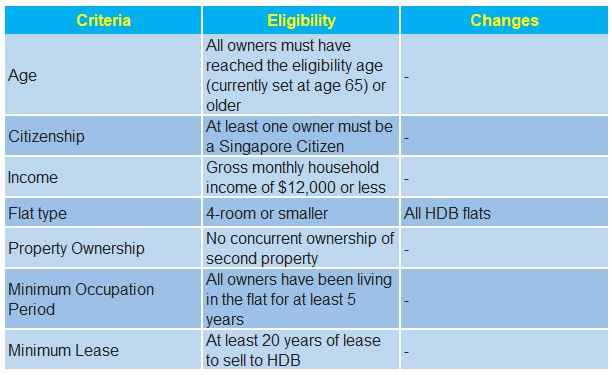

The Lease Buy-back Scheme(LBS) came in effective from 1st April 2015. Although many people feedback that the idea seems like a joke, it was not meant to be one. LBS is not a new idea invented by (Housing Development Board)HDB. It is a form of reverse mortgage which is a way of converting the money that is lock up in your property into liquid cash so that you can have more cash on hand for your retirement. OCBC Bank and NTUC Income offered it as early as 2006 but they were discontinued due to low demand. The following is the existing criteria of LBS and the changes that will take place.

This post is not going to discuss LBS in detail but to share the idea of a reverse mortgage scheme in general and who may be suitable for it. So, what exactly is reverse mortgage?

Before going into the details of how a reverse mortgage works, let us first look at a typical mortgage when we buy a property. Assume that a man bought a property and took a mortgage of 20 years. He will be required to pay a down payment and service an installment over the next 20 years. After which, this property becomes fully paid and he takes over the ownership of the house from the bank.

Before going into the details of how a reverse mortgage works, let us first look at a typical mortgage when we buy a property. Assume that a man bought a property and took a mortgage of 20 years. He will be required to pay a down payment and service an installment over the next 20 years. After which, this property becomes fully paid and he takes over the ownership of the house from the bank.

Some of the risk involved in a mortgage loan are the upward change in interest rates or worse, when there is a bad market and the property value drops to a point that the bank needs you to top up the difference because of the Loan-To-Value(LTV) Ratio. The LTV Ratio in Singapore is 75% for most first time home buyers. This means if the maximum loan amount a homeowner can get is $375,000 and your down payment needs to be at least $125,000 if the property is worth $500,000. If the price of the property drops, the bank will ask the homeowner to top up the difference if it falls below the LTV ratio.

In a reverse mortgage, as the name suggest, it works opposite of a mortgage loan. Now, we have a fully paid property and we pledge it to a financial institution e.g. a bank. Think of it the financial institution is buying back the property and taking a loan from you. They will give you

- A lump sum of money upfront

- A sum of money every month for the tenure.

One of the risk involved is when the value of the property drops, the sum of monthly income will drop as well. If you wish to remain the same level of income, you will have to top up the difference in value. The logic is similar to the LTV Ratio reason mentioned above. A legal suit was filed against NTUC Income in 2009 because of such situation.

In additional to the risks, some considerations to look at are the surviving spouse or children living in the house. In the event of your death, the surviving spouse of children can choose to pay off the money that you had received to “buy back” the property or continue to receive the money till the tenure end and let the financial institution take over the property. These are usually stated at the point of entering into the contract. Another possible scenario is if you outlived the tenure which the financial institution have the right to take back the property.

Do note that the above mentioned are reverse mortgage in general and the financial institutions are mainly commercial oriented. The terms may not be the same in the case of the LBS offered by HDB because end of the day, the HDB flat is meant as a public housing. You can read on the details of how LBS works.

In most cases, a home owner can consider a reverse mortgage if he has not dependents or there is no intention of leaving the property to the dependents. Even with that, it may be better to rent out the extra rooms to receive the monthly source of income and have someone staying together to know that they are well and healthy. Of course, rental will have it’s issues as well.

In a snapshot of how reverse mortgage works, you can refer to the diagram below.

In conclusion, weigh the pros and cons, discuss it with your financial adviser and know what is best for you.