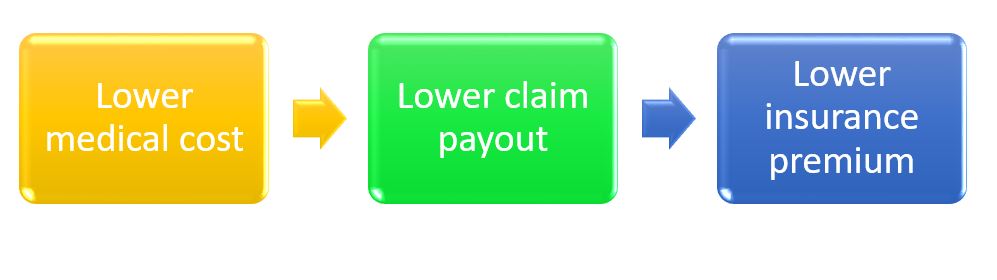

The obvious reason for the increase in premium is the huge losses incurred by the insurance companies resulted from much higher cost bills compared to the previous years. Mercer had recently reported that the medical inflation in Singapore was 10% in 2018. The most logical cost cutting measures is to manage the cost of treatment is as follow.

While we know there are numerous cases of over-charging and over-treatment by doctors, we have to accept the fact the medical cost is increasing due to new medical technology and treatment. Let us take a cancer treatment as an example. A diagnosis of cancer will be a death sentence in the past but today, the survival rate can be as good as 100% depending on the stage of cancer.

(Source: What are the most curable cancers? )

In 2005, I made my first critical illness claim for breast cancer. She went on to survive very well. Sadly, she pass on in 2015 but it was due to stomach cancer.

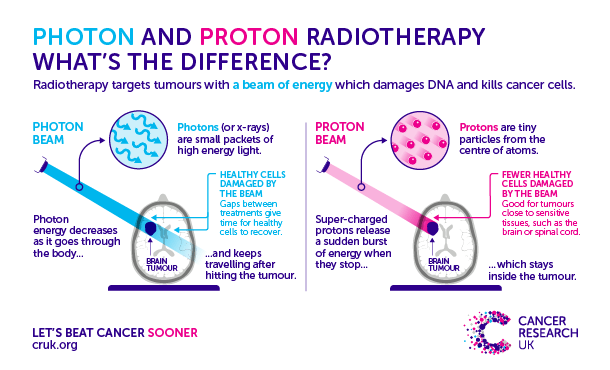

I had also made a critical illness claim in 2017. He was diagnosed at Stage 3 and the client is still surviving well today. As previously mentioned, one reasons for medical cost to escalate so much is medical advancement. The commonly method of treatment for cancer are Chemotherapy and (Photon) Radiotherapy. A new way of treating cancer is Proton Radiotherapy or Proton Therapy in short. It is similar to Radiotherapy i.e. both use beams of energy to inhabit the cancer cells. The differences are Photon Radiotherapy uses X-Ray while Proton Therapy uses Proton rays. The main advantage of Proton Therapy is it can focus on the cancer cells thus cause less damage to Radiotherapy which will also kill the healthy cells around the tumor. In military term, the traditional radiotherapy is “Area target” and Proton Therapy is “Point target”.

You might be asking since it is less damaging to the patient’s health, why are medical institution not replacing the traditional radiotherapy with Proton Therapy? There are many reasons and one main reason is cost – the cost of treatment using Proton Therapy is far more damaging to the pockets than the traditional radiotherapy method. The machine for proton therapy treatment was recently installed at The Singapore Institute of Advanced Medicine Holdings (SAM) and an estimation of the treatment cost was given by SAM’s chairman and chief executive officer, Dr Djeng Shih Kien.

Dr Djeng said, “Conventional radiation therapy currently costs about $25,000 to $30,000. Proton therapy at the centre will cost up to thrice as much and require about the same number of sessions”

Proton Therapy is not covered under our Medishield Life and most of the Private integrated shield plans at the moment. Aviva Myshield is the only Private Integrated Shield plans that covers that treatment at the moment.

There is no such treatment available in Singapore at the moment and it will be available only in early 2020. Without actual costing, we cannot get the insurer to include the risk without pricing it into the premium as well. Personally, I’m not sure if it will be a good idea to be included in those plans. If the cost of treatment is costing 300% more, how much increase will we see in the premium of the policies? And if we wish to get this less invasive treatment now, we have to visit USA, Europe or a few Asia countries such as China, South Korea, Japan, Taiwan. Medical insurance that covers oversea scheduled treatment can be an option for patients who intent to seek treatment outside of Singapore. You can check with your Financial Adviser Representative if your plan covers that.

Assuming the cost of treatment is $100,000. How much more will it cost to include the flight, lodging of your family members etc? That is one reason I disagree with an article which suggested we just need medical insurance and critical illness plan is not necessary. In a similar situation, the critical illness plan will pay the lump sum of your coverage that could be anything from $100,000 to $300,000 or more. You can decide to use this money to seek treatment oversea if needed or if the treatment is in Singapore but not covered by the medical plans, you can use it to pay off the bills. Of course, it may be a different case if one has that 2 or 3 times that amount idling around.