We had shared the potential risk receiving a claim payout which is much lower then the actual loss due to average clause when we under-insured our property. One effective way to avoid getting penalised by average clause is to purchase a insurance that is paid on first loss basis.

First loss insurance, also known as primary insurance or specific excess insurance, is a type of coverage that provides protection against a predefined portion of financial loss. Unlike traditional insurance policies that cover the full extent of a loss, first loss insurance only covers a specified percentage or amount of the total loss.

Benefits of First Loss Insurance

- Cost-Effective Protection: By covering only a portion of the total value of assets, first loss insurance allows businesses to mitigate their risk exposure without incurring prohibitively high insurance premiums.

- Tailored Coverage: First loss insurance policies can be customized to address the specific risks faced by individual businesses. This flexibility ensures that businesses are adequately protected against their most pressing threats.

- Cash Flow Preservation: In the event of a loss, first loss insurance provides a financial cushion that can help businesses weather the storm without depleting their cash reserves or resorting to costly borrowing.

- Risk Management Tool: By identifying and quantifying potential losses, first loss insurance enables businesses to implement targeted risk management strategies to minimize their exposure to risk.

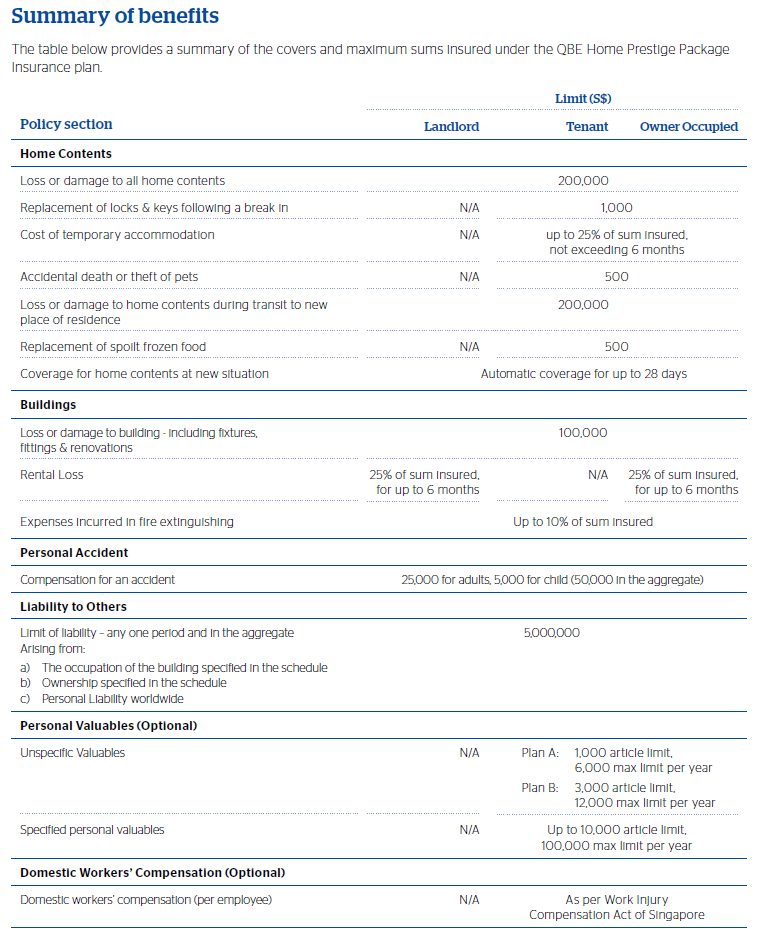

For example, Sarah bought a house worth $1mil. She purchase a first loss basis home insurance policy with benefit as shown below which will will cover up to $200,000 which is 20% of the property value in the event of a covered loss. If she had purchased an insurance policy which had average clause applied, she will be penalised and entitled to 20% of her claims made. As this is paid on first loss basis, she will receive up to $200,000 regardless the value of her property at the point of claim.

Incident: A fire broke out at Sarah’s home. She sustains damages to the renovation, contents and other valuables. The total damage to her home is estimated to be $180,000.

First Loss Insurance Claim Process:

- Reporting the Damage: Sarah contacts her insurance company to report the damage to her home caused by the fire.

- Damage Assessment: An insurance adjuster assesses the damage to Sarah’s home to determine the extent and cost of repairs. They confirm that the damage falls within the scope of Sarah’s policy coverage.

- Calculation: Since Sarah’s first loss basis policy covers up to 20% of her home’s value ($200,000), and the total damage is $180,000, Sarah’s claim falls within the coverage limit.

- Claim Processing: The insurance company processes Sarah’s claim and approves it for the maximum coverage amount of $180,000.

- Payment: Sarah receives a payout of $180,000 from her insurance company, which she can use to repair the damage to her home.

Outcome: Sarah’s first loss basis home insurance policy effectively mitigates her financial loss resulting from the fire damage. While the insurance payout may not cover the entire cost of repairs, it provides significant assistance, allowing Sarah to restore her home to its pre-loss condition without shouldering the entire financial burden herself. This helps Sarah recover more quickly and ensures that her home remains a safe and secure place to live.

In an unpredictable world, first loss insurance offers businesses a strategic means of safeguarding their financial interests against unforeseen events. By providing cost-effective protection tailored to the specific risks faced by each business, first loss insurance empowers companies to navigate turbulent times with confidence. As part of a comprehensive risk management strategy, first loss insurance can help businesses not only survive but thrive in the face of uncertainty.

You may also be interested to know Three reasons our fire insurance may not pay.