The outlook for mortgage rates is that the rates are expected to go up. It is a known fact the mortgage rates have a significant impact on the cost of buying a home. When the rates increase, your monthly payments go up. A 5 basis point change in the rates can be significant in the long run especially the loan size is huge. Assuming a loan of $1,000,000 at 1.60% increased to 1.65% will see an installment repayment from $3,499 to $3,524 over 30 years. Thus, consumers are always concern about the rates. While mortgage rates is beyond our control, we can decide on another major factor that affects the repayment installment i.e. the amount of loan to commit. A common decision to be made by property buyers is should they pay more upfront and take a smaller loan or should they pay less upfront and hold more cash for liquidity. But there is no right or wrong answers to that decision. On top of the investment opportunity to generate a better returns than the mortgage rates, it also depends on a person’s mindset to be debt free.

Let me share one of my client’s situation and you decide what you will do. We shall call him Mr. Million.

Mr. Million had purchased a property and took a 30 years mortgage loan of $1,000,000 at 1.6% p.a. The monthly repayment as well as the total repayment amount is as follow.

The monthly installment is $3,499. The total interest paid will be $259,781.

Mr. Million have a spare cash of $150,000 and he was unable to decide to reduce the loan to $850,000 or just hold that cash and re-invest it.

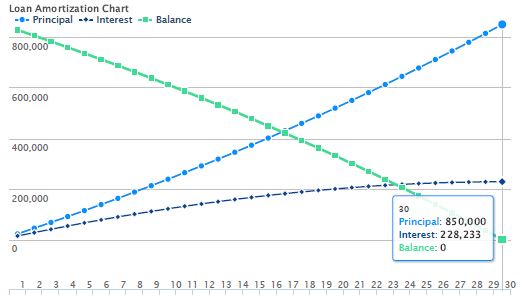

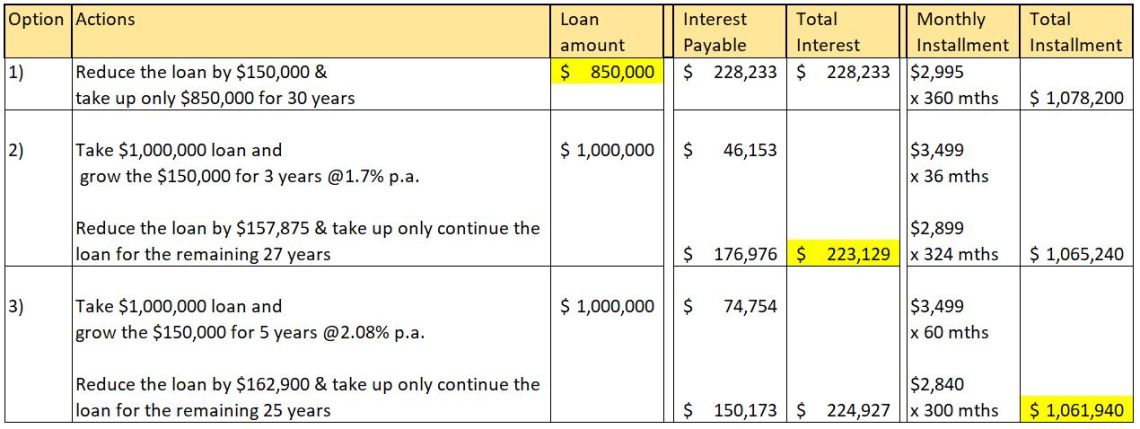

Option 1: If he choose to reduce it by $150,000.

Advantage:

- He reduces the monthly installment to $2,995

- The total repayment is reduce to $228,233

Con:

- He lose the liquidity of $150,000 for liquidity

- The $150,000 can serve as a backup fund for his monthly installment of $3,499 if needed.

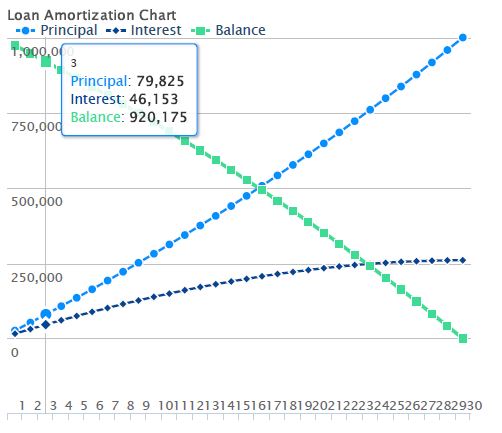

Option 2: If he choose to take a $1,000,000 loan and set aside the $150,000 with (i) guaranteed 1.7% p.a. over 3 years or (ii) a guaranteed 2.08% p.a. over 5 years.

(i) After repaying $3,499 monthly for 3 years, the remaining loan amount will be $920,175.

The $150,000 would have grown to $157, 875 after 3 years. He can do a capital reduction or re-financing when the lock-in period cease. With that, the new loan amount will be $762,300.

This will reduce the monthly installment to $2,899 and a total repayment interest of $176,976.

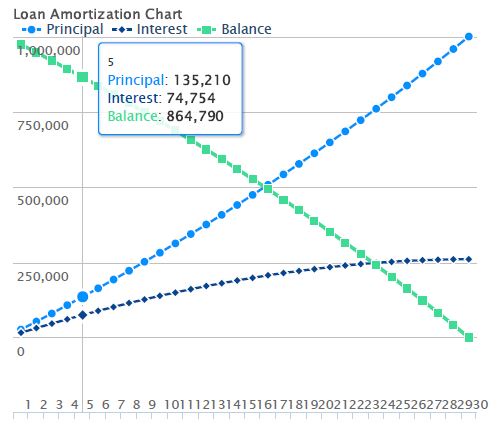

(ii) Alternatively, he can hold this $150,000 over 5 years at a rate of 2.08% p.a.

After repaying $3,499 monthly for 5 years, the remaining loan amount will be $864,790.

The $150,000 would have grown to $162,900 after 5 years. He can do a capital reduction or re-financing when the lock-in period cease. With that, the new loan amount will be $701,890.

This will reduce the monthly installment to $2,840 and a total repayment interest of $150,173.

So, what does all these means? Below is a summary:

In conclusion, while we were taught to take up a lowest possible loan to reduce our liabilities, it is always good to look at the opportunity cost. There is no best option. It depends on a person’s preference to have the lowest liability, pay the least interest or pay the least cash outlay.

Do note the above scenario is assuming the interest rate remains at 1.6% through out the repayment period. The results may change accordingly to the various factors and you might want to do a proper assessment first before deciding the best course of action.