A happy new year to all. Let us start the year getting updated on the changes in CPF and understand how the changes will affect us. There are quite a few changes across different age group and we shall look the change that affect across all ages that is the contribution cap for CPF.

The changes to CPF salary ceiling

| 2015 | W.E.F 1st Jan 2016 |

| $5,000 | $6,000 |

What this means to you is more will go into your CPF if you are earning $5,000 this year. For discussion purpose, let’s assume our income $6,000 per month in both 2015 and 2016. Below shows the effect of the change.

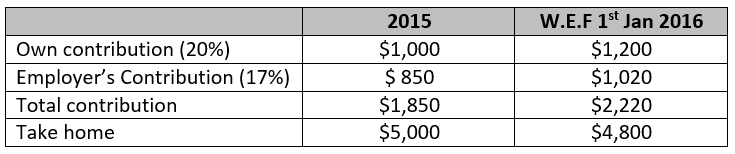

The reason why we contributed only $1,000 in 2015 is the salary ceiling back then was $5,000 so regardless how much you earn, only the maximum of $5,000 is subjected to CPF contribution. This year, our contribution will be $1,200 (20% x $$6,000) with the salary ceiling increased to $6,000.

It may not look like an attractive change to us because even though we are earning the same $6,000 in both years, the take home pay in 2015 will be higher than in 2016 but do note our employer also contribute on the amount up to $6,000 as well. If we consider the whole package of CPF total contribution and our take home pay, we would had “earned” $6,850 in 2015 and $7,020 in 2016.

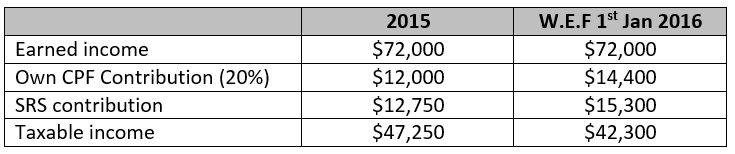

Another effect in on your personal tax. The following is base on an annual income of $6,000 x 12 mths and no other deductibles or reliefs except CPF contribution for ease of illustration.

Since you contribute more to CPF, you get more CPF relief. The taxable income therefore decreases and you pay lesser tax although you are getting the same income.

Another piece of good news to lower your income is the SRS contribution ceiling. The changes to Singaporean or Singaporean PR to SRS contribution is as follow.

A Singaporean or Singaporean PR can contribute maximum of $15,300 to the SRS account and get tax relief. To continue from the previous example on taxable income, we can further contribute to SRS to reduce our taxable income and the effect from the change is as follow. Likewise, for ease of illustration, we consider CPF contribution as the only relief.

In conclusion, while the change may mean more goes into CPF and less take home pay for some, the overall effect may not be as bad as we think. There are solutions to reduce your tax if you look around and I believe a financial planner can help you in this area if needed.