There was a period of time when a million dollar was a unreachable figure. I’m not saying that it is an amount that is easy to accumulate today but it is more realistic. Afterall, an average HDB flat can cost close to half a million and some flats were sold above the $1mil mark in some area.

So, do you need a million dollar cover and how much do one really need as a coverage amount? Here are some methods you can use to estimate your coverage required.

1) Multipliers of Income Approach

This is a very traditional method of calculation is taking your annual income multiply it by 5 or 10. That is to assume if premature death occurred now, your love ones will have 5 to 10 years of your income replacement to let them adjust to the lifestyle prior to the death. This method is the easiest but it has it flaws because in practical sense, the dependents may never have the same earning power as the sole breadwinner. For e.g. I have a client who is in management and earns nearly $20,000 per month. His wife have not been working since the birth of the first child more than 10 years ago. Will it be easy or possible for the housewife to get back to employment and earn $20,000 in the next 5-10 years? It can be tricky to decide how long the family will adjust to the lifestyle without the sole breadwinner’s income.

This is a very traditional method of calculation is taking your annual income multiply it by 5 or 10. That is to assume if premature death occurred now, your love ones will have 5 to 10 years of your income replacement to let them adjust to the lifestyle prior to the death. This method is the easiest but it has it flaws because in practical sense, the dependents may never have the same earning power as the sole breadwinner. For e.g. I have a client who is in management and earns nearly $20,000 per month. His wife have not been working since the birth of the first child more than 10 years ago. Will it be easy or possible for the housewife to get back to employment and earn $20,000 in the next 5-10 years? It can be tricky to decide how long the family will adjust to the lifestyle without the sole breadwinner’s income.

2) Need-based Approach

An more commonsensical method is the need-based approach. It can be very comprehensive but because of the comprehensiveness, it can be a complicated process. This method takes into account the financial obligation an individual have for each dependent and the assumed inflation rate till that dependent becomes financially dependent. The individual’s assets will be categorised into cash, near-cash assets such as shares and unit trust which can be converted to cash within days assuming market valuations are not an issue. However, assets such as properties will take months to be convert into cash. The properties can be further categorised into stay-in or investment property. For e.g. if an individual own only a property which the family is staying currently, it is unlikely the dependents will sell it else they will lose the roof over their heads. But if the dependent have another property, the dependent can consider selling it to have more cash on hand if needed.

An more commonsensical method is the need-based approach. It can be very comprehensive but because of the comprehensiveness, it can be a complicated process. This method takes into account the financial obligation an individual have for each dependent and the assumed inflation rate till that dependent becomes financially dependent. The individual’s assets will be categorised into cash, near-cash assets such as shares and unit trust which can be converted to cash within days assuming market valuations are not an issue. However, assets such as properties will take months to be convert into cash. The properties can be further categorised into stay-in or investment property. For e.g. if an individual own only a property which the family is staying currently, it is unlikely the dependents will sell it else they will lose the roof over their heads. But if the dependent have another property, the dependent can consider selling it to have more cash on hand if needed.

As mentioned, this method is very commonsensical and we can see it using this simple case study.

An individual has a wife, a son age 5 and a daughter age 4. The wife is financially independent on him and he provides $500/mth to each child. He wants to provide the children till they are age 21. We can use the following to calculate the amount of coverage he need.

(Age of child’s financial independence – current age of child) x $500 x 12

For the son, it will be

(21 – 5) x $500 x 12 =$96,000

For the daughter, it will be

(21 – 4) x $500 x 12 = $102,000

The total amount of coverage required for him will be $198,000.

Do note in an actual planning, a financial advisor will take into consider that inflation rate to ensure the $500/mth is in line with the cost of living.

3) Income Protection Approach

One of the easiest is to look at the potential income a person can earn till his retirement. The retirement age can be 50,55,60,65 or even beyond that. This method is similar to how workman compensation or a court decide on a disability or death compensation. The disadvantage is it is difficult to assume the increment rate. The amount can be derived using the following

One of the easiest is to look at the potential income a person can earn till his retirement. The retirement age can be 50,55,60,65 or even beyond that. This method is similar to how workman compensation or a court decide on a disability or death compensation. The disadvantage is it is difficult to assume the increment rate. The amount can be derived using the following

(Retirement age – Current Age) x Current Income

However, in a real life, a person’s income will increase over the years because of his experience or promotion and we have to take into account the salary increment over the years. The amount after taking into account the increment can be compute using a financial calculator.

PMT= Annual income

Ir= Assumed increment annually

np = No. of working years (i.e. Retirement age – Current age)

Click “FV”. The figure shown on FV is the potential income one stands to earn.

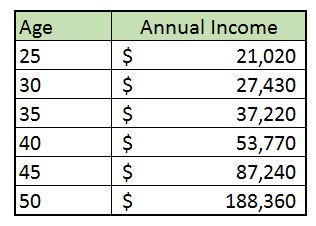

Assuming the retirement age is 55, a person with the below income at different age will generate $1,000,000 of income assuming there is a 3% increment annually.

What the chart above means is if a person is age 25 years and earns a minimum of $21,020 annually, he should protect his loss of income of $1,000,000 that is potentially in the bank if nothing goes wrong.

Please note the 3 methods of calculation are meant to be informative only. For a proper assessment, please speak to a financial adviser.

I love your blog.. very nice colors & theme. Did you design this website yourself or did you hire someone to do it for you? Plz respond as I’m looking to design my own blog and would like to know where u got this from. cheers

LikeLike