Retrenchment is a dread word.

Having enter the work force and becoming a insurance agent during the Asian Financial crisis, survived the Tech Bubble and Global Financial Crisis, I saw retrenchment happened in all these financial crisis. In fact, that was the reason I decided to leave the job as an Facilities Technician when I was in my 20s, I saw those in the 40s getting the pink slip and I asked myself if I want to be one of them if I hit 40s. I took the risk to join the financial advisory industry because I do not want to be retrenched.

Retrenchment is likely to be a word that is commonly heard in the coming months especially when countries are out of COVID-19 and the support from the government stop. It is likely that more companies will be restructuring their business model. We may not be able to stop that from happening to us but we can mitigate the risk. Retrenchment Insurance is one way that you can “insure your income”.

Coincidentally, the topic of unemployment insurance was raised in the Parliament by Ms Sylvia Lim just before the COVID-19 outbreak in February 2020. That was not the first time that the topic was brought up. Ms Lim had brought it during the Budget debate in 2016 but the concept was slightly different. Unemployment insurance, also known as redundancy insurance, was to ensure that those who lose their jobs because their job became redundant could get a payout. In any case, this article has no intention to discuss the policies by the government but what we can do as an individual. If there is a retrenchment insurance for you, will you take it up?

NTUC Income had a Retrenchment Insurance plan in 2004. It was taken off the shelf because the take up rate was too low. Majority of the people never think they will lose their job. Even from a financial planning point of view, some may think this plan is unnecessary because we can self-insured this risk by having a rainy day fund of at least six months of our expenses in our savings account.

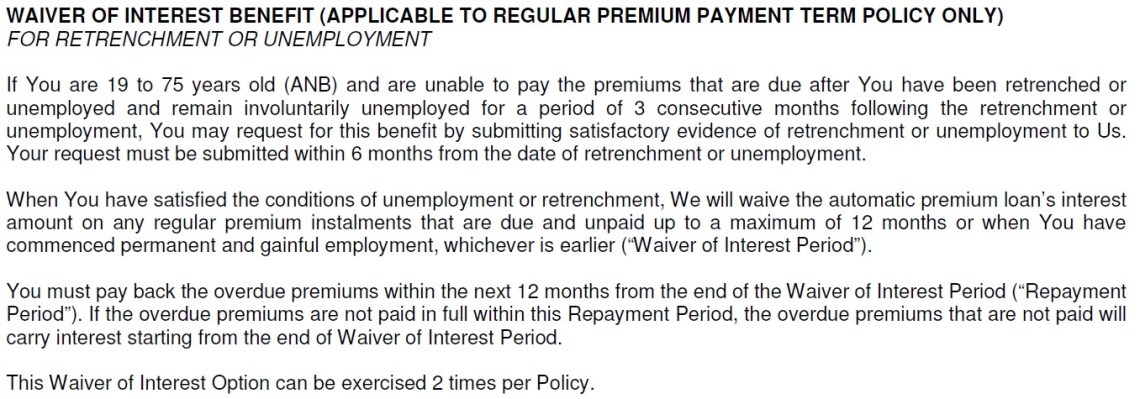

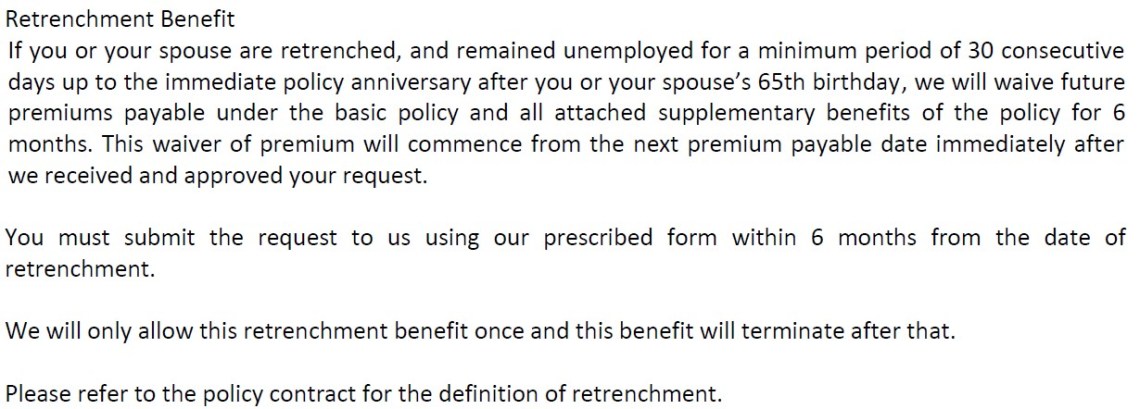

With COVID-19 happening now, we had seen insurance companies having insurance deferment schemes to help those who face difficulties to pay their insurance premium due to COVID-19. The Family Protect from NTUC Income is one plan with retrenchment benefit. It pays 1% of your sum assured each month up to 3 months, subject to terms and conditions of the policy. There are also insurance plans with similar retrenchment benefits. Unlike Family Protect that provides a payout during a retrenchment, these benefits may waive the premium for a period of time. Some examples of the different benefits offered by different insurers are seen below.

Aviva

Manulife

NTUC Income

Let us know your opinion. Do you think retrenchment insurance may see a revival? Or will insurance with retrenchment benefits be a factor for consideration in future purchases?

I believe that there is still a need for unemployment insurance, very much like disability income insurance.

Not everyone has the necessary resources to put aside 6-12 months of emergency savings (living expenses). I’ve read a recent article that many singaporeans do not have much savings?

It would be good for the government to run such a scheme for cost effectiveness, if not insurance companies can offer it again.

LikeLike