What does blackout has to do with Insurance?

During the blackout, there were numerous post on Facebook regarding this disruption. One of such post made was as below.

Most likely the milk was not damaged in any way but the ice-cream is likely to have melt but still edible. What if it was something more valuable and it deteriorated during the blackout especially if you are running a eatery? Who will pay for your damaged stocks?

In most home insurance and some business insurance, deterioration of stock in refrigeration is a covered event. However, the policy wordings maybe differ between companies. Let us look at policy wordings from a few insurers.

Insurer A

Insurer B

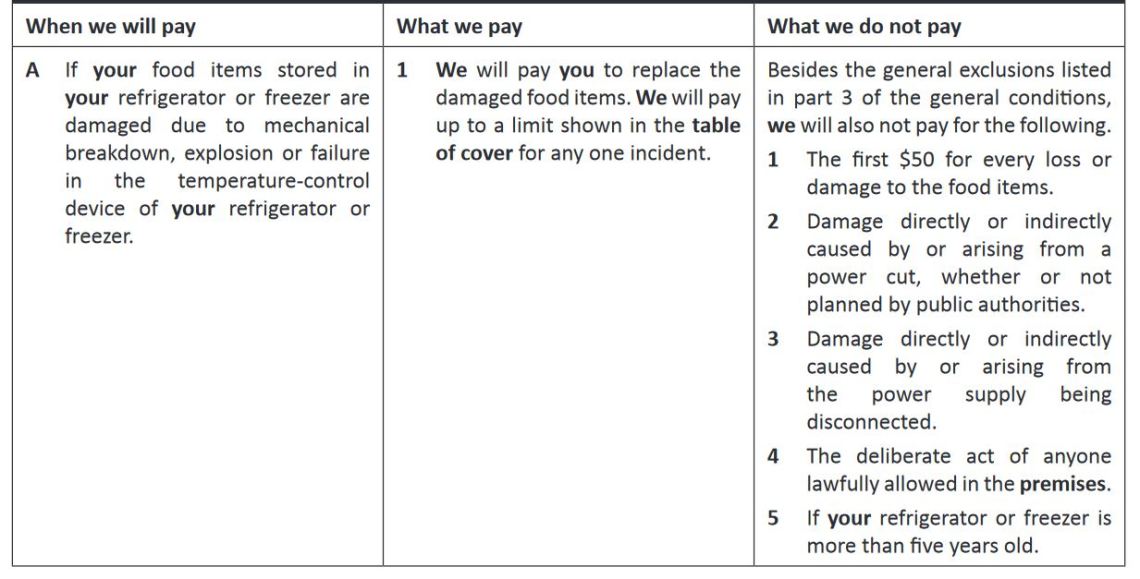

Insurer C

You might have notice that other then the benefits, the scope of coverage may be different. Some insurers may even impose a minimum hours of electrical breakdown before a compensation is admitted.

Another highlight is the exclusion. Insurer A states that it will not pay “Loss or damage caused by a deliberate act of or a pre-scheduled maintenance with prior notification by the company (or its employees) supplying Your power.” and Insurer B states that “We will not pay for loss or damage arising from: (b) Any act of the public utilities authority or its employees.” However, Insurer C states that “Besides the general exclusions listed

in part 3 of the general conditions, we will also not pay for the following. 2 Damage directly or indirectly caused by or arising from a power cut, whether or not planned by public authorities.“

Now, think about this – If you are insured with Insurer A, the neighbour on your left is with Insurer B and the neighbour on your right is with Insurer C. All 3 of you submitted a claim for your damaged food under this section for the recent power outrage, who is likely to have a successful claim? It might also interest you to know that some company may not even cover this event at all.

The clauses in general insurance are not like life insurance which have similar clauses regardless of company. It is very risky to purchase a general insurance such as motor insurance or home insurance base on the cheapest premium. Look into the policy wordings which can be very lengthy but you may not have to read the whole document but read what you think will be of risk to you. Alternatively, speak to your financial advisor and he can help you.