Endowment policies are commonly known as “Saving plans”. The main objective of getting an endowment policy is to accumulate a sum of money at the end of a period of time. For e.g. to provide a education when the child gets into university or to create a retirement fund at age 55. While endowment policy is not the only way to achieve those financial goals, it is still a good method for those who are risk averse.

An endowment plan consist of a death benefit but that is usually not the main concern. Most will look into the guaranteed returns or total returns. It can be difficult to compare a plan with another these days due to the different features. For a 15 year saving plan, one company may require the policyholder to pay for the full 15 years while another may require you to pay for as short as 1 year, 3 years or just 10 years in what we called as a “limited-pay endowment policy”.

This is a case study of my client who have the following financial objective.

- An endowment plan to mature in 15 years time

- Expect about $70,000 in maturity amount.

A typical comparison of endowment plans starts with the plans that are able to achieve the client’s financial goal. In this case, there were a total of 8 plans from various companies.

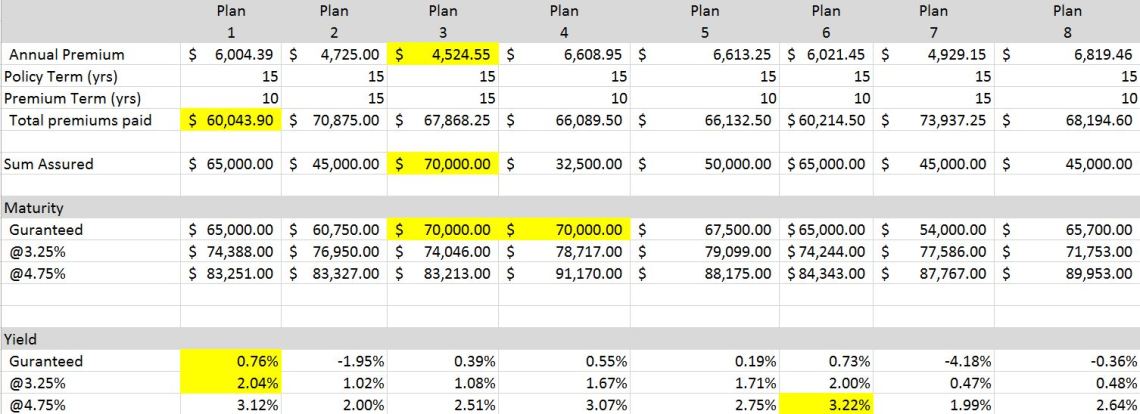

Table 1

Those highlighted were the “best” in their respective feature. The premiums used above were inclusive of any riders included. I prefer to use this premium instead of the basic premium because it is the actual amount paid and it should be used as a reference to the returns. However, other financial advisors may just use the basic premium and exclude any riders or premium loadings.

It can be difficult to compare since the premium, premium term and returns all varies from one plan from another. So, a more accurate way is to compute the internal rate of returns which are the percentage illustrated on the yield table.

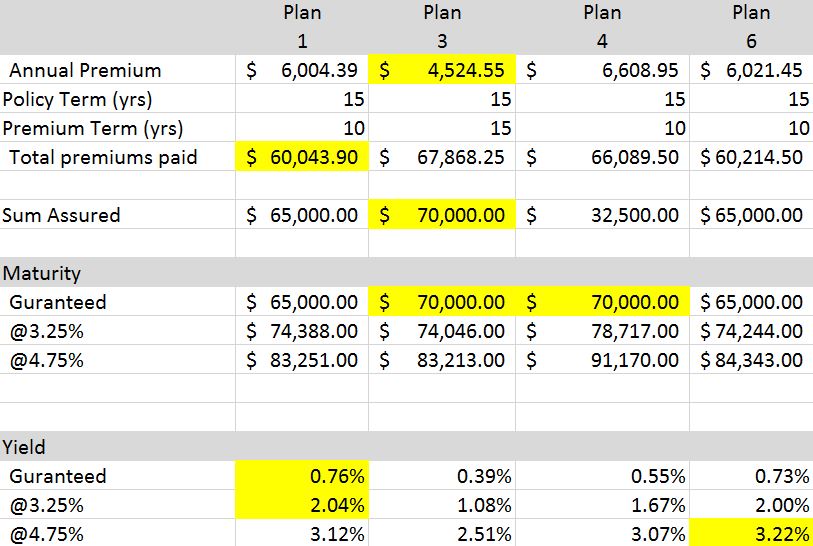

It can be rather confusing for a client to make a decision if they have to consider all 8 plans so the plans are usually presented after filtering out the not so ideal plans as shown below.

Table 2

From the above, the plans will be explained to the clients in detail and together with the comparison table, it will be easier for the client to make an informed decision.

A client with a budget constraint or concern with death benefit may choose plan 3 that has the lowest premium and highest coverage amount although it may not be the best option.

For someone who is extremely low risk taker may decide to take up Plan 1 for the highest guaranteed yield. What this means is in the worst case scenario that the insurer did not pay any bonus for the next 15 years, the principle amount is not only guaranteed but you still get a yield of 0.76% per annum.

If the client is very optimistic of the market or the insurance company, he may decide to look at either Plan 1 or 6 since they have the highest yield base on 3.25% and 4.75% projection respectively.

There is no hard and fast rule to suggest one should choose a particular plan. It all depends on an individual’s personal choice. My role as a Independent Financial Advisor is to provide an objective view so that the client have a clear answer to his financial goals.