Insurance originated as a tool for risk transfer. It works on the concept of risk pooling where a group of people with a common risk put in a little sum of money together and should there be a financial loss due to that risk, the money that is pooled together will be used to compensate the financial loss.

As market evolves and product manufacturers get more innovative, there are many types of insurance other than the usual life insurance, savings insurance, motor or travel insurance etc. For instances, pet insurance are getting more popular these days as pet owners see their feline and canine friends more than just pets. The cost of medical treatment and even pet burial can have an impact on the pet owner’s financial situation especially when they usually comes unexpected. Our mobile phones crossing the four figures and a screen crack can cost a big hole in the owner’s pocket these days. To mitigate our financial loss, Telcos and insurance companies begin to launch Mobile phone insurance to protect against screen damage, 1-to-1 replacement and other benefits.

While the premiums for these insurance are usually affordable, the question is should be buy it or are we just feeding to the product manufacturer’s profits? Every insurance is worth buying and everything should be insured if we use our right brain to think. The premium is always going to be much lower than the actual loss. However, if we had used our left brain to be more analytical and methodical in our thinking then we can use the logic process as shown below.

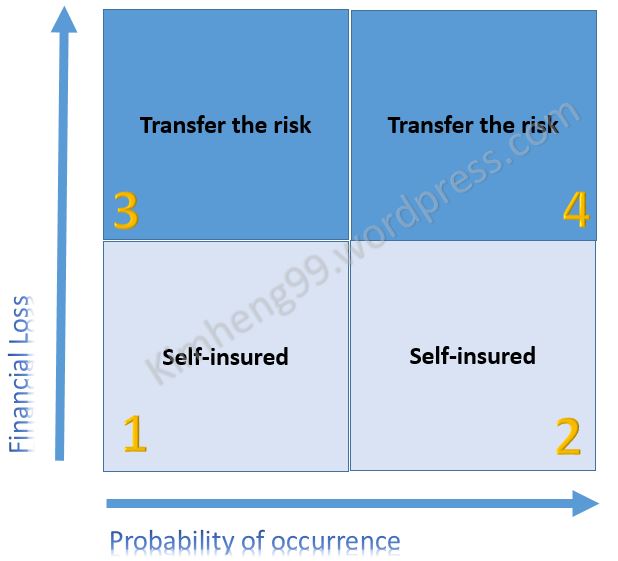

The X-Axis shows the probability of occurrence. It means the likelihood of the same incident happening again and again and again. For e.g. between a high fever and a fractured arm, most likely a high fever has a higher occurrence rate or probability of loss. So, if we want to insure between the two, which should be take priority? Logically it should be a high fever because it is more likely to happen and we are more likely to claim for it then a fracture arm. However, another person may say we should insure against the fracture arm because the cost of treatment is more expensive than a high fever. That is what the Y-Axis refers to – the financial loss on that incident.

Looking at Quadrant 1, it can be interpreted as if the probability of occurrence is low and the financial loss is low, we should self-insured this amount than to buy an insurance for it. For e.g. it is very unlikely anyone will buy an insurance to cover his spillage of coke in a fast food restaurant because it happens but very seldom and even if it happens, he can easily afford to buy another cup of coke.

Further down the X-Axis in Quadrant 2 are those incidents that maybe common but the financial loss is low. For e.g, a clerk always get cut by the edges of the paper. It makes more financial sense to buy the plasters herself to paste over the cuts then to pay for an insurance to cover the cost of the plasters.

Some incidents as illustrated in Quadrant 3 are may have a low probability of occurring or the incident may not occur at all. However, if it happens, it will cause a serious financial burden on our pocket. For e.g. a cancer treatment. Not everyone will suffer from cancer but if one is diagnose with it, the medical cost will be very challenging for most of us. We should transfer this risk to the insurer.

Lastly in the last quadrant is those with high probability of occurrence and the financial loss is substantial to us. The risk in this quadrant obviously needs to be transfer out to the insurers. We should pay the premium and let the insurance company handle the financial loss if it happens. For e.g., a shipping company has to send the goods to her customer. The ship has to pass thru’ the Straits of Malacca that has very high piracy attacks. But in managing risk, we may want to look at the situation deeper and think why is there such a high occurrence rate and can we manage that. As a company, they may want to change to air freight to avoid the risk. We also try to lower the rate of occurrence. For e.g., a company have a high rate of damage products and that resulted in not just financial loss to the company but also reputation loss of the company. The management realised the staff at the operation department are not well train in using the machines. With further training, the company can manage the damage and financial loss better.

As we can see from the examples, although insurance is a risk transfer mechanism, it requires both the policy owners and insurers to do their part. The policy owner cannot have the mentality of letting the insurers settle the payment since premiums are paid. That kind of mentality will cause future premium to surge. On the insurers end, they need to assess the risk and charge a premium that is fair to the policy owners.