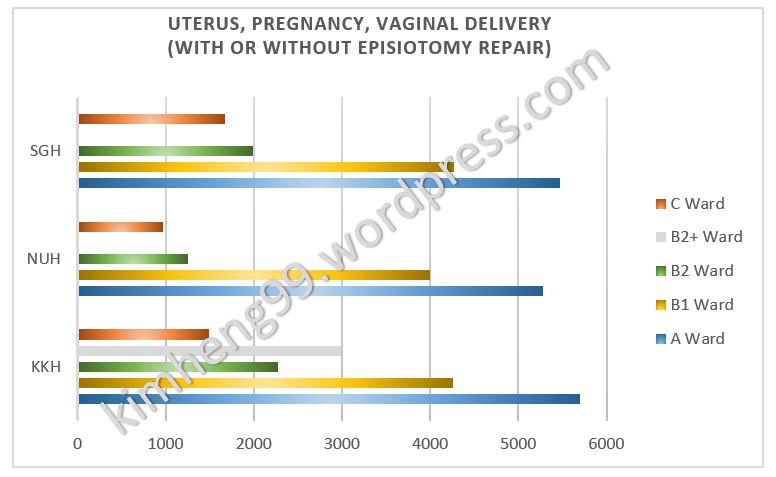

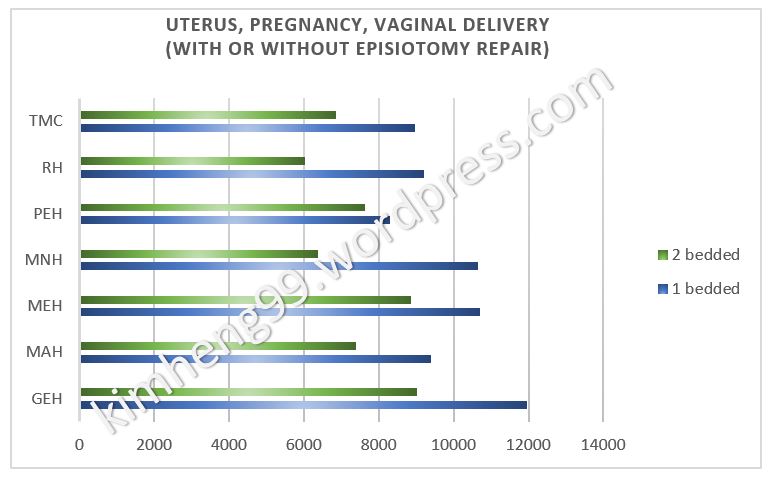

A pregnancy last an average of 40 weeks and is broken into 3 stages. The First Trimester (week 1- 12), Second Trimester (Week 13 to 28) and the Third Trimester (Week 29 to 40). We are not discussing the physical well-being for mum-to-be here but we shall look at what are the different financial planning that can be considered. This is especially important when an child delivery in Singapore may not come cheap. The following are delivery cost by 75% of the patients in the respective hospitals.

Public hospitals

Private Hospitals

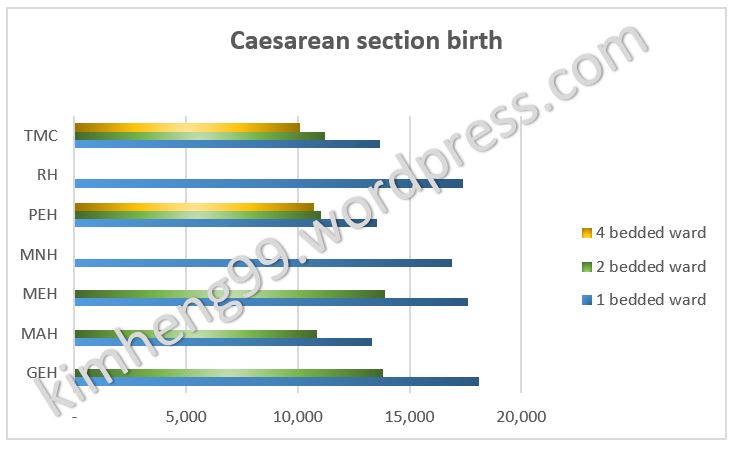

The cost for Cesarean Section Birth is much higher as below.

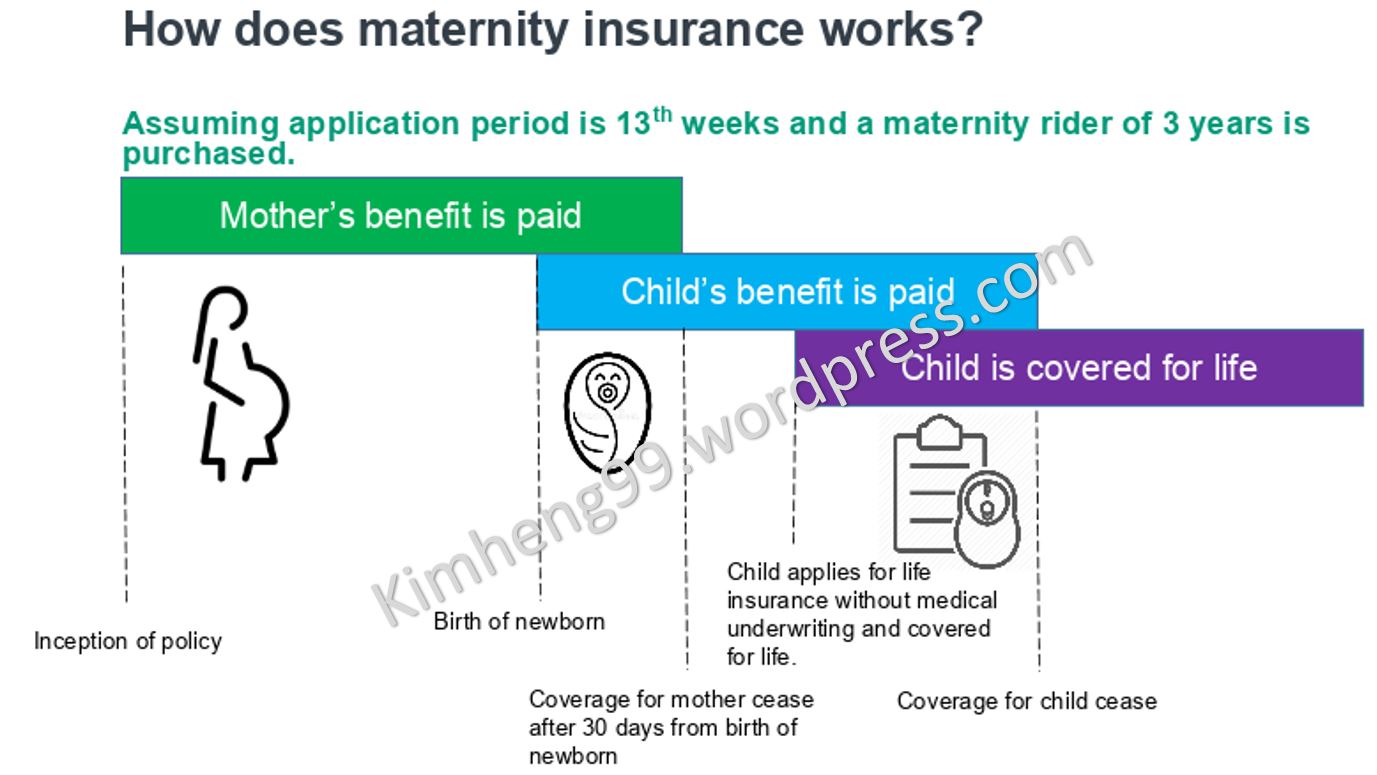

There are quite a handful of maternity insurance in the market at the moment. Most will require the expectant mother to buy the maternity plan and another plan for the child when he is born. I prefer the AIA Guranteed Protect Plus with AIA Mum2Baby Protect because it can be attached to an whole life policy. I do not encourage Investment-Linked Policy and will prefer to give the maternity plan a miss if it has to be attached to one unless it is far superior than the rest in the market. This plan allows the newborn to purchase an insurance within 60 days from birth without medical underwriting. Pre-exisiting conditions of the newborn is also covered up to $30,000 within 90 days of birth; up to 6 years old. And my favorite feature for this plan is it allows the transfer of the expectant mother’s policy to the newborn. What this means is that the expectant mother not only save the additional money to buy one more policy for the newborn, the premiums that she had paid for herself can be transferred to the newborn’s policy. This saving for the additional policy can be put to a better use.

Here is an video explaining how AIA Guranteed Protect Plus with AIA Mum2Baby Protect works.

Once the newborn is delivered, the most important plan to consider is medical insurance and the integrated shield plans(ISP) will do the job. One issue with ISP is most insurer allows the child to apply from the 15th day of birth. Good news is that Medishield Life will provide cover from Day 1 of the birth.

With excess budget, you can look at protection plans for the child or saving for his education. However, please look into the parent’s coverage first! It is important to ensure the parents leave enough financial resources to take care of the child if the unforeseen misfortune happens. If the child do not have the financial resources to see through even Primary 1, there is no purpose to create an education fund for his university. Like the wise said, ” If you have a goose that lays golden egg, will you protect the goose or the eggs?”

By this time, your financial planning is almost completed. The last piece of puzzle will be a personal accident plan. While it is always good to start as early as possible, I will encourage this to be in place when your child learns to walk. That is when the curious child is likely to get injured . Most are minor injuries like bruises or bumps but as a concern parent, you may prefer to send him to see a doctor especially if the injury is on the head. These out-patient bills may not be expensive but cumulatively, it can be quite a sum of money too. A personal accident plan may come in useful.

Having mentioned some plans in this article, I would like to stress that there is no one plan that fits all. Please speak to a financial adviser for proper recommendation.

By submitting this form, you agree that Avallis Financial may collect, use and disclose your personal data, as provided in this entry form, for the following purposes in accordance with the Personal Data Protection Act 2012, the Privacy Statement and the Data Protection Policy of Avallis Financial.