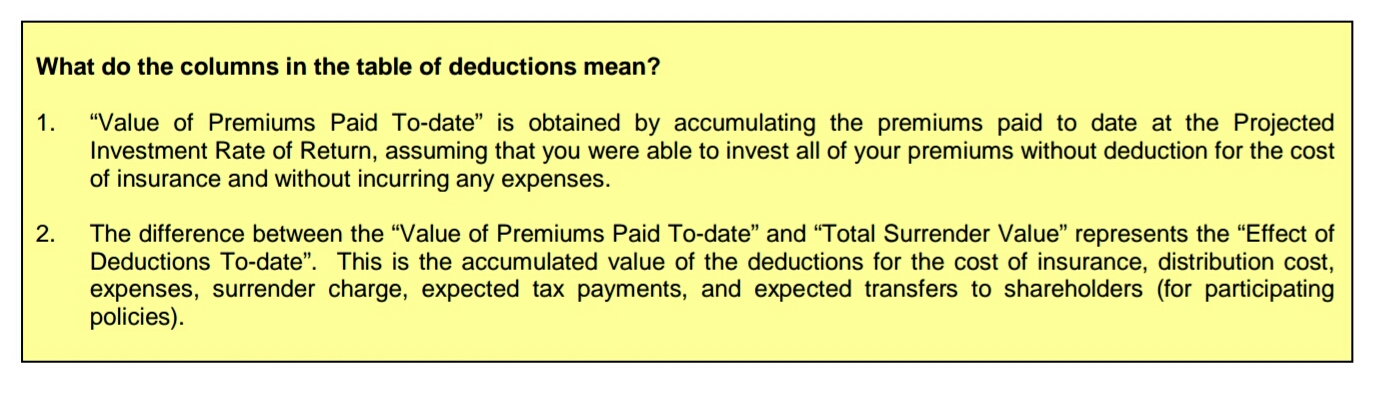

You might of have seen a page that states “Table of deductions” in your life insurance benefit illustration and have you asked what it means to you as a consumer?

I was surprised with the explanation of a prominent leader of the financial service industry on Table of deduction. This particular person explain the figures reflected as ” This is the amount that you are giving away to the insurance company to pay for the insurance company”. Is this right or wrong? Let’s look at the definition for “Table of Deductions” from Life Insurance Associate of Singapore (as shown below)

Do you notice any difference in the two explanation?

If you were to ask me, the amount you are giving away to the insurance company to pay for the insurance policy is called the “premium“.

Table of deduction, on the other hand, reflects the amount of differences that you will get back from the insurance policy as compared to if you had invested that money yourself at a certain rate.

Here’s an example of the table.

What it means to the consumer is – The premium of this policy is $2,308 per annum.

You could have use the amount of $2,308 to invest on any instrument that gives a returns of 3.25% or 4.75% per annum. (For discussion purpose, we use 3.25%)

If you had invested at 3.25%, your $2308 will grow to $2,383. However, you have used this money to purchase this policy which had $0 in the first year if you terminate it. The “potential financial loss” of the consumer will be $2383 because that is what he will potentially get if he had invested at 3.25% but got $0 when he terminate this policy.

Fast forward to the 5th year, if you had invested $2,308 per annum for the next 5 years and consistently get a rate of 3.25%, the amount you will get will be $12,713. This policy will have a surrender value of $5,749 at the end of 5th year. Therefore, the “potential financial loss” i.e the effect of deduction will be $6,964. You can get this

figure by using

The amount your money would had grown to if you had invested at 3.25% p.a less Surrender value

= $12,713 – $5,749

= $ 6,964

While it is good to use Table of Deduction as a factor to decide on a purchase of policy, it should no be the main factor especially if your policy is meant for protection instead of returns.